Personal Wealth Management / Market Analysis

Trump Didn’t Make Small Cap Great Again

The Trump Trade, to the limited extent it existed, ended eight months ago.

In assessing markets, media still places too much emphasis on the occupant of this building. Photo by JT Sorrell/iStock.

This article touches on politics, a wee bit of a charged subject these days. Please understand our commentary is limited to how political developments influence markets. We favor no politician nor any party.

It seems someone keeps forgetting to alert media to the not-so-breaking news that the Trump Trade isn't what's driving markets. With each passing day, headlines continue to claim the Trump Bump is morphing into a Trump Slump right before our eyes-with many presuming this spells trouble for stocks generally. The latest fixation: Small cap. From July 25 through August 21, the Russell 2000 (an index of teensy US stocks) fell -6.4%, putting its cumulative return since Election Day at 14.8%.[i] Or, said differently, putting its return behind the S&P 500 and S&P 100 (an index of yuuuuge US stocks) since Election Day. Journalists seized upon this and churned out the slew of articles we just linked to claiming a once-resilient Trump Trade is giving way. Look out below!

Or not. You see, Trump Trade logic is flawed. Unlike most sector and country performance data-which show little influence from the election-US small cap is one area where the election seems to have affected returns. But take this to heart: That period was fleeting. It ended on December 8, 2016. The huge majority of it ended November 14, 2016. The broad, global equity market rally-quite obviously-didn't. The fleeting small-cap pop after last year's election is yet more evidence Trump Rally theory cannot explain the good returns thus far in 2017. Hence, fearing a Trump Slump looms doesn't make much sense, in our view.

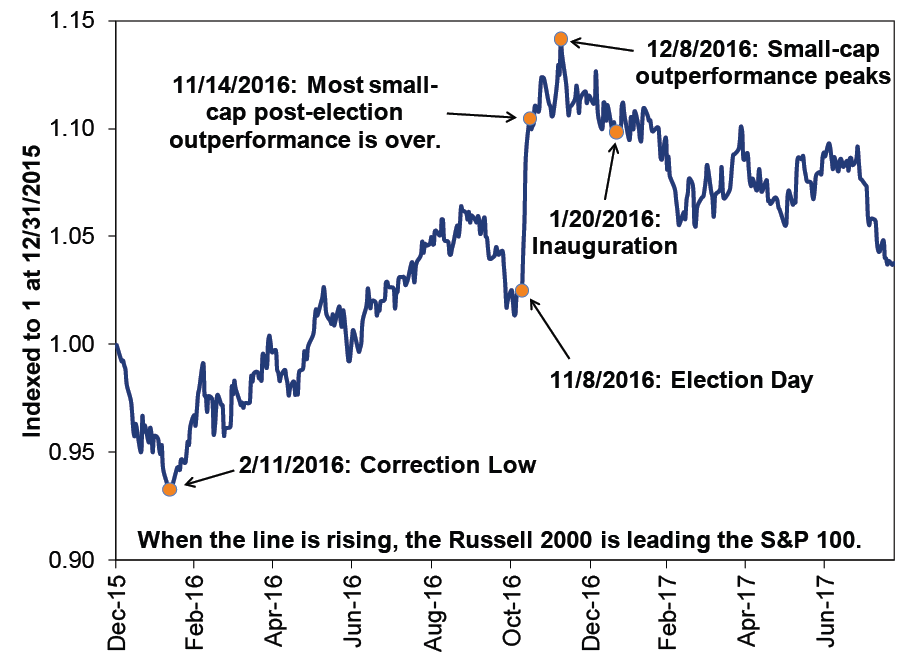

The case for a small-cap Trump Bump held that his stimulus plans, tax cuts and deregulation would benefit these firms substantially. Meanwhile, proponents theorized Trump's protectionism would ding big multinationals more than primarily domestically oriented small firms. Obviously, none of this has happened at this juncture, which you may interpret as explaining why small cap has faltered. But take note! Small cap's jump was over before Trump was eveninaugurated. Exhibit 1 plots the Russell 2000's returns divided by the S&P 100's from December 31, 2015 to August 22, 2017.

