Personal Wealth Management / Market Analysis

To Markets, the Brexit Vote Is Largely Over

While question marks remain, markets have already dealt with most of the uncertainty over June 23's vote.

Another day, another round of sensational headlines about Brexit. The Leave campaign is in uproar over the government's decision to extend the voter registration deadline from Tuesday night to midnight on Thursday, accusing them of trying to "skew" the outcome. New Bank of England data revealed investors pulled £65 billion from UK assets in March and April, the biggest outflows since the financial crisis. George Osborne didn't utter a peep about April's huge industrial production growth, earning accusations that he's ducking data that don't fit the Remain campaign's narrative. And of course, the warnings of economic and stock market calamity in the UK and Continental Europe if voters choose Brexit on June 23 keep flooding in. No doubt, if Leave wins, there will be question marks-it is unrealistic to think otherwise. Yet the sheer flood of warnings and competing opinions-omnipresent for the better part of a year now-has done investors a favor: It has let markets price in much of the uncertainty, helping reduce the potential for a surprise if Leave wins.

Markets' efficiency with matters like this is self-evident if you see it in action, so here are some charts.

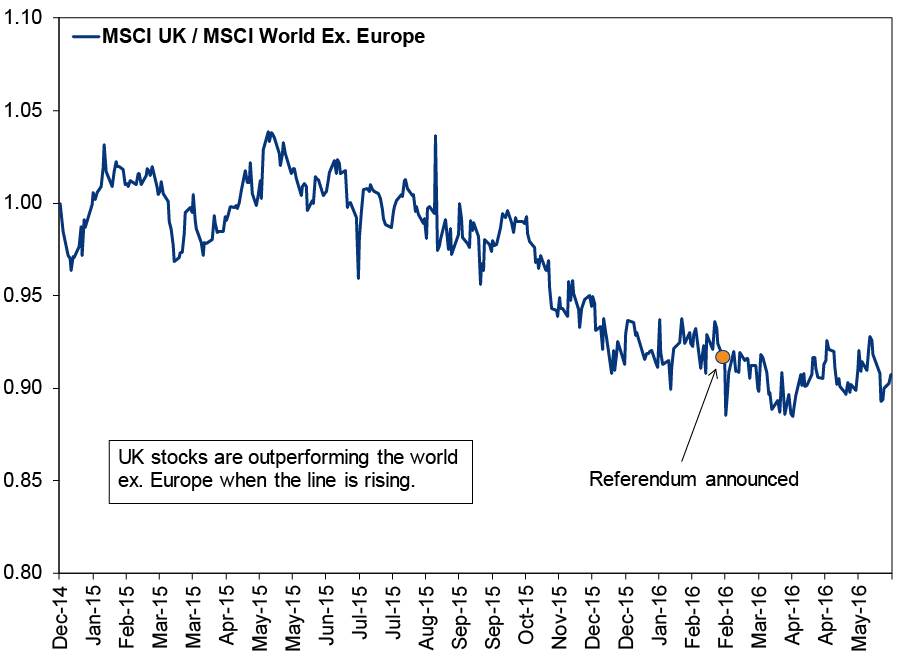

Exhibit 1: MSCI UK Versus MSCI World Ex. Europe

Source: FactSet, as of 6/8/2016. MSCI UK and MSCI World Ex. Europe Indexes with net dividends, 12/31/2014 - 6/7/2016. Indexed to 1 on 12/31/2014. Note that this is excluding Europe and not excluding the eurozone or EU, which are both different.[i]

