Personal Wealth Management / Economics

Three Quick Hits on Energy

The latest nuggets on the US, EU and Japan.

A mere weekend has passed since we last checked in on global Energy markets, yet it seems like there is at least a week’s worth of news. How are US oil producers responding to higher European demand and continued fears of a supply shortage? Are EU member states united behind the idea of a Russian oil and gas ban? And what of Russia-reliant Japan? We will explore all three stories momentarily, but spoiler alert: The widely feared supply shock still doesn’t appear to be at hand.

US Producers Step Up

Last Friday, Reuters reported on private US export terminal data showing some encouraging news: The US exported more crude oil to Europe in March and April, with much of it coming from Texas’ prolific Permian Basin. “At least 65% of U.S. crude shipped to Europe in March was identified as WTI Midland in U.S. Customs data on Refinitiv Eikon, a 63% increase from the same month last year. The cargoes, most of which are priced from the Magellan East Houston terminal, carried about 22 million barrels overall.”[i] Much of it went to Denmark, Italy, Spain and the UK.

Now, this might seem suboptimal from an American point of view, considering we are all trying to survive sky-high gas prices. But it should actually help temper prices globally. As we discussed last week, there are varying grades of oil, and refineries are usually geared toward heavy sour crude or light sweet crude (except in Europe, where many are homologated for Russia’s Urals oil, which basically blends the two). The Permian Basin pumps light sweet crude. But Gulf Coast refiners are mostly equipped to process heavy sour crude, which can risk the light sweet stuff piling up. Exporting the surplus to Europe eases the US’s supply/demand mismatch and Europe’s feared supply crunch at the same time, which can help stabilize oil prices globally. As an analyst interviewed by Reuters noted, “light sweet crudes are easier to process by less complex refineries, often helping them offset higher processing costs.” It is as close to a win-win as you can get.[ii]

