Personal Wealth Management / Market Analysis

This Is Not the Financial Crisis’s 10-Year Anniversary

The run on BNP Paribas's hedge funds didn't end the bull market-the death knell was the mark-to-market accounting rule's taking effect later in 2007.

Editors' note: MarketMinder does not recommend individual securities. The below simply represent a broader theme we wish to highlight.

10 years ago today, France's largest bank froze three hedge funds as subprime-panicked investors fled. Headlines globally are calling this the beginning of the Global Financial Crisis, and at first blush, it certainly has all the trappings. Packaged subprime mortgages, a run on a bank, a liquidity crunch and hard-to-value assets. World stocks slid -7.3% in just 6 trading days when the news broke.[i] But then they bounced. By Halloween, the MSCI World Index was up 6.2% since BNP Day.[ii] That turned out to be world stocks' peak. US stocks peaked weeks earlier, on October 9. "Why" is always harder to pin down than "what," but all evidence suggests it's no coincidence the bear market began as banks started taking the asset writedowns required by FAS 157-the mark-to-market accounting rule-which took effect in November. Subprime and frozen funds are part of the backstory, but in my view, mark-to-market was the catalyst that ultimately destroyed nearly $2 trillion in bank capital. That catalyst no longer exists, as regulators subsequently neutered the rule-something to keep in mind today, as headlines warn a resurgence of allegedly risky debt raises the likelihood of a 2008 repeat.

BNP's funds weren't the only ones that imploded in 2007. Two Bear Stearns hedge funds collapsed in June and July, forcing creditors to liquidate some of the funds' collateral. As The New York Timesreported at the time:

Several lenders, including JP Morgan Chase, Goldman Sachs and Bank of America, reached deals with Bear Stearns that forestalled a need to sell securities in the open market. It appeared that some lenders pulled back over concerns about the effect that a large liquidation would have on bond prices and investor confidence. While the securities involved represent a fraction of the market, a liquidation could have forced a bigger sell-off while setting a lower price.

One lender, Merrill Lynch & Company, moved ahead with plans to auction $850 million in collateral it had seized from the Bear funds, according to people briefed on the matter. And Deutsche Bank was said to be shopping $600 million in assets.

The boldface is mine, because it is the kicker: While mark-to-market accounting wouldn't be the law of the land until November 15, some banks were phasing it in. Selling assets at fire-sale prices would make these banks write down the value of all comparable assets on their balance sheets. Whether or not they intended ever to sell them. But at the time, we didn't get that vicious circle of fire sales, writedowns, more fire sales and more writedowns. Banks plodded along until October, the eve of mark-to-market D-Day. That's when the writedowns got fast and furious. UBS, Citigroup, Merrill Lynch and others took hits then. Bear Stearns took its big one on November 14.

In principle, mark-to-market accounting is fine-for some assets. But at the risk of oversimplifying, before FAS 157 banks could put assets in one of two balance sheet buckets: "for sale" or "hold to maturity." In the first, banks intend to trade them, so valuing them at the going market price makes sense. Your trading portfolio is worth only what you can sell it for. But in the second bucket, valuing them at the market price is rather senseless. If you don't intend to sell, ever, the potential selling price doesn't matter. Banks holding mortgage-backed securities to maturity cared only about the interest income, which never really dried up (even as market values sank). But FAS 157 forced their hand. Once it took effect, all banks had to take paper losses on illiquid, held-to-maturity assets whenever another bank fire-sold them.

