Personal Wealth Management / Market Analysis

Underappreciated Thursday

Signs of underappreciated positives in the US and Europe.

Thursday, the BEA revised Q3 US GDP from 2.0% to 2.7% q/q annualized. The revision primarily reflected positive contributions from higher inventories and exports. Although the result was slightly below expectations of 2.8% q/q annualized, in our view, it’s a reaffirmation of the underappreciated strength of the US economy.

While not gangbusters, Q3 was a reacceleration from previous quarters. Nevertheless, some folks point to a downward revision to consumption and high inventory components to mean future growth will slump. As the thinking goes, fearful consumers will curtail spending and businesses (saddled with high inventories) won’t need the same level of production to meet demand. But consumption is regularly more resilient than many expect, and although the revised Q3 consumption post was lower than the initial estimate, it still reflects growth (1.4% q/q annualized). In fact, consumers aren’t so “tapped out” as widely billed—consumer spending continues to be near all-time highs. Incomes are rising. And household debt service as a percent of disposable income is near 15-year lows.

Photo: Getty Images.

Likewise, businesses with high inventory levels are likely cognizant of near-record high corporate revenues in the US and are preparing for continued future demand. Thursday’s BEA release revealed another widely underappreciated factor: US businesses are quite strong. Even when adjusted for inflation, US corporate profits reached a record high.

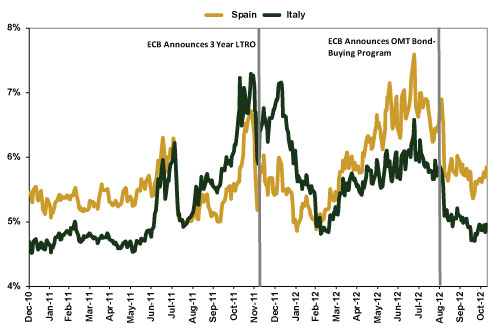

Another underappreciated Thursday story: the eurozone. Following a likely resolution to the Greek bailout debate earlier this week, Italy auctioned bonds at the cheapest levels in nearly two years. The auction raised a total of nearly €6 billion—€2.9 billion of 10-year bonds at yields of just 4.45%, down from 4.92% at a similar auction last month, and €3 billion of 5-year bonds at yields of just 3.23%.

Exhibit 1: 10 Year Sovereign Yields (Since 12/31/2010)

Source: Thomson Reuters.

Likewise, Spanish bond yields sank to their lowest levels in over eight months—yields on benchmark 10-year bonds dipped to 5.20%. In fact, Spain is already funding 2013 spending, and Italy is close to completing this year’s funding. The lower yields were particularly positive given their duration falls outside of the ECB’s three-year bond buying (LTRO) program window the countries relied on earlier this year to access debt markets at reasonable yields. Although these are minor improvements in the eurozone, they’re still signs of markets’ continued improving confidence in what to many has seemed a frustrating, drawn-out approach.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today