Personal Wealth Management / Market Analysis

¡Viva España!

As we see in the case of Spain, improving economic data from the eurozone suggest the region won’t be as big a burden as feared on global markets.

ECB President Mario Draghi (left) may have reason to smile visiting Spanish Parliament President Jesus Posanda and Bank of Spain Governor Luis Maria Linde. Photo by Pablo Blazquez Dominguez/Getty Images.

The eurozone’s Q2 economic data are starting to trickle in, and while the region remains weak overall, we’re seeing more and more signs of nascent improvement—further proof the region’s recession won’t be a big drag on global growth, and evidence investors’ lingering eurozone jitters are overwrought.

Take Spain. In Q2, the country remained in recession—for the seventh straight quarter—but the pace of contraction slowed to just -0.1% q/q. Sure, that doesn’t mean Spain is out of the woods, but a peek under the hood shows several signs of a stabilizing economy.

For one, it’s the second straight quarter of headline improvement. And that improvement is rather broad-based. On a quarterly basis, consumer spending contraction slowed from -2.0% in Q4 2012 to -0.4% in Q1, and the slower contraction held in Q2 2013. Business investment contraction has also slowed quarterly—from -3.9% in Q4 to -1.0% in Q1 and -0.9% in Q2. Granted, short-term readings are variable and can be revised and updated. But the trend since Q4 2012 is noteworthy—particularly since it shows broad private-sector improvement.

Trade data are especially striking—as indicators both of international competitiveness and domestic demand. In Q2, combined Spanish exports and imports grew +1% q/q. As a matter of comparison, in Q1 2012, combined imports and exports contracted -1.9% q/q; in Q2 2012, they grew +0.5%. This suggests a strengthening of total trade in Spain, an economic positive.

Exports held up quite well earlier in the recession but dipped a bit in late 2012 and early 2013—not terribly surprising considering somewhat slowing global growth rates. But they rose +1.2% in Q2, suggesting Spanish exporters are starting to shrug off somewhat weaker external demand. This is largely because Spanish goods have become pretty competitive globally, thanks in part to many of the reforms enacted over the past year and a half.

Imports, by contrast, fell -5% for the year in 2012 as domestic demand cratered. But the contraction slowed quarterly to -1.7% in Q1, and again to -0.2% in Q2—more evidence of stabilizing domestic demand. Other indicators further support this. For example, Spain’s General Retail Trade Index, a gauge of retail sales tracked by the Instituto Nacional de Estadística, has also improved in 2013, rising steadily since February.

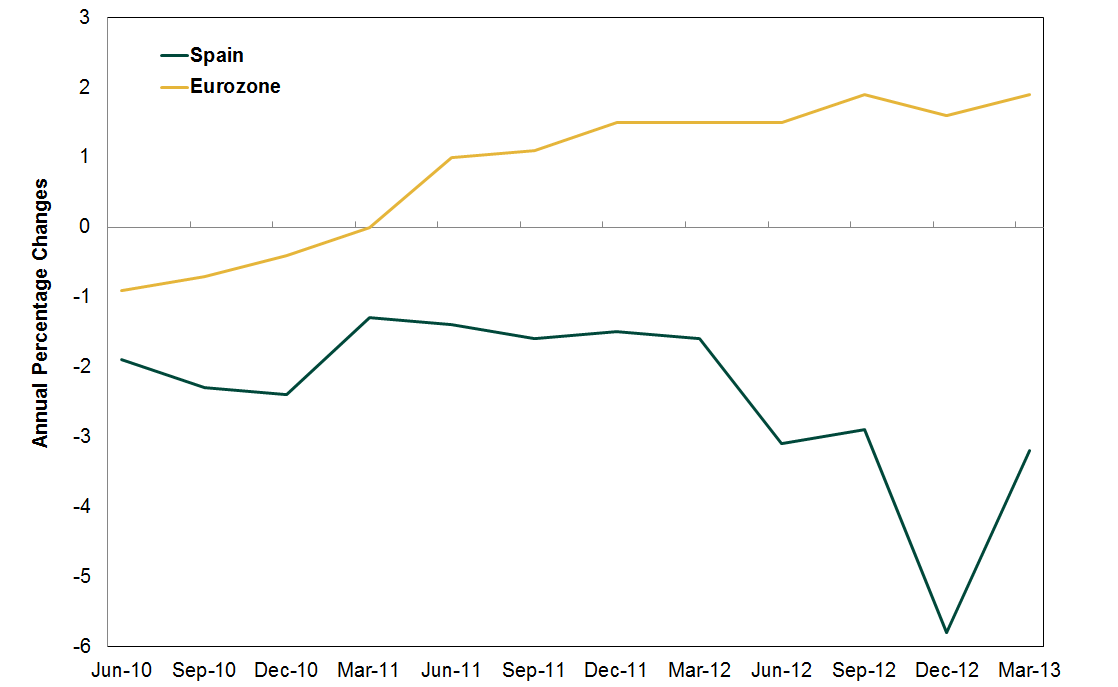

Looking ahead, Spanish firms seem well-positioned to capitalize on improving demand at home and abroad. Following the implementation of various labor reforms, Spanish businesses have spent the past couple years getting lean and mean. With more payroll flexibility, firms have been able to reduce unit labor costs, getting more bang for their buck. Spain has made tremendous strides on this front, especially relative to the rest of the eurozone. This trend continues today. (See Exhibit 1.)

Exhibit 1: Unit Labor Costs, Spain vs. Eurozone

Source: Bank of Spain, data accessed 7/24/2013.

But firms also cut overall investment/output quite a bit—partly because of the weaker economic climate, and partly because of the many tax hikes they’ve weathered. Capacity utilization fell from 72.6% in Q1 2012 to 69.4% in Q1 2013. But it appeared to perhaps turn the corner in Q1, rising to 73.1%. This suggests firms have largely squeezed all they can squeeze, and even a modest uptick in demand will force firms to fire up dormant facilities and production lines—auguring well for higher business investment looking forward.

As does the overall economic outlook. Though not a perfect indicator, the Leading Economic Index (LEI) for Spain increased 0.5% in May—the third rise in five months—and is up 1.8% over the past six months (compared with 1.4% over the previous six). Tellingly, capital equipment and new orders—the gauges most tied to the private sector’s outlook—contributed positively.

Again, none of this means all is rosy in Spain ahead. But it does strongly suggest fears of a Spanish implosion taking down the entire eurozone were overwrought. Especially as the banks continue working through their problems and sovereign yields remain manageable. Reality has vastly exceeded investors’ dour expectations, and as this continues—both in Spain and throughout the eurozone on balance—global stocks likely move further past eurozone fears.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Upcoming IPOs, US Jobs Data, Credit Card Delinquencies

2026-06-05

2026-06-05 -

Market Volatility Seek Perspective Instead2026-06-05

-

Market Analysis No Flowers for the May Jobs Report?2026-06-05

-

Expert Commentary The US Midterm Campaign Trends Ken Fisher Is Watching

2026-06-04

2026-06-04

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today