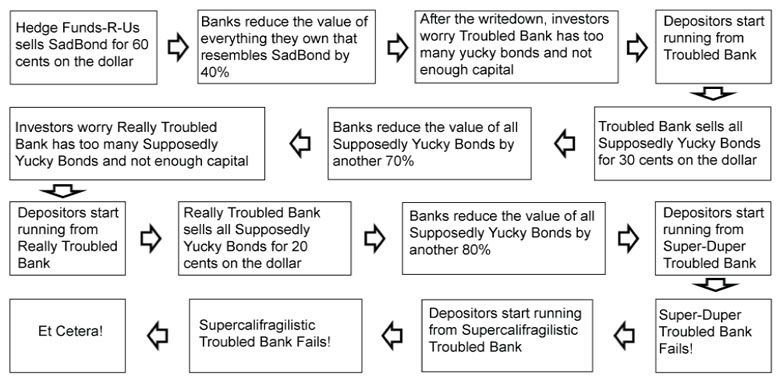

Here you might ask, "if banks never meant to sell assets, then what fire-sales were there to mark to?" This is where the hedge funds come in. Thanks to some changes in the Net Capital Rule, which regulated investment banks' use of leverage, hedge funds were margined to the hilt in 2007. So they didn't just need to worry about raising cash to meet investors' redemption requests. They also faced the risk of margin calls. This is what happened to Bear Stearns' funds, triggering fire sales that summer. There was no summertime bank balance sheet bloodbath because most banks didn't have to take the corresponding hit. But once mark-to-market took effect, any time a hedge fund sold, banks got blasted, creating a negative feedback loop. Here's a toy model:

Exhibit 1: An Oversimplified Financial Crisis

Source: My weird brain and history.

Your next logical question might be, "why were all these writedowns a surprise?" That's where the fact these were illiquid assets comes in. By illiquid, I mean, "rarely traded and hard to sell in a pinch." Since stocks trade constantly, it's easy to figure out what they're worth. But for something that doesn't change hands frequently, it's more difficult. The last reference price might be months old-or more. Pretend you're Hedge Funds-R-Us trying to sell that hypothetical SadBond in January 2008, three months after anyone else traded it. Three months of scary headlines, volatile markets and worldwide handwringing. You reckon you'll have to accept a lower price, but you have no way to measure how low, because fear is impossible to quantify. X number of headlines doesn't equal a Y% discount. You just have to put it out there, hope for the best, and see what bids you get. When buyers know you're desperate, they'll lowball. Just how it works.

Mark-to-market made 2008 great for bargain shoppers, including the Federal Reserve, which ultimately reaped handsome profits on Bear Stearns' not-toxic-after-all assets. But for banks and investors, it was wretched. No one knew when the next writedown would come or what collateral damage it would inflict. People hoped a wave of January writedowns would be the extent of it, but then Bear Stearns failed. A month later, Merrill Lynch took a fresh $6.6 billion writedown, triggering another wave. In mid-May, Citigroup announced plans to shed $400 billion in assets over the next three years, and everyone braced for more pain. After a summer of writedowns, Merrill fire-sold its portfolio of mortgage-backed securities to Lone Star Capital, effectively pulling the rug out from under its peers and setting up the Great Dismantling of Wall Street as We Knew It. Within weeks, Lehman Brothers was dead; AIG was a ward of the state; Goldman Sachs and Morgan Stanley were bank holding companies instead of investment banks, allowing them to tap Fed funding; WaMu was seized by the Office of Thrift Supervision; and Merrill Lynch became property of Bank of America. The government's inconsistent, haphazard response triggered the massive panic that roiled stocks in September and October. When the feds chose who lived and who died with seemingly no rhyme or reason, everyone froze. No one wanted to take risk, whether that risk was funding a bank or buying a stock.

The crisis ultimately ended the next March, during a Congressional hearing on mark-to-market. As investors anticipated changes to the rule, which the Financial Accounting Standards Board eventually delivered, stocks rallied. The amendment, released April 9, relieved banks of the need to apply mark-to-market to illiquid, held-to-maturity assets. That stands to this day.

This is why all the warnings of 2008 redux-which we've seen for 10 years now-are moot. Mortgage-backed securities are still with us, but we now know they weren't toxic. Even the subprime-based ones. They were back near face value years ago, proving the crisis didn't have to happen.[iii] If the rules let banks ride it out, with no writedowns on illiquid assets they never planned to sell, everything probably would have been fine. Overleveraged hedge funds would still have had their day of reckoning, but the banks would have been able to cruise, collect the income and wait for the storm to pass.

Thankfully, this is what they can do the next time people get jittery about subprime or illiquid, opaque packaged debt. The financial system is by no means risk-free, but without mark-to-market, troubles in isolated parts of the market shouldn't ripple through banks' balance sheets.

[i] FactSet, as of 8/8/2017. MSCI World Index return with net dividends, 8/8/2007 - 8/16/2007.

[ii] FactSet, as of 8/8/2017. MSCI World Index return with net dividends, 8/8/2007 - 10/31/2007.

[iii] So said former FDIC head William Isaac in his most excellent book, Senseless Panic.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today