Personal Wealth Management / Market Analysis

Trade Truce?

China and the Trump administration’s weekend handshake, like the tariffs it suspended, is mostly symbolic.

Did you hear? The US – China trade war is off! China agreed to improve intellectual property protections and buy an unspecified large amount of US-made goods, primarily from the agricultural arena, and both sides agreed not to pursue new tariffs at this time. That means the Trump administration’s tariffs on $50 billion of Chinese goods, China’s retaliatory tariffs on $50 billion of US goods, Trump’s mooted retaliation-to-the-retaliation of tariffs on $100 billion of additional Chinese goods, and China’s mooted retaliation-to-the-retaliation-to-the-retaliation of tariffs on $100 billion more US goods are all on ice. For now. Markets seem happy with this development, and far be it from us to quibble with a happy stock market. But this also strikes us as much ado about nothing—the “resolution” is as symbolic as the tariff threats were. China’s vague promises probably amount to very little actual change in bilateral trade. On the bright side, getting past the stalemate could give investors one less thing to worry about, perhaps lifting sentiment and helping folks move out of the correction mindset.

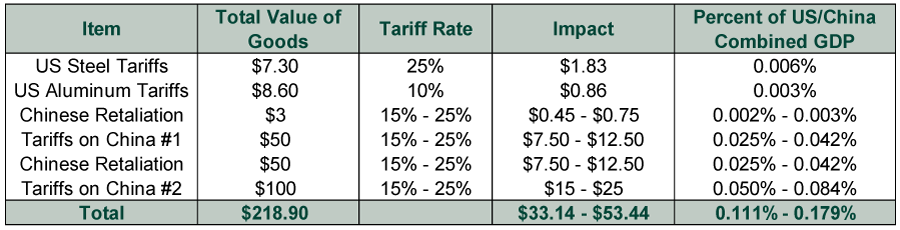

As Exhibit 1 shows, the direct impact of all tariffs adopted and threatened so far would have amounted to, at most, $53.44 billion, or just under 0.2% of combined US and China GDP. For the US alone, the impact would have been $40.2 billion. That sounds big, but in 2017 alone, nominal US GDP grew by $766.1 billion.[i] The new tariffs, on their own, would have been nowhere near enough to sink the US into recession. Not having them will be nice, but it isn’t some whopping positive—just the absence of a tiny potential negative folks have overrated for months.

Exhibit 1: Scaling the Tariffs

Source: US Trade Representative, China Ministry of Commerce, World Bank, as of 4/10/2018. Estimates of steel and aluminum tariff impact exclude imports from exempted countries and will likely remain in effect, as they do not appear to be part of Saturday’s deal. GDP figure used is nominal 2016 GDP, the latest available for both countries.

China’s weekend concessions appear similarly small. Pledging to better protect US firms’ intellectual property is all well and good, but it is also something China’s government has pledged before, and their latest pronouncement lacked details. Short of their removing the requirement for foreign firms to surrender trade secrets in order to do business in China, it is difficult to envision meaningful change.

Pledges to purchase more US-made goods in order to reduce the bilateral trade deficit probably fall similarly short. Though they haven’t agreed on an amount yet, the number flying around on Friday was $200 billion. Problem is, the US exported just $130 billion in goods to China last year. More than doubling this figure in short order is unrealistic unless it involves diverting shipments from other countries to China—nearly impossible to direct in a private sector-led economy like America’s. (Not to mention, the impact on actual US output would be zero sum.) A Monday Trump Tweet implied most of the increase will come from agricultural products, but total nominal GDP in the agriculture, forestry, fishing and hunting industry last year was just $169.1 billion. We daresay farmers aren’t going to suddenly divert all that production and then some to China. Perhaps Saturday’s breakthrough causes them to plant more soy next spring, but probably not tens of billions of dollars’ worth. The US exported about $22.4 billion dollars’ worth of soybeans last year, with an estimated 62% going to China.[ii] The USDA reports farmers have planted about 89 million acres of soy this year, and one out of every four rows planted already goes to China. Is a handshake deal among bureaucrats really going to be the impetus for farmers to devote millions upon millions more acres to soy?

Similarly, administration officials hinted at raising liquid natural gas (LNG) exports to China. Theoretically, this is more feasible than ramping up farm exports, as the US shale industry has long dealt with a huge natural gas surplus. However, the US doesn’t presently have the infrastructure to ship tens of billions of dollars’ worth of natural gas to China each year. Total natural gas exports last year were just $15.4 billion. Currently, the industry has capacity to liquefy 2.8 billion cubic feet per day (Bcf/d). The EIA projects five projects currently under construction will raise that to 9.6 Bcf/d by next year’s end. But China will have to continue competing with Korea, Mexico, Japan and Europe for its share of US exports. Considering the US government does not own domestic LNG production, it cannot mandate that all new output gets loaded on China-bound tankers. Perhaps higher demand from China does eventually spur the development of more export-related LNG infrastructure, but it likely wouldn’t come online for years.

Some observers interpreted China’s lack of concrete pledges—and the Trump administration’s apparent willingness to settle for squishiness—as a sign of the administration losing leverage. But this is completely speculative. Unless you bugged the Beijing delegation’s hotel room, there is roughly zero way to know how much leverage the Trump team really has. This is also a sociological concern, the sort of thing markets generally don’t care about. It is cocktail party chatter, not a driving force for US or global corporate profits.

Again, we aren’t trying to throw cold water on good news. Simply ending trade war chatter could be just the boost investors’ animal spirits need. But the actual economic impact of this new deal will probably turn out to be quite small. If this proves to be the end of trade war rhetoric, it seems to us a fitting symbolic end to a quite small, symbolic “trade war” that never even began.[i] Source: FactSet, as of 5/21/2018.

[ii] The 62% figure refers to fiscal 2016/2017, not calendar-year 2017, but it is the best we can find and still useful for illustrative purposes.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today