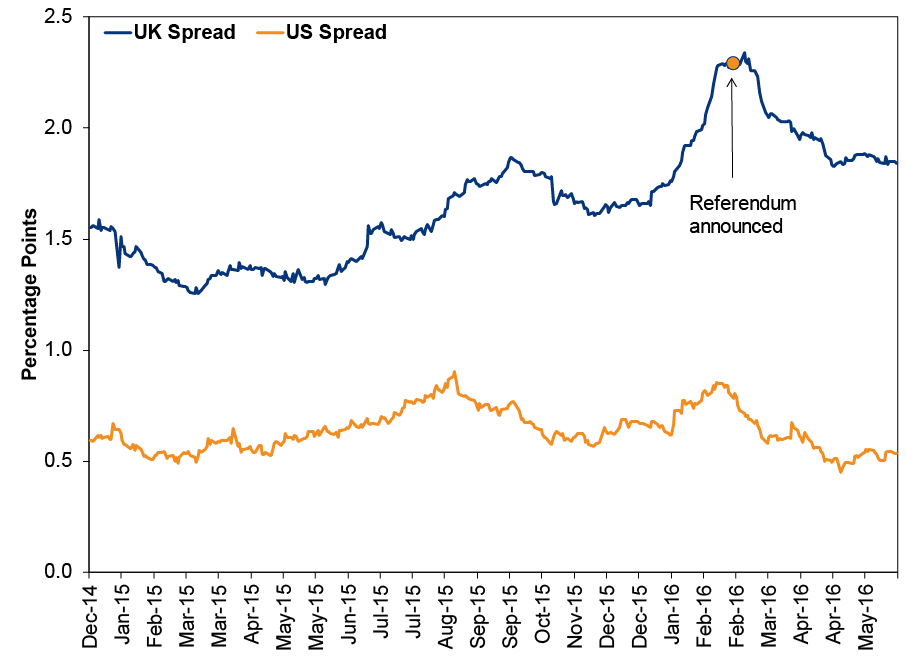

Exhibit 2: Corporate Debt Spreads

Source: FactSet, as of 6/8/2016. BofA Merrill Lynch Sterling Corporate & Collateralized All Stocks UK Issuers (7-10 Y) Effective Yield minus UK Benchmark Bond 10-year yield and BofA Merrill Lunch US Corporate (7-10 Y) (AAA) Effective Yield minus US Treasury Constant Maturity 10-year yield, 12/31/2014 - 6/7/2016.

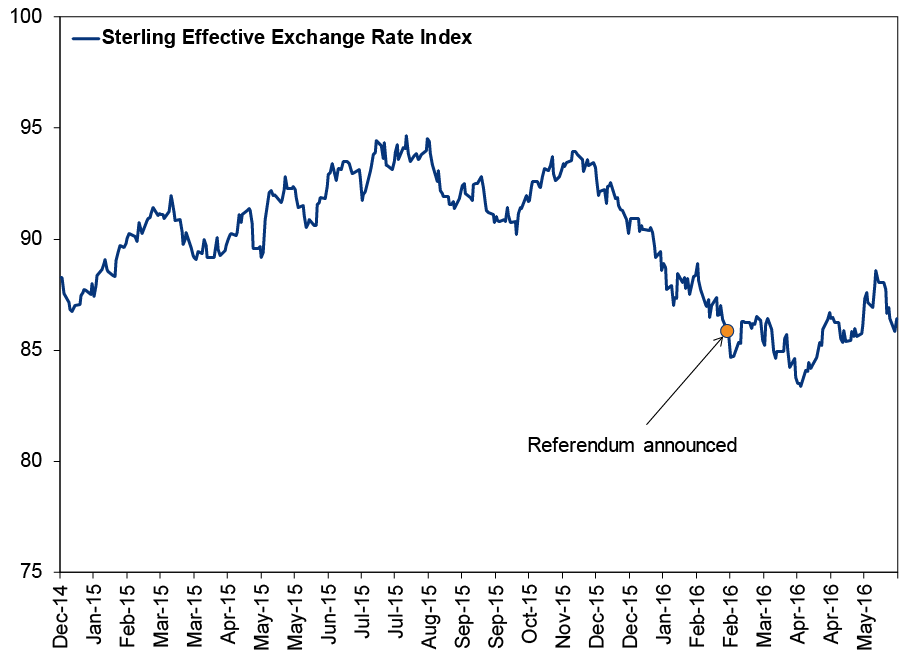

Exhibit 3: The Pound

Source: FactSet, as of 6/8/2016. Bank of England Sterling Effective Exchange Rate Index, 12/31/2014 - 6/7/2016.

In all three cases, much of the volatility occurred before February 20, the day UK Prime Minister David Cameron scheduled the referendum. Markets paid close attention to Cameron's negotiations with EU leaders in the preceding months. They saw the occasionally narrow polls and rising tide of Brexit warnings. During that period, the UK underperformed the non-European world[ii], UK firms' funding costs jumped and Sterling weakened. Since then, however, despite the increasingly heated campaign, markets have settled. UK stocks are choppy but roughly even with the non-European developed world. UK corporate debt spreads have narrowed considerably, even though they're elevated relative to the US. The pound has seesawed but is more or less where it was when Cameron made his announcement. None of this means there won't be any volatility should Leave win, but taken together, these charts strongly suggest markets have dealt with much of the uncertainty. Surprises move markets, and with folks reading so much into recent polls, a vote for Brexit wouldn't qualify as a surprise.

