Personal Wealth Management / Market Analysis

Top-Down Lessons From Energy

As the Energy sector’s experience this year shows, most stocks with similar drivers should be expected to behave similarly.

Editors’ Note: MarketMinder doesn’t make individual security recommendations; references to individual firms in the commentary that follows are simply made to illustrate a broader point.

Most financial media focuses on individual companies: Stories about executive leadership shifts, last quarter’s earnings, product issues or lawsuits often dominate. This is all fine, and individual security factors are no doubt important to weigh. But it downplays a key point, in our view: Drivers at the sector, country, industry or style levels often matter much more than stock-specific factors. We think investors would be well served to take note that similar stocks usually—and should—behave similarly.

Take, for example, the Energy sector. Most of the firms in this sector are heavily exposed to oil prices. Some directly, given they explore for oil. Others are more indirectly exposed: Perhaps they are natural gas producers, but since gas is often a byproduct of oil exploration, oil production trends exert plenty of influence on gas prices. Globally, the sector has only a few firms with no direct or indirect exposure to crude.

So when oil prices tanked earlier this year tied to oversupply and faltering demand due to the economic lockdowns, Energy stocks tanked categorically, too. The MSCI World Energy sector has had 55 consistent constituent companies since the index hit its year-to-date high on January 6.[i] From then through its March 18 low, the sector fell -59.5%, far exceeding global stocks’ overall -28.6% decline over this span.[ii] Of the 55 constituents, 54 were down. 51 underperformed the world and 28 underperformed the sector. The one stock that rose was Cabot Oil & Gas. What was bad for the Energy sector was pretty much bad—to varying degrees, of course—for all the stocks in it.

From the low through April 29, Energy stocks rallied—posting 59.8% gains.[iii] Over this span, the MSCI World rose 23.4%.[iv] Of Energy’s 55 constituents, 54 were up, 49 outperformed the World and 26 topped the sector. The high return was 184% and the low -0.5%.[v] Prior “winner” Cabot Oil & Gas was the third-worst performer in the group, while the sole decliner was Australia’s WHSP, although this firm is pretty far from a pure-play energy company. The uptrend for the sector was pretty broadly good.

Since then, Energy stocks—classic value plays—have seen their rally flatten out, falling -2.9% from April 29 through August 4.[vi] Meanwhile, World stocks have climbed 13.3%.[vii] Over this span, most Energy constituents are, like the sector, lagging. Only 10 are outperforming. One of those: previous laggard WHSP. Cabot Oil & Gas fell -5.0%.

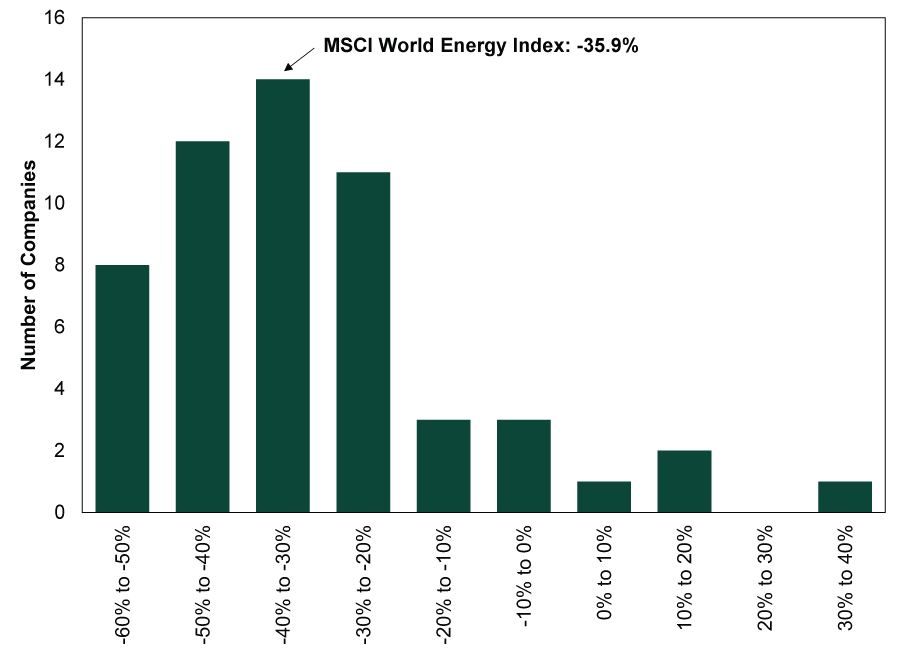

To sum up: On the year, the Energy sector is down -39.5% through August 4 and there are very, very few outliers, as Exhibit 1 shows.

Exhibit 1: Bell Curve of MSCI World Energy Sector Constituent Returns, Year to Date

Source: FactSet, as of 8/5/2020. Returns cited are total returns in USD. 12/31/2019 – 8/4/2020.

Cabot is one of those stocks that are up. WHSP is down slightly, but good enough to finish fifth in the sector. But as our earlier dissection shows, these good year-to-date returns versus their sector belie the experience throughout. Chasing these outliers could have burnt you badly, compounding the damage the sector was experiencing overall. Other outliers include a uranium miner and an oil storage firm, whose drivers are obviously pretty different than the Energy sector’s at large. (Especially oil storage early this year, given the huge glut of oil put this at a premium.)

To us, the moral of the story is that most stocks with similar drivers mostly will and should act similarly. There are differences to an extent, no doubt. But they shouldn’t be gigantic, in our view, with the stocks you own bucking the overall trend for the category by a wide margin. In a diverse portfolio, that may counterintuitively mean owning stocks you aren’t expecting to outperform broad markets—and even ones that may not do well. Consider it an insurance policy in the event your broad expectations prove incorrect. That is diversification in a nutshell, and it can be frustrating. But a portfolio consisting of a bunch of outlier stocks that don’t reflect broad sector trends can easily mean one that behaves in haphazard ways you may not be able to anticipate or blend into a broad strategy.

[i] Source: FactSet, as of 8/6/2020.

[ii] Ibid. MSCI World Energy sector and MSCI World Index returns with net dividends, 1/6/2020 to 3/18/2020.

[iii] Ibid. MSCI World Energy sector return with net dividends, 3/18/2020 to 4/29/2020

[iv] Ibid. MSCI World Index return with net dividends, 1/6/2020 to 3/18/2020

[v] Ibid. High and low price return of MSCI World Energy sector constituent stocks.

[vi] Ibid. MSCI World Energy sector return with net dividends.

[vii] Ibid. MSCI World Index return with net dividends.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01 -

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today