Personal Wealth Management / Market Analysis

Unemployment, Overall and on Average

Is a still-high unemployment rate that unusual?

The BLS’s US unemployment rate fell -0.4% in November to 8.6%—beating analysts’ estimates of no decline from October’s 9.0%—and putting the rate 2.8 percentage points and 3.0 percentage points above average and median unemployment (since 1948), respectively.

We’ve detailed many times the wonkiness of the unemployment rate’s calculation. It isn’t simply the number of Americans without work (defined by surveys of US households) divided by the estimated workforce. It is the number of out-of-work folks who actively sought jobs divided by the estimated workforce. That “actively sought” part creates a great deal of statistical noise—occasionally lowering unemployment as folks cease their search and increasing it when they resume. In Friday’s report, the household survey showed unemployed job-seekers fell by 549,000. Roughly half found work. About half stopped looking. So there’s something for everybody—job market bull or bear—in the data.

While the rate fell and hiring continued (both pluses) there’s no denying unemployment remains high. What else is high? The number of theories attempting to explain currently elevated unemployment. Some argue it’s too much regulation, jacking up the cost of hiring decisions and impacting employers’ confidence. Others argue many unemployed folks lack transferrable skills, limiting the opportunities they’re qualified for. Still others argue it’s a lack of labor mobility—unemployment plus underwater homes means laid-off workers face a difficult time relocating to areas where work is more plentiful. Still others point to productivity—indicating rising worker output means employers simply don’t need to hire as quickly to maintain overall factory output. Some just blame Democrats. Some Republicans. And there are more. (This is more a “best of” list than an all-inclusive snapshot.) And there’s possibly some truth to all in varying degrees. But none exclusively explain why unemployment remains elevated—or if still-elevated joblessness is historically unusual.

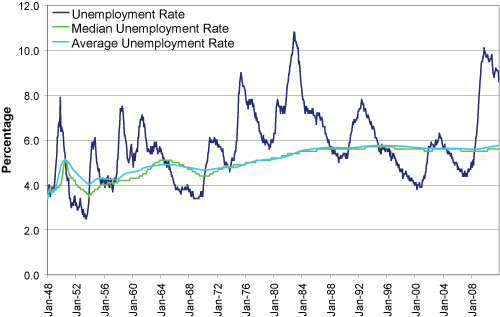

Yes, unemployment’s high. But if you’d like to gauge whether stubbornly high unemployment is unusual, step one would be understanding historical unemployment. Perhaps you’d compare past relative unemployment peaks to average unemployment. Or median unemployment. As we noted above, unemployment is above the simple average and median. But those metrics change slightly with every monthly release—so to know what folks may have considered elevated in the past, it’d be pertinent to know what was then average unemployment for comparison. Thus, Exhibit 1 below plots three things: headline unemployment, median unemployment through time and average unemployment through time.

Exhibit 1: US Unemployment Rate Versus Median and Average Unemployment Rate

Source: Bureau of Labor Statistics, January 1948 – November 2011.

Unemployment never reaches zero, but 4-6% is widely considered high rate of employment. And recent historical averages are within that range (though admittedly toward the high end). But what’s also easy to see is there’s a huge amount of time elapsed between relative unemployment peaks and the point unemployment nears the median and average. Of particular note: 1982’s 10.8% unemployment, which didn’t hit 6% until 1987. Nearly six years. Long! But economic growth continued throughout the six-year period, gradually working off unemployment. And that’s not unusual; it’s the norm.

So while we’d agree a healthier housing market (though we’d quibble with government attempts to “fix” housing), a lighter regulatory and tax climate and more could aid jobs through more growth, there’s little reason to believe the result would be an immediate reduction in a wonky statistic that nearly always takes a long time to fall. Ultimately, it would be far more atypical or unusual for unemployment to be at average or median levels today than its currently elevated state.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today