Personal Wealth Management / Economics

US Durable Goods Still Strong

February’s capital goods orders missed estimates, but capital goods remain an economic bright spot.

February’s durable goods orders missed estimates, rising 2.2% over January versus expectations of 3.0%. Core capital goods, excluding volatile transportation and defense orders, also missed estimates, rising 1.2% versus estimates of 1.4%.

That may not seem terrific, but a closer inspection tells a different story—with core capital goods orders set to hit all-time highs. Most of February’s miss was due to an upward revision in January’s number—from -4.0% over December to -3.6% m/m. Core capital goods were also revised upward from -4.5% to -3.7% m/m. Again, January’s negative read may not seem great, but it was likely due to some near-term distortions. Thanks to the 2011 year-end expiration of tax rules allowing accelerated depreciation of capital goods, it appears likely there was some pull forward into the end of last year—pumping up year-end numbers at January’s expense.

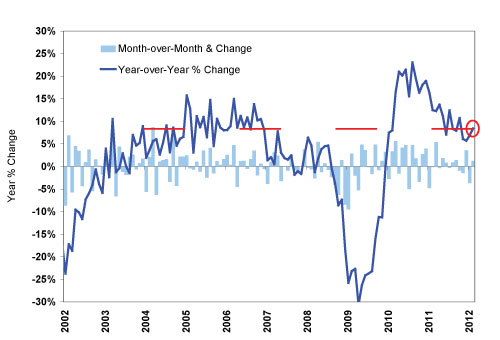

Month to month readings of any economic metric can be volatile and prone to unexpected distortions. Taking a longer view, it becomes clear durable goods orders remain strong. Exhibit 1 shows despite a recent deceleration, core capital good orders remain at the same healthy levels seen throughout most of the last bull market.

Exhibit 1: New Orders for Non-Defense Capital Goods Ex-Aircrafts (Core Capital Goods)

Source: Thomson Reuters, US Commerce Department.

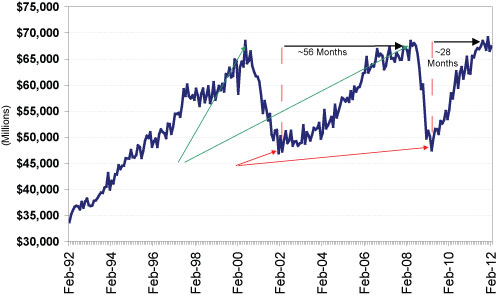

Further, Exhibit 2 shows capital goods orders have rebounded strongly off their 2009 lows, bouncing back to previous highs twice as fast as the last economic expansion. It seems the pace of growth in durable goods orders is returning to levels somewhat similar to the last economic expansion. However, the absolute growth appears set to break all-time highs and remain a bright spot for the US economy.

Exhibit 2: Growth in Core Capital Goods Orders (Ex-Aircraft and Defense)

Source: Thomson Reuters, US Commerce Department.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today