Markets hate uncertainty above all else, so resolving the stay-or-go question should bring relief. If Remain wins, then the status quo persists. Britain has done pretty darned well since joining the European Economic Community in the mid-1970s. If Leave wins, there will be some issues to work through, but those issues will take time, and markets will deal with them much as they've dealt with this referendum-pricing in worst-case-scenario warning after worst-case-scenario warning well before anything actually happens, then sighing with relief if the outcome is less disastrous than advertised. A lengthy, public, contentious EU exit negotiation process might weigh on sentiment, but it shouldn't cause a bear market-see the eurozone's slow-moving efforts to reinvent itself after the debt crisis for proof. Existential questions seem vast, but they become part of the long-term backdrop. Investors see life going on in the meantime, and markets get on with it.

Some post-Brexit questions are already starting to come into focus. For instance, Cameron and Scottish First Minister Nicola Sturgeon have warned a Leave vote could trigger another Scottish independence referendum, particularly if a majority of Scots vote Remain. Northern Ireland would also have some decisions to make, as its economy is increasingly intertwined with its southern neighbor. The potential return of border controls between the North and the Republic would be critical. So would trade. The UK would have ample time to renegotiate trade relationships, but as World Trade Organization chief Roberto Azevêdo has pointed out, the UK lacks the institutional capacity to start this right away. The EU has negotiated all Britain's trade deals for decades, and finding and hiring qualified trade reps will take time. It's doable, but a process.

None of these issues will be resolved overnight. All will probably create winners and losers. Some might bring profound societal change. But for markets, the question isn't whether things go well or poorly. Rather, it's whether there is a sudden, negative shock. Considering the amount of publicity and scrutiny over these and many other questions-and how long they'll take-it's highly unlikely a huge negative would strike without warning. Instead, we'll probably get leaks, rumors, speeches, summit meetings, more leaks, more rumblings, more summit meetings and, eventually, compromises. Who knows what those compromises will entail! But leaders in the UK and Europe must answer to voters, giving everyone involved a huge incentive to avoid snap decisions and sudden changes. Love or loathe the results, the process is a blessing for markets.

Should Leave win, expect a media circus, and remember: Anyone claiming to know precisely what will happen is speculating. No one can know today whether the UK will break up if it Brexits. Or which countries it will trade freely with. Or what its relationship with the EU will be. Or whether Cameron will remain Prime Minister. Or who will replace him if he doesn't. Pundits have spilled countless pixels on these topics, and they will spill many more-but they are all just guessing. There are dozens of possibilities, but markets move on probabilities. It will take time for those probabilities to form, which is all the more reason to avoid hasty portfolio moves. Investors will have time to assess the situation.

If Remain wins, the preceding four paragraphs will be moot. But in the meantime, the next two weeks could be rough. Expect more odd leaks like the one stealing headlines on Monday, when unnamed MPs told the BBC they'd do their best to override a Leave vote in Parliament, driving fears of a "Constitutional crisis." Expect more campaigning masquerading as analysis, like the essay from pro-Brexit Justice Secretary Michael Gove claiming negotiations over an EU exit would start years after the vote, despite Cameron's claims otherwise, and the UK would continue enjoying all the EU has to offer in the interim. Not to pick on the Right Honourable Gentleman, but for investors, it's crucial to see politicking for what it is. That's how you keep a level head when campaigns get crazy. Case in point: One could rationally interpret Gove's missive as evidence Brexit would be far less disruptive than many fear-or as evidence it would be even longer and messier than people think. It cuts both ways. We're inclined to chalk it up as an attempt to win over fence-sitters who don't want to give up the benefits of EU membership.[iii] That's an issue for voters to deal with, not investors.

We don't write any of this to influence voters-we're neutral. Bias toward either side is blinding. Our aim here is simply to help investors cut through the noise and sensationalism and understand what will matter for markets, so they can avoid costly errors. By all means, have strong opinions about the societal implications of staying in or leaving the EU. But firewall the investing portion of your brain from those opinions and emotions.

[i] We excluded Europe to remove skew from related worries over how Brexit would impact the other 27 EU nations, as well as the union's future. Unfortunately, this series unnecessarily removes Switzerland (which isn't in the EU), but MSCI doesn't make a World Ex. EU index. Rock, hard place.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today