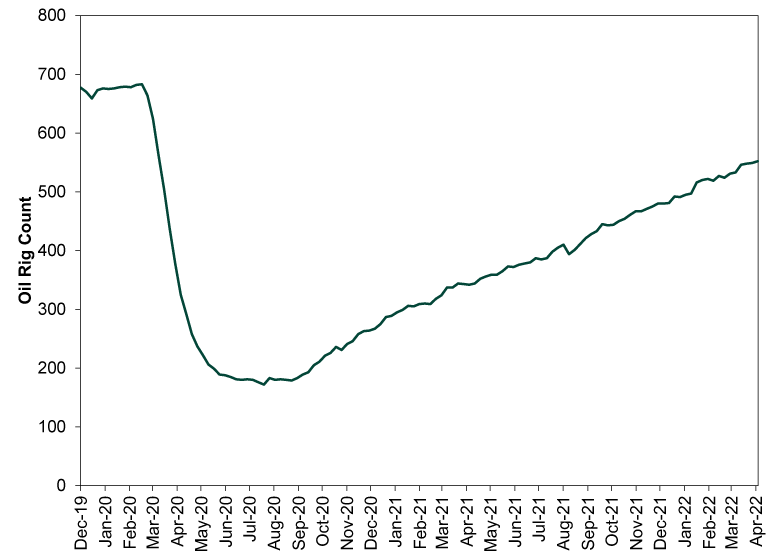

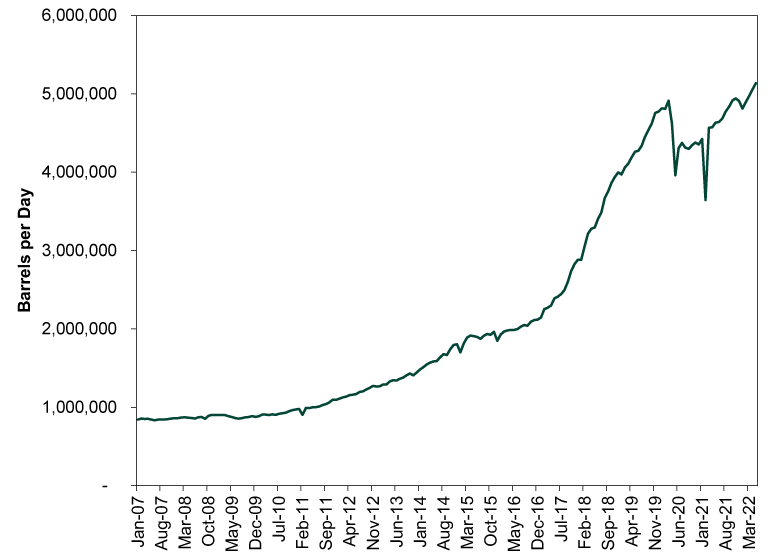

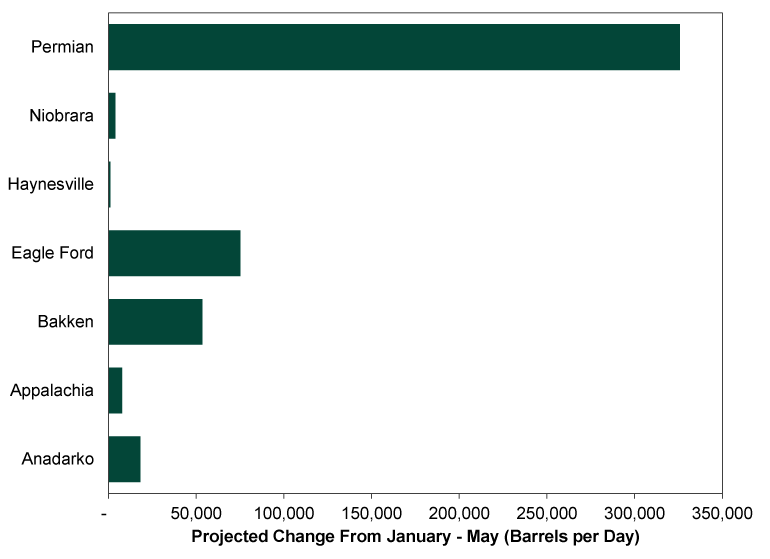

This raises another point: Overall US production is on an upswing. For months now, we have seen pundits bemoan the US oil industry’s failure to help the world avoid a shortage. Taking most of the commentary at face value, you might think oil producers are sitting on their hands. But as Exhibits 1 – 3 show, that isn’t the case. Oil rig count continues rising toward pre-lockdown levels. The US Energy Information Administration’s (EIA’s) projections see Permian Basin output hitting a fresh record high this month. Other regions lag, but all tracked by the EIA appear to be cranking higher since tensions in Ukraine heated up.

Exhibit 1: Oil Producers Are Adding Rigs

Source: FactSet, as of 5/2/2022. Baker Hughes Weekly Rotary Rig Count (US Oil), 12/31/2019 – 4/29/2022.

Exhibit 2: Oil Production Is Bigger In Texas

Source: US EIA, as of 5/2/2022. Total Monthly Production in the Permian Region, January 2007 – May 2022. April and May 2022 are EIA projections.

Exhibit 3: Other Major Regions Are Pumping, Too

Source: US EIA, as of 5/2/2022. Projected change in total monthly output from January through May 2022.

This is generally how markets work. Supply fears send prices higher. High prices incentivize producers to turn on the spigots. Supply increases. Prices stabilize. The timing varies, and the adjustment process can be painful in the short term, as it is for many now. But the market is responding to a big need, and in time, it should help ease the acute fears.

EU Leaders Still Negotiating a Russian Oil Phaseout

When last we left European energy, Germany had gotten behind a gradual, phased-in EU ban of Russian oil. But there were still some holdouts, particularly in landlocked Hungary and Slovakia, which can’t easily import oil by sea. EU sanctions require unanimous member state approval, and Hungary reiterated on Monday that it stands ready to veto any sanctions that hamper its ability to access the oil and gas it needs. This has triggered talk of sanctions that would exempt Hungary and Slovakia, and Germany’s economic and climate minister told the press on Monday that countries who lack diverse energy suppliers “must be respected.”[iii] The European Commission will reportedly present member states with draft sanctions on Tuesday, and ambassadors will talk everything out on Wednesday.

We aren’t diplomats, which is probably a good thing for the world, so we won’t guess at whether or not they agree on something. But the apparent willingness to grant exemptions suggests anything they announce will have a long timeline and plenty of holes—most likely amounting to voluntary participation from the nations that think they are equipped to handle it (or will be by the time the ban phases in). In short, the latest news seemingly underscores the low likelihood of a sweeping, sudden ban that presents a higher risk of an energy crunch and recession. Now, it is still possible Russia could retaliate with a sudden full ban of its own. It would be weird, considering Russia’s need for hard currency, but it could happen. However, markets move on probabilities, not possibilities, and for now the most probable scenario remains at most a managed phaseout.

Japan Is Still Buying Russian Gas

While most attention focuses on Europe, energy-import-reliant Japan is expanding its natural gas links with Russia. Not only is it continuing to get a boatload of natural gas from joint ventures with Russia on Sakhalin Island, but it is moving forward with new joint ventures in an Arctic liquefied natural gas (LNG) terminal that will eventually ship Russian gas from Siberia to Japan. In the short term, it is a reminder that economic need will usually come first. Japan is already suffering high energy import costs due in part to current prices and part to the weak yen. Cutting ties with a chief supplier now would make the problem even worse. Of course, from a geopolitical perspective, this has the less-than-optimal impact of blunting sanctions’ effects. But economically, in the medium term, Japan buying more gas from Russia should free up more of the world’s LNG exports for Europe—a beneficial backstop if, as feared, Putin cuts off more EU nations’ gas flows later this month.

[i] “More of Europe’s Crude Supply Is Coming From Deep in the Heart of Texas,” Arathy Somasekhar and Stephanie Kelly, Reuters, 4/29/2022. Accessed via Nasdaq.

[ii] We would add that an export ban regardless of blend mismatch would be lose-lose, considering it would discourage production, which no one wants.

[iii]“EU Close to Deal on Russian Oil Phaseout; Hungary, Slovakia Object,” Emily Rauhala and Quentin Ariés, The Washington Post, 5/2/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today