Personal Wealth Management / 2020 Election

We Have Presumptive Nominees

With Joe Biden seemingly locking down the Democratic nomination, markets get an earlier-than-expected dose of political clarity.

Editors’ Note: Our political coverage is intentionally non-partisan. We favor no party nor any candidate and assess politics solely for their potential impact on capital markets.

Today, we will take a break from covering the bear market and associated developments to highlight something more … normal: election-year politics. Yesterday, Senator Bernie Sanders suspended his presidential campaign, making former Vice President Joe Biden the presumptive Democratic nominee. This means we now have a two-man race for the White House, well before the party conventions. While markets are fixated on COVID-19 now, the presidential election should get more attention as it approaches. In our view, the early resolution to the Democratic primary should help election uncertainty fall. While we aren’t arguing this is hugely bullish in the near term, that reduced uncertainty is a positive factor we think is worth considering.

With over two dozen candidates vying for the Democratic nod, a contested convention was a possibility. All it would have taken was the same three or four candidates splitting the vote. But then Biden dominated Super Tuesday and continued racking up delegates over Sanders afterward. Now, with Sanders’ departure and President Donald Trump waiting in the wings, we know the presumptive nominees seven months before the general election. This gives stocks a bit of political clarity—earlier than most expected this year.

Political uncertainty is usually elevated early in an election season as lots (this time, literal dozens) of candidates compete for the party base’s attention. That often means promising sweeping policy changes, which stocks generally dislike. Markets must also grapple with a dizzying array of potential election outcomes, complicating analysis. As primaries thin the herd, this abates somewhat. Once presumptive nominees emerge, markets gradually get still more clarity. Uncertainty falls further as stocks digest each nominee’s flagship policies and likelihood of victory. Nominees’ focus also shifts from their base to middle-of-the-road voters, which tends to moderate their rhetoric.

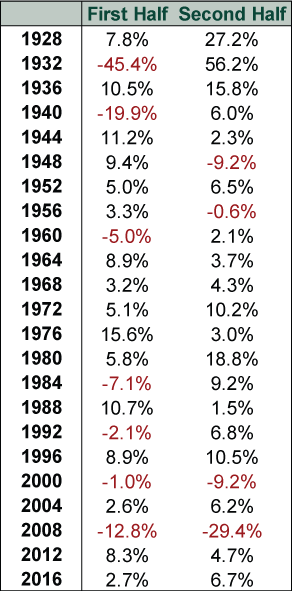

Meanwhile, House and Senate races take shape, giving markets a sense of whether the winner will have to work with a hostile, friendly or divided Congress—key to weighing legislative risk ahead. Thanks in part to this falling uncertainty, market returns typically improve in the second half of election years.

Exhibit 1: Returns in US Election Years

Source: FactSet, as of 4/8/2020. S&P 500 price returns, 1/3/1928 – 12/31/2016.

Now, this doesn’t preclude negative stretches, including bear markets. As Exhibit 1 shows, bears in 2000 and 2008 turned second-half returns negative. Politics are only one factor. But we think the trend is worth noting.

With the 2020 nominees known, markets can now turn their attention to the factors that can help them price in the eventual outcome. Polling, for example. As 2016 shows, national polls don’t necessarily indicate which candidate has an Electoral College advantage. But state polls—particularly in battleground states like Florida, Wisconsin and Michigan—may be more telling. Though, it is likely still too early to glean anything meaningful from them, as many did when a poll released Monday showed Biden six points ahead of Trump among registered Floridian voters, with eight percent undecided.[i] What will be more meaningful is how these polls evolve once the general election campaign gets going in earnest.

As November approaches, stocks will also monitor which candidate’s message seems to be resonating more with voters, particularly Independents—and whose party’s base seems more enthusiastic and therefore more likely to show up at polls. That enthusiasm feeds into Congressional races, too. Folks motivated to vote for a presidential candidate often sway down-ballot races as well, which frequently hinge on relative turnout. Big coattails didn’t seem likely to us before COVID-19 hit. It is too soon to say if this has changed. But if it does, markets likely anticipate it.

As in other election years with bear markets, non-political fundamentals may have a greater influence on returns. Right now, that looks like COVID-19—and whether commerce-restricting containment efforts lift sooner than expected. But it may be something else by November. Only time will tell. COVID-19 could also interfere with how markets typically price in election probabilities. For example, it likely keeps the election in the background for a while yet and may even delay campaign milestones like the conventions. If major gatherings remain off limits, it could also affect candidates’ momentum and reach. The virus itself is also a campaign wildcard. Will it still dominate the political discussion this autumn? Or will it have faded, allowing other issues to dominate the debate? Again, this is unknowable now, but worth watching.

That said, merely knowing the nominees brings stocks a dose of clarity they didn’t have just last week. Falling political uncertainty may seem trivial amid the coronavirus pandemic, but we think it can still provide a little-noticed tailwind for stocks in a brighter, post-COVID-19 future.

[i] “Slight advantage goes to Joe Biden over Donald Trump in Florida poll,” Anthony Man, South Florida Sun Sentinel, 4/8/2020. https://www.sun-sentinel.com/news/politics/fl-ne-biden-leads-trump-florida-poll-april-20200408-z74bj736uzhtffbvl4br5fkglu-story.html?outputType=amp

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today