Personal Wealth Management / Economics

What Pundits’ PMI Pessimism Says About Stocks

It suggests to us the bull market is on fine footing.

“The September PMI data will add to worries that the UK economy is heading towards a bout of ‘stagflation.’”[i] Across the English Channel, pundits bemoaned that “the Delta variant of coronavirus hit demand and supply-chain constraints pushed input costs to a more than two-decade high.”[ii] Japan’s results allegedly “underscor[ed] the protracted impact of the coronavirus pandemic,” while America’s showed “persistent supply-chain problems hit activity.”[iii] Reading those takes on September’s flash purchasing managers’ indexes (PMIs), you might think these business surveys point to contraction in many parts of the developed world. But if so, you would be wrong. Why the dour reaction, and what should investors make of it? Here we put pundits’ latest PMI pronouncements into perspective.

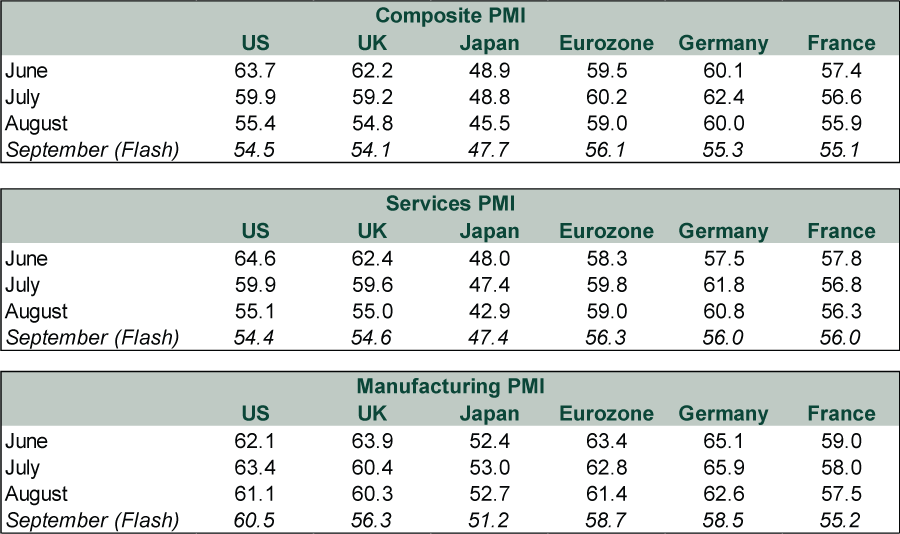

September’s flash PMIs did broadly tick down from August. But all remain well above 50, signaling expansion—except Japan, which hasn’t posted an expansionary reading since April (and, before that, January 2020). So for the US, UK, eurozone, Germany and France, September’s downticks don’t imply contraction—they just suggest growth wasn’t quite as broad-based as last month’s. (Exhibit 1)

Exhibit 1: Major Economy PMIs

Source: FactSet and IHS Markit, as of 9/23/2021. Flash PMIs are preliminary estimates based on 85% – 90% of responses.

Services activity—the lion’s share of developed world GDP—saw the biggest drops in the eurozone, leading composite levels’ declines. But this simply follows the US’s path a month prior. America reopened first from lockdowns among western nations, enjoyed the post-lockdown surge in economic activity first, and also saw that initial burst fade first. That pop, which stemmed from unleashing pent-up demand in late spring and early summer, always appeared unlikely to last. Once people got the initial rush back to shops and restaurants out of their system, they would logically return to a slower pace of life. We think this is the chief force behind the recent PMI downticks. Declines from very high levels earlier shouldn’t shock.

Manufacturing seemingly held up a bit better, due partly to lengthening supplier delivery times. Those are normally viewed positively as a demand indicator, as it means producers can’t keep up with incoming orders. That is the case now, but there are also severe shortages hampering production, which is a headache. Even stripping that skew out, though, results were still good. Manufacturing output subindex levels were in the low 50s (save Japan’s at 48.1).[iv] In other words, despite supply constraints clearly weighing on factories, output is still expanding, which suggests the problem remains surmountable.

Demand is strong, too, although that is less of a positive signal than it would otherwise be. Ordinarily we would look now to new orders as the forward-looking component of PMIs, but for the moment, we don’t think they have much predictive power, if any. In theory, today’s new orders are tomorrow’s production, but supply shortages throw a big monkey wrench in that.

For investors, we think pundits’ negative response to fine PMI readings is a sign of sentiment, not fundamentals. PMIs are some of the most widely watched reports out there. Nowadays, so are supply-chain issues, like the much publicized port backups and semiconductor shortages we read about every day as COVID outbreaks and lockdowns plague key global hubs. Ditto for China’s electricity shortage and rationing. Global markets discount such widely available information—and well-known problems—in real time. In our view, stocks’ direction depends on how reality develops against those expectations, not the generally backward-looking news flow itself.

Prevailing pessimism sets a low bar to clear. When the economy’s actual path isn’t as bad as feared, stocks typically benefit. Weaker growth needn’t be an impediment. In our view, over the 3 to 30 month timeframe markets generally weigh, bottlenecks will likely prove passing—ergo economic weakness and price pressures stemming from them, too. We don’t think they materially shift the global economy’s longer-term outlook. Besides, slower growth was always likely post-reopening, a baseline we think stocks have long since incorporated. Supply disruptions this year have added another wrinkle. But they probably aren’t the cause of an economic downturn markets didn’t anticipate.

[i] “Output Growth Slows Further, While Selling Price Inflation Hits Record High,” Staff, IHS Markit, as of 9/23/2021.

[ii] “Euro Zone Business Activity Slowed in Sept, Input Costs Hit Over Two-Decade High,” Staff, Reuters, 9/23/2021.

[iii] “Japan’s Sept Manufacturing Activity Growth Slows - Flash PMI,” Staff, Reuters, 9/23/2021. “US Economic Activity Slows in September Amid Delta, Supply Shortages - IHS Markit,” Xavier Fontdegloria, Morningstar, 9/23/2021.

[iv] “Downturn in Private Sector Activity Continues in September,” Staff, IHS Markit, as of 9/24/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today