Personal Wealth Management / Economics

Unemployment with a Taper Twist

Unemployment improved slightly in August, but how this impacts QE tapering plans remains to be seen.

This is a tapir (with an I)—because we couldn’t find any visual representations of a taper (with an E). Photo by Marianna Massey/Getty Images.

Will they or won’t they? That’s what most headlines asked about QE tapering after August’s unemployment report—(drumroll) the last one before the allegedly pivotal September 17-18 FOMC meeting. Some say the falling unemployment rate means the taper is on. Others say the shrinking workforce and slower-than-expected payroll gains mean the taper is off. Our guess? Impossible to say—there isn’t much logic behind QE in the first place, so it’s tough to imagine plans for its end following gameable rhyme or reason. We believe the economy and markets will be better off when QE ends—whether tapering starts this month, later this year or 2014.

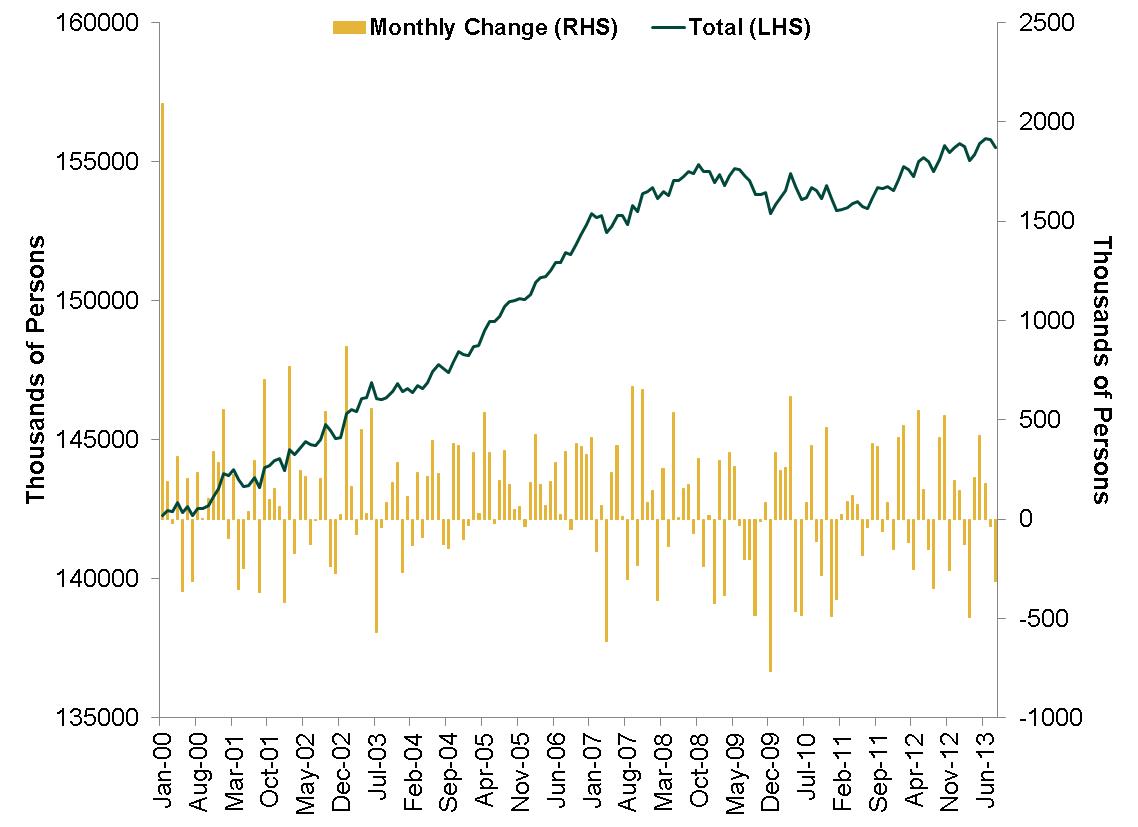

Those who do try to read the unemployment tea leaves probably won’t find many taper clues. August’s report was a rather mixed bag—slow improvement of headline data continued, while the underlying data varied. Overall, the results were largely in keeping with most employment reports since the recovery began. Unemployment dropped to 7.3%—still elevated, but better than the 8.1% of a year ago. Total nonfarm payrolls marked their 42nd consecutive month of growth—coming in slightly less than expected at 169,000 compared to the average estimate of 180,000, with the private sector contributing 152,000 jobs. But a larger driver of the falling unemployment rate was a 312,000 drop in the labor force—the second straight fall. Some say this means discouraged workers are leaving the workforce and suggests a weaker labor market, but labor force participation typically varies from month to month. The workforce has declined at times throughout the recovery, yet the civilian labor force is still over 2.6 million people higher than its December 2009 low and remains near all-time highs.

Exhibit 1: Civilian Labor Force

Source: Federal Reserve Bank of St. Louis, Bureau of Labor Statistics, as of 9/6/2013.

Even if the employment report were more conclusive, the Fed’s next move would be tough to handicap. Yes, Ben Bernanke told Congress tapering could start as early as September, but forward guidance doesn’t mean much—words aren’t set in stone, and plans can change. Plus, Bernanke has one vote on the FOMC. Different members have competing views, and Bernanke’s months-old testimony may or may not reflect the broader views of policymakers when they meet again next week.

What we do know, however, is this: Whether it happens next week, the next few months, or even in 2014, QE will start to wind down—a super bullish event, in our view. QE hasn’t had its intended impact on growth. The monetary base (M0) has risen over 250% since 2008, but the amount of money circulating through the economy (M2) hasn’t risen anywhere near as much. In order for QE to do much good, M2 needs to grow faster, which requires banks to lend more enthusiastically. But QE is a disincentive—it flattens the yield spread, reducing banks’ net interest margins. Reducing and eventually stopping bond purchases would allow long rates to rise, widening the yield spread and increasing banks’ potential operating profits—a greater incentive to lend. Then, more money would flow to the economy, likely boosting growth.

This is already happening in the UK, where QE ended late last year. Since then, the BOE’s balance sheet has shrunk a bit, but the money supply has continued growing. The UK yield curve has steepened, its economy has accelerated and stocks are up—powerful precedent for the US! Yet no one notices, heightening the bullish surprise potential once QE ends on our side of the Atlantic.

In short, the sooner QE ends, the better for markets and the economy, in our view—but whether tapering starts next week or next year, the bull market should continue apace with plenty of fundamental support.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today