Personal Wealth Management / Market Analysis

US Q2 2011 GDP and a Word on Revisions

The US Bureau of Economic Analysis announced its first estimate of US Q2 2011 GDP Friday and its revisions to prior data.

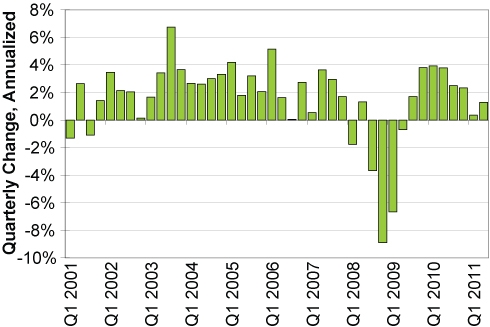

Friday, the BEA announced US real GDP grew at a +1.3% seasonally adjusted annual rate in Q2 2011, accelerating from downwardly revised Q1 growth of +0.4% (prior estimate was +1.9%). Consensus estimates called for +1.8% growth.

Exhibit 1: Real US GDP Growth

Source: US Bureau of Economic Analysis.

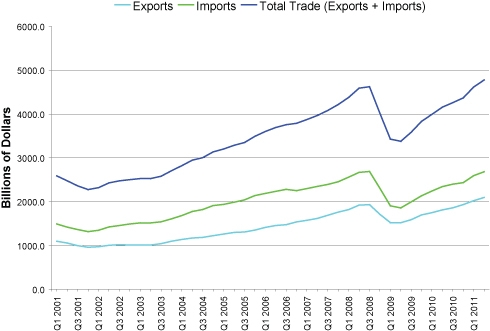

Already, many media sources are bemoaning the slow rate of growth, and there’s little reason to quibble—faster would be better, and this is clearly not the most robust GDP report ever. But let’s not overstate the case: The numbers do show growth and acceleration from Q1’s revised rate. In addition, total trade grew nicely at +3.5% as exports (+6.0%) andimports (+1.3%) both increased—a sign of a healthy global economy.

Exhibit 2: US Trade

Source: Bureau of Economic Analysis, Federal Reserve Bank of St. Louis.

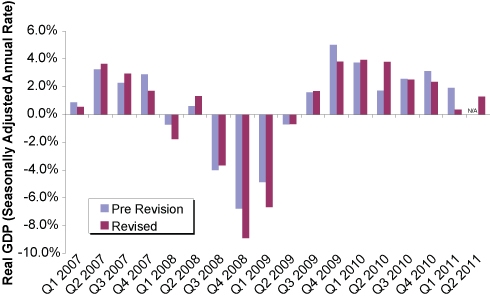

Beyond Q2’s first estimate and the revision to Q1, the BEA also re-examined data from the past three years. Several quarters were adjusted—in some cases sizably. Specifically, Q4 2008 and Q1 2009 were each lowered by over a full percentage point—a large skew from the average revision. Several other quarters were increased. The net effect of the BEA’s changes is they now report real US GDP is a hair below its pre-recession peak—by roughly 0.4%. Prior estimates had put it above.

Exhibit 2: Annual Historical Revision—Real US GDP at Seasonally Adjusted Annual Rates

Source: US Bureau of Economic Analysis.

But regarding these revisions, the real story isn’t so much what the numbers now say versus what they did, but rather, that government data have caveats one has to grasp well in order to use it well. As we’ve written many times, GDP is not a pure metric of economic health or vibrancy. For example, the rate is seasonally adjusted (often involving many major statistical quirks) and counts imports as a negative when, in fact, they don’t necessarily detract from economic activity and the totality of trade (exports plus imports) is perhaps a more important factor. GDP is a useful tool to help illustrate single-country output to an extent. But, perhaps above all else, GDP data are inherently backward looking, and revisions to three-year-old figures especially so. Since stocks are far more interested in what lies ahead, unearthing new data from what stocks consider the distant past isn’t going to provide much actionable information.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today