Personal Wealth Management / Market Analysis

Time for a New Sector?

What if some Tech companies aren't really Tech?

Editors' Note: MarketMinder does not recommend individual securities. The below merely represent a broader theme we wish to highlight.

Is Facebook a Tech company? Most folks would say yes. It's a dot-com, after all. Presently, index providers agree. But MSCI and S&P Dow Jones are mulling moving it to a new sector-Communication Services-along with Telecom, some Consumer Discretionary firms and a few other Tech companies. While far from final, this proposal is an interesting idea highlighting economies' and markets' evolution. Moreover, it shows the importance of assessing whether a security you're considering is really likely to trade like its peers.

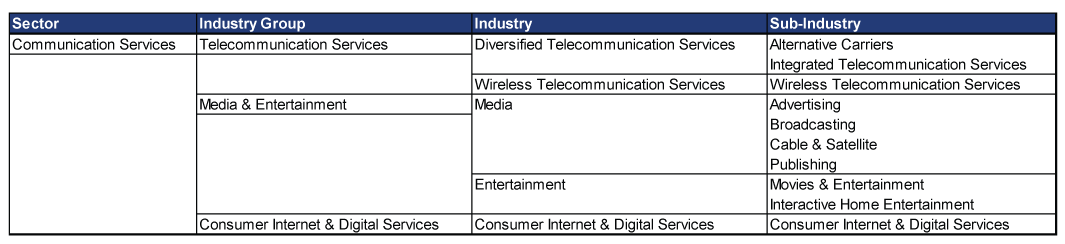

The new sector would reconfigure the Global Industry Classification Standard (GICS)-the sector roadmap used by many, if not most, indexes. The Telecom sector would become an industry group in Communication Services. So would the Media Industry Group, which would move from Consumer Discretionary and get a new name-Media & Entertainment-comprised of two constituent industries intuitively called "Media" and "Entertainment." Another new industry group-Consumer Internet & Digital Services-would include companies like Facebook, Alphabet (Google) and others mostly in Tech today. Exhibit 1 shows how this new sector may look.

Exhibit 1: The Would-Be Communication Services Sector

Source: MSCI.com, as of 7/26/2017.

These changes would modernize GICS, which hasn't kept pace with how media and technology have evolved-or how firms have changed their business models to compete. Firms with similar businesses now exist in different sectors. For example, Comcast is in Consumer Discretionary while AT&T is in Telecom-yet there is a ton of overlap across the two businesses. "Mainstream media" is presently in Consumer Discretionary, but others that communicate information and generate significant revenue from advertising-like Google and Facebook-are part of Tech. There is some logic to making GICS better reflect these similarities.

Logical or no, this may not happen. When considering big index changes, MSCI and S&P Dow Jones seek input from the investment community. The index providers want actual users' views on eight "discussion topics." For example, should search engines, social media and mobile messaging stocks be in Communications Services? Should revenue generation-the current method-drive classification? Or is the platform used to conduct operations a better determinant? Should this new sector maintain the historical returns/characteristics of the Telecom sector, or should they strike it and start anew? Investors will weigh in on these and other questions from now through September. MSCI and S&P aim to decide by November.

For now, our main takeaway is that it highlights questions about sector classification, which like most of investing, is more art than science. Is the current system logical? Sure. Is the proposal also logical? Yep. But even beyond that, there are plenty of other unaddressed grey areas. Should Apple be in Tech or Consumer Discretionary-maybe in the Retailing industry? After all, it has hundreds of retail stores and generates most revenues by selling products and digital entertainment. What about Amazon? It is now in Consumer Discretionary, but cloud computing-software as a service-is a big part of its business, making it compete directly with Tech firms. It also sells groceries, in case you hadn't heard, competing with Consumer Staples. Even some firms that seem like a perfect fit in a sector may not be. McDonald's is Consumer Discretionary, right? Not so fast. Some say it operates like a REIT! Don't judge a book by its cover. Regulatory matters also influence securities. With the FCC now regulating ISPs as public utilities, will these firms correlate more with the Utilities sector? Time will tell, assuming the regulation stands. If so, should they be classified with them?

All these situations require investors to analyze securities to determine if they really fit their home sector's themes. Stocks in an industry may not be as similar as labels might suggest. The issue here is simple: Let's say you identify a reason to think sector X will outperform. If you buy stocks that don't trade anything like X overall, you may not benefit from the driver you identified.

Beyond these issues, sector classifications and changes aren't market drivers. Usually, they're backward-looking responses to industry changes or past performance. Real Estate, for example, became a sector in 2016 after outperformance drew investors' attention. Since then, it has faltered. Similarly, index providers created the GICS system in1999 in part to make Tech its own sector (so investors could more easily chase heat, we guess). While we can say now this added value, investing based on some interpretation of the change could have proven costly when the dot-com bubble burst. So consider these proposals for what they are: A reminder about markets' continual evolution-and a warning about potential outliers.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the Iran Flare Up2026-07-08

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Market Analysis Can Germany Engineer Faster Growth at Last?2026-07-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today