Exhibit 1: If There Was a Small-Cap Trump Trade, It Has Been Over for Months

Source: FactSet, as of 8/23/2017. Russell 2000 Index and S&P 100 Index total returns, 12/31/2015 - 8/22/2017.

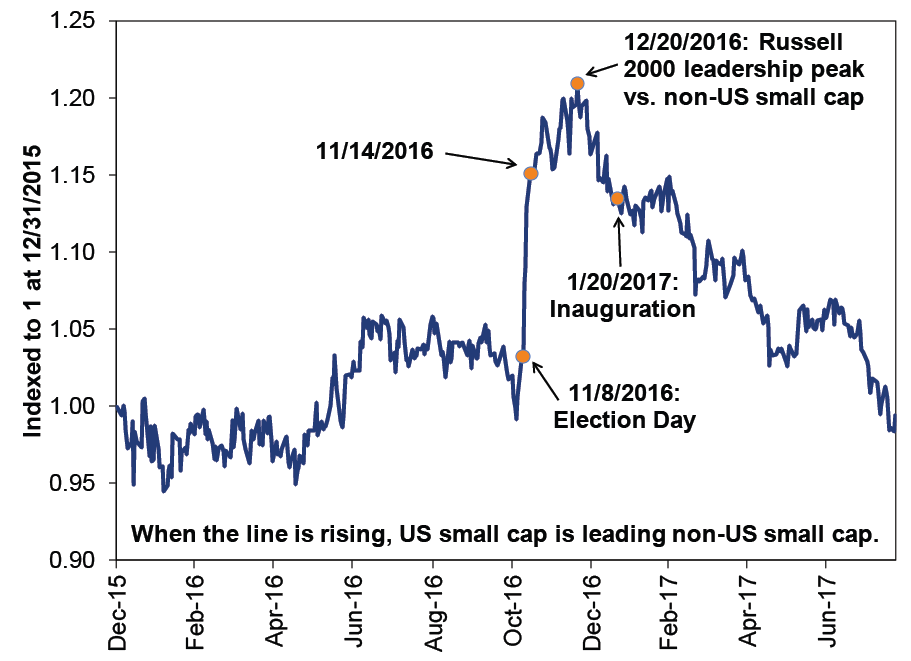

Obviously, the pop up around the election-and slump thereafter-stands out. However, the Russell 2000 was actually outperforming during much of the period after February 11, 2016's correction low. Which makes sense! The Russell fell much more than the S&P 100 during the correction. A big bounce back-relief rally-when Energy and China-related fears proved overblown seems a logical explanation for this aspect. But it isn't a full explanation. Were that the case, one would expect small-cap outperformance to extend to non-US stocks, too. Yet that didn't happen. Exhibit 2 shows the Russell 2000 versus a gauge of teensy non-US stocks (the MSCI World Ex. US Small Cap Index). You'll notice the post-election reaction looks strikingly similar to Exhibit 1.

Exhibit 2: US Small Versus Non-US Small

Source: FactSet, as of 8/23/2017. Russell 2000 Index with gross dividends and MSCI World Ex. US Small Cap Index with net dividends, 12/31/2015 - 8/22/2017.

All this leads us to a conclusion we've shared here before: To whatever extent there was a Trump Rally-which doesn't seem like that great of an extent, in our view-it was a short-term, sentiment driven move lasting a few weeks. It ended well before 2017 began.

Yet global equity markets have had a stellar year thus far. A non-US-led stellar year, that is. It is really hard to argue Trump's winning-and proceeding to be stymied by intraparty gridlock-is super bullish for Austria, Denmark and Spain. Yet those nations are among the best performers this year while the US is near the bottom. There is no sign of a Trump Trade in these data.

If the Trump Trade doesn't explain the rise, we figure you can look askance at media claims a lack of big legislation or regulatory reform (or or or!) will smack stocks. If a Trump Bump didn't boost stocks, there is little logic in fearing it will soon turn into a Trump Slump.

[i] Source: FactSet, as of 8/23/2017. Russell 2000 total return, 7/25/2017 - 8/21/2017 and 11/8/2016 - 8/22/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today