Personal Wealth Management / Economics

What to Make of China’s Q2 GDP Rebound

China’s Q2 GDP surprised pundits—and their reaction is telling, in our view.

In a bit of good global economic news, China’s Q2 GDP rose 3.2% y/y after Q1’s historic -6.8% contraction, topping expectations for 2.5% growth.[i] Though the report beat expectations, the broad reaction was largely skeptical—indicative of the dour sentiment prevalent today.

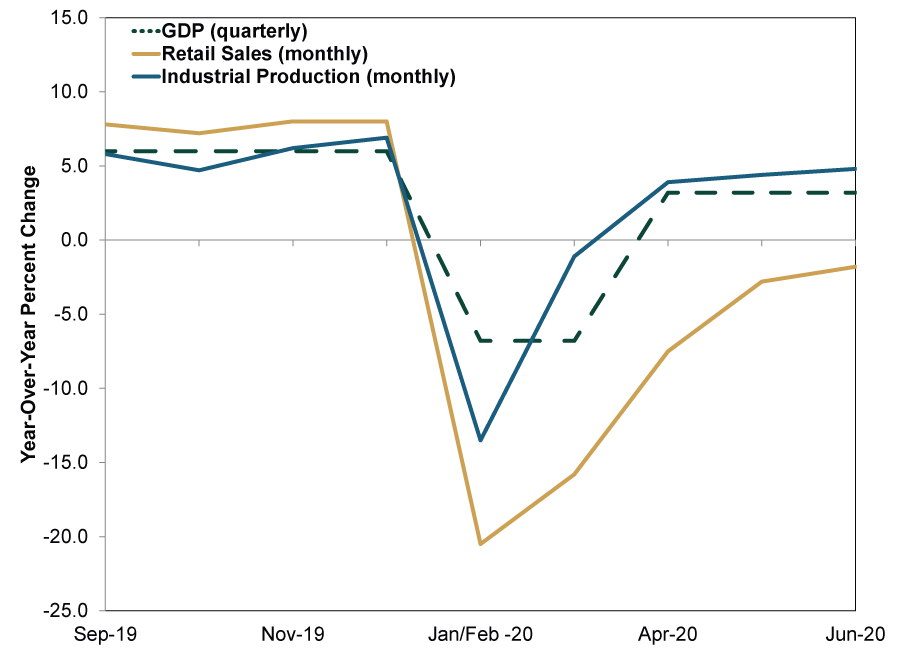

Of course, the rebound doesn’t reverse the drop in total. For the first half of 2020, Chinese GDP is down -1.6% y/y from 2019’s first half.[ii] Looking under the hood reveals industrial production has recovered more quickly than personal consumption—a trend supported by recent monthly data. For example, in June, industrial production rose 4.8% y/y, accelerating from May’s 4.4%, while retail sales’ decline slowed by a percentage point but remained in negative territory (-1.8% y/y in June versus May’s -2.8%).[iii]

Exhibit 1: China’s GDP, Retail Sales and Industrial Production

Source: National Bureau of Statistics of China and FactSet, as of 7/16/2020. January and February data are combined to account for skew due to the Lunar New Year holiday.

Though GDP gets the spotlight, Q2’s positive report is consistent with other recent datasets. China’s purchasing managers’ indexes (PMIs, monthly surveys that track economic activity) for the manufacturing and non-manufacturing sectors have exceeded 50 since May—indicating more businesses expanded than contracted.[iv] June exports and imports rose modestly, positive signs for foreign and domestic demand. The upshot: Chinese economic activity has been stirring after the country started easing its draconian lockdowns in March.

While China’s rebound impressed a handful of experts—some forecast China as the only major economy to grow in 2020—most had plenty of yah-buts. Some noted China is relying on a familiar playbook of government stimulus to boost factory output and spur growth. This reliance on heavy industry has prompted some warnings of a rapidly inflating property bubble setting up future issues. Personal consumption has been tepid, too, and some worry nervous consumers will be unwilling to spend for a while—limiting any recovery. Beyond domestic developments, pundits argue the global economy remains weak, which will weigh on export-heavy Chinese growth. Ominous external clouds allegedly also loom, from trade tensions with the US to a potential new COVID outbreak that forces another national lockdown.

We don’t dismiss all these concerns, and some raise sensible considerations. We agree the global economy’s prospects rely on other major economies’ reopening progress, which has been gradual and inconsistent. That has weighed on Chinese exporters. Government stimulus, too, isn’t a magical pill for economic growth. That spending simply chooses winners and losers and isn’t always the most efficient use of capital.

Yet reality may be better than headlines seem to appreciