Personal Wealth Management / Market Analysis

Valuations—and Valuation Fears—Rebound

Are stocks really overvalued?

This bird isn't flying too high. Neither are stock valuations. Photo by Zoran Milich/Getty Images.

What a difference six weeks makes: In late August, after stocks lost over 10% in just 14 calendar days, some pundits hyped a silver lining-stocks were cheap. Fed head Janet Yellen and others had called stocks overvalued in May, and thanks to the correction, the problem was solved! But now, they're singing a different tune. Markets are recovering, and headlines once again call stocks overvalued, warning investors should expect blah returns. In our view, it's all noise. Stocks weren't pricey in May, and they aren't now. Valuations normally expand as bull markets mature, and stocks should still have plenty of room to run.

Exhibit 1 provides a pictorial description of this sentiment flip-flop.

Exhibit 1: S&P 500 Price-to-Earnings Ratio in 2015

Source: FactSet, as of 11/9/2015. S&P 500 12-Month Forward P/E Ratio, 12/31/2014 - 11/6/2015.[i]

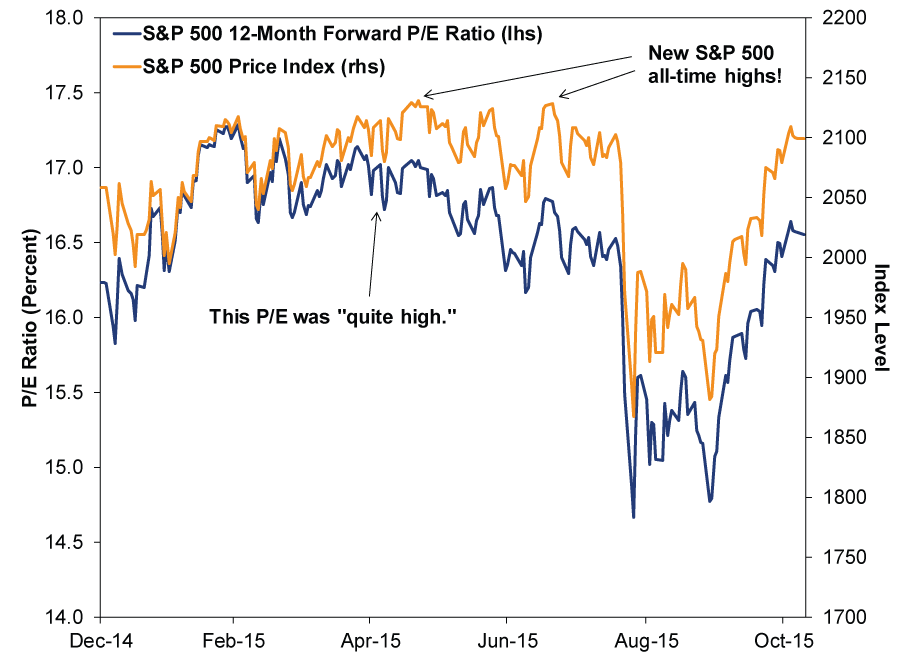

That first arrow points to May 6, the day Yellen called stock valuations "quite high." Oddly, P/E ratios then were lower than in late February and early March, even though stocks had risen. They also fell further from there, even as stocks hit new highs.

Exhibit 2: Really, Too High?

Source: FactSet, as of 11/9/2015. S&P 500 12-Month Forward P/E Ratio and S&P 500 Price Index, 12/31/2014 - 11/6/2015.

By now, you might be thinking, "sheesh, P/E ratios seem kind of feckless." We agree! They're open to interpretation, and they aren't predictive. As a ratio, they are driven by changes in the denominator (earnings) as well as the numerator (price), but most observers over-focus on the numerator, creating some weird perceptions. Someone looking at Exhibit 1, without pre-existing knowledge of stocks' returns, would easily think stocks fell from late February on. Yet they are up since then. The P/E ratio fell because projected earnings for the next year rose more than stocks did.

The knock on current valuations is that nothing has fundamentally changed since before the correction, making the rally inherently unsustainable-a quick, hope-driven snap-back. If stocks' fundamental backdrop were dreary, we'd get the pessimism. But fundamentals are actually quite positive, and we think investors should be delighted that nothing changed radically from May to late August to today. The global economy is still growing, with the US and UK in the driver's seat. Yield curves are positively sloped, and the US yield curve has steepened. China is still slowing, not landing hard. Commodity prices are still ultra-low, benefiting energy consumers and energy-importing nations. Non-commodity-reliant Emerging Markets are growing nicely. Low commodity prices also continue skewing Chinese imports down in value terms, making investors freak before they look at import volumes and realize demand there is firm. US earnings remain resilient to the stronger dollar, as the currency's impact on costs offsets the hit to revenues. Headline S&P 500 earnings growth of -2.2% y/y for Q3 drags down sentiment, fueling fear of a "profits recession," but excluding the long-beleaguered Energy sector, earnings are up 4.8% y/y with 444 firms reporting.[ii] Political gridlock keeps governments from mucking with property rights in the US, UK and much of Continental Europe. All these factors and more make a strong foundation for stocks.

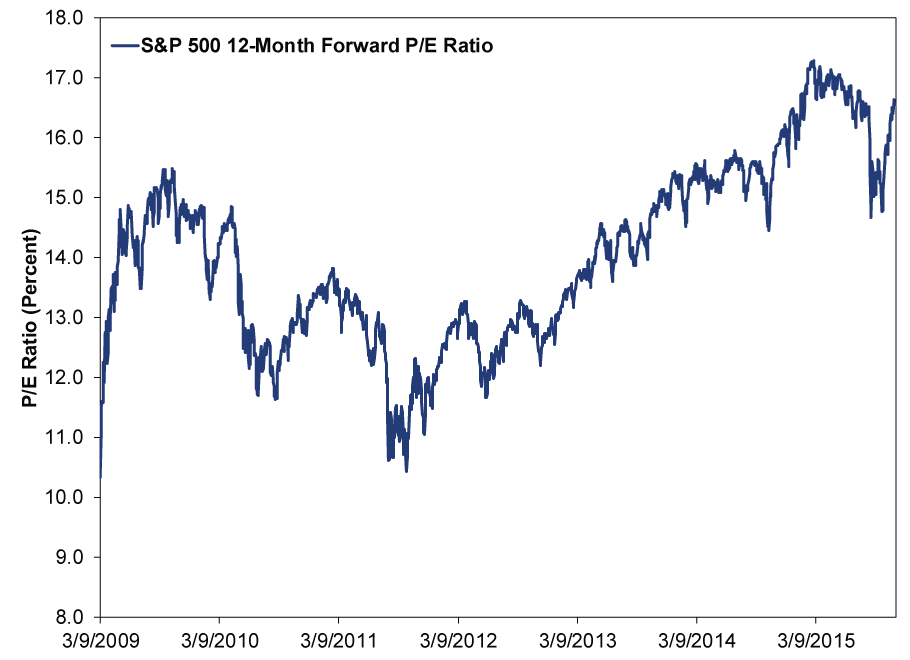

Valuations are useful solely as a sentiment gauge. August's drop showed that in spades-there was no rational reason investors should become dramatically less willing to bid up stocks in just two weeks. That was a sentiment-driven pull-back through and through. Valuations can also track sentiment's evolution over a full market cycle-starting high as stocks rebound before earnings, falling as earnings catch up, and then slowly rise as the bull mature and investors gain confidence. That's about where we are today, as Exhibit 3 shows.

Exhibit 3: S&P 500 Forward P/E Ratio During This Bull Market

Source: FactSet, as of 11/9/2015. S&P 500 12-Month Forward P/E Ratio, 3/9/2009 - 11/6/2015.

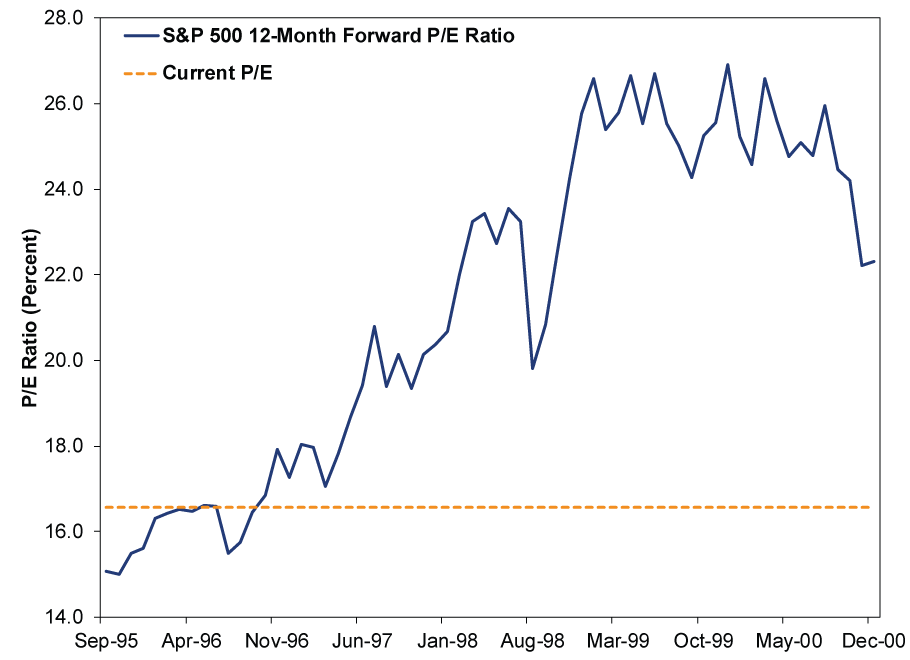

Today's P/Es are a bit above long-term averages, but averages are made up of extremes-extreme lows and extreme highs. Moreover, the average P/E doesn't represent some intrinsic or "fair" value for the market. Markets don't work like that. Stocks spent most of 1997, 1998 and 1999 with P/Es above today's level (Exhibit 4). The runaway craziness of the Tech bubble, when all those sloppy, profit-less IPOs fetched gigantic premiums, didn't hit until late 1999/early 2000. And the bubble didn't burst until after the Fed inverted the yield curve.

Exhibit 4: Stocks Were Far Pricier in the late 1990s

Source: FactSet, as of 11/9/2015. S&P 500 12-Month Forward P/E Ratio, 9/29/1995 - 12/31/2000 and on 11/6/2015.

That isn't to say P/Es will top 26 at this bull's peak. That isn't how markets work, either. But it does show today's valuations aren't inherently expensive, and there is no reason why they can't keep expanding as sentiment improves.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03 -

Market Analysis Digging Into Last Week’s Fed ‘Credibility’ Concerns2026-08-03

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today