Personal Wealth Management / Market Analysis

Two Charts and Some Thoughts on Manufacturing

Don't overrate any one month of data, good or bad.

It's the first of September, and you know what that means-a new round of manufacturing surveys! Last month we flooded you with 29 countries' worth of data to show global manufacturing appeared to be on an upswing. This month, lest we write more or less the same story again, we'll zero in on two: America and Britain. One was not so great. The other was smashing. Both are worth noting, but we'd suggest investors not get hung up on either, for good or ill. One month does not a trend make.

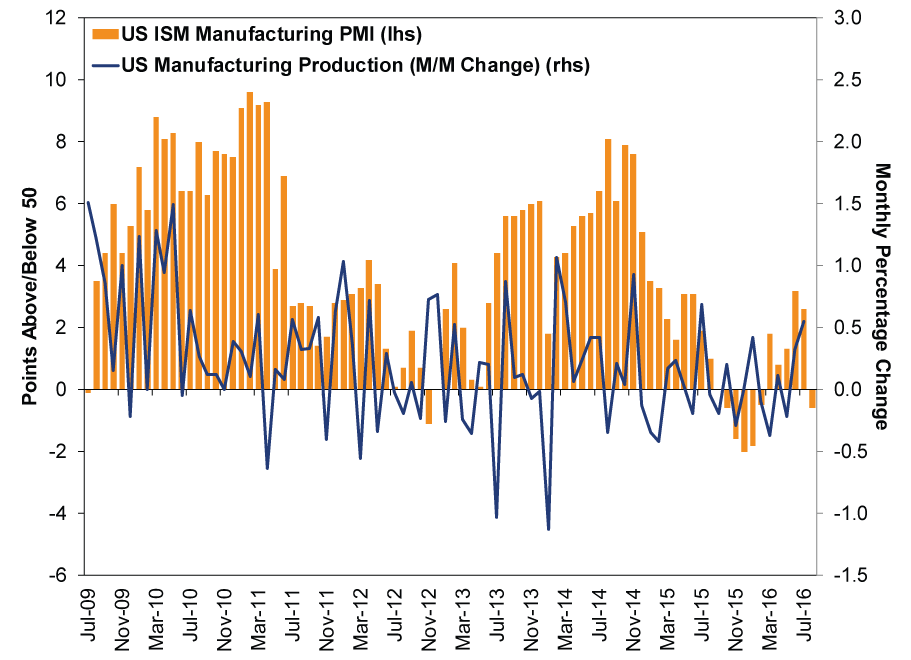

First up, America, where the Institute for Supply Management's August Manufacturing Purchasers' Index (PMI) slipped to 49.4, implying contraction, as all PMIs under 50 do. This snaps a five-month growth streak, and forward-looking new orders contracted as well. Now, this doesn't mean heavy industry actually shrank in August. PMIs measure how many firms grew, but not how much each grew. If fewer than half of the surveyed businesses saw higher activity, but they grew a lot more than the majority shrank, then the net result could very well be growth. PMIs are quick, fuzzy estimates, not airtight calculations. Then again, even if actual industrial output did slip, it should hardly signal the death knell for this expansion. As Exhibit 1 shows, the Manufacturing PMI shrank for five straight months in late 2015/early 2016, while manufacturing output mostly contracted. Yet the economic expansion didn't end. GDP slowed somewhat, but it still grew, with services and consumption doing the heavy lifting. Since manufacturing is only about 12% of GDP, isolated weakness there generally isn't enough to tip the economy into recession. It's a headwind, but surmountable.

Exhibit 1: US Manufacturing PMIs & Industrial Production

Source: FactSet, as of 9/1/2016. ISM Manufacturing PMI, July 2009 - August 2016; Manufacturing Output, July 2009 - July 2016.

Plus, August could easily be an anomaly. For what it's worth, ISM's factory survey chairman, Bradley Holcomb, thinks it is, as survey respondents' comments just aren't consistent with widespread trouble. "Strong demand" and "good business" were popular phrases, as were "sales increased." Again, PMIs are just kinda quirky. We wouldn't be at all surprised if August's dip were a quirky blip.

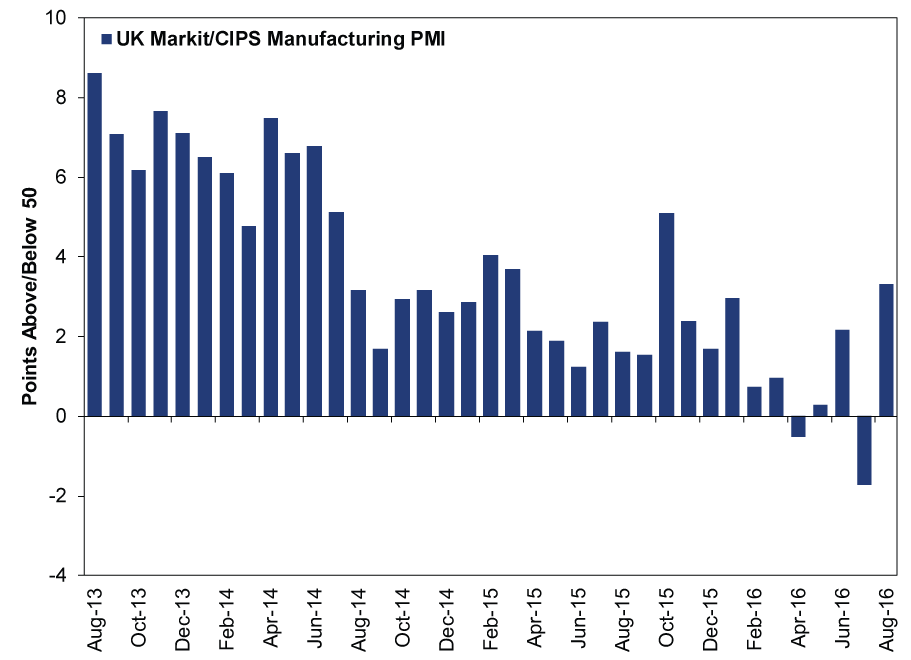

As for the UK, where August's PMI looked utterly smashing, we'd be hypocritical if we told you to get excited. So we won't. One month is just one month. Then again, the jump to 53.3 follows July's sudden, post-Brexit-vote dip to 48.3, and it's fairly consistent with the longer-term trend of growth, as Exhibit 2 shows. Far be it from us to debunk one isolated bad month with one isolated good month, but we're comfy calling this preliminary evidence that July's dip was a sentiment-induced one-off. We won't draw conclusions, as that would be hasty without a few months' more data, but it's an encouraging start.

Exhibit 2: UK Manufacturing PMI

Source: FactSet, as of 9/1/2016. Markit/CIPS UK Manufacturing PMI, August 2013 - August 2016.

Also encouraging: The component breakdown. New orders' rise was "among the steepest on record," according to the press release, a nice rebound from July's steep contraction. The presser also cites "reports of stronger demand, product launches and clients committing to new and previously postponed contracts." That last bit is crucial. The shock of Brits' decision to leave the EU in June clearly knocked the wind out of businesses, as shown in a number of sentiment surveys and July's PMI. That's totally normal. When something unexpected happens and seems to ratchet up uncertainty, it's natural to pause. Pretend you were a UK business owner in that environment, and you'd spent months reading report after report from various experts warning of a huge economic calamity if the Leave campaign won. You'd probably decide a bit of caution was in order, and ring up your suppliers to delay some orders you placed the week prior, when you thought Remain would win. It's the sensible thing to do! And then, once you saw your sales were steady and foot traffic was high-and you saw strong retail sales and consumer spending reports showing business was strong nationwide-you'd probably need to ring those suppliers back up and say, "let's get those shipments cooking, and add another few boxes of widgets and doodads while you're at it!" And then life would carry on as normal.

Again, we don't yet know definitively that this is what happened. It's early. Maybe we see a few more downticks if sentiment wobbles more. But August's comeback is consistent with the fact that nothing fundamentally changed for the UK's economy when the vote was over. Britain is still in the EU, trading freely with the other 27 EU nations and all their free-trade partners. Anyone with an EU passport can still travel freely to the UK and shop till they drop. Nothing will change until the exit is actually complete, which could take years. Until then, it's mostly business as usual.

Will future economic data confirm this? Maybe. Only time will tell. Overemphasizing August's jump would be as much of an exercise in confirmation bias as overrating July's plunge. Always beware behavioral errors! But not knowing exactly how the UK economy will react to the Brexit vote in the near term isn't a reason to make big portfolio changes. Markets discount all widely known information, including opinions and forecasts. Given how many people, think tanks and politicians warned of a post-vote UK recession, the potential for one is likely already baked into UK and global stock prices-and stocks are likely already looking further out, to the next 12-18 months or so, where most observers expect things to be more or less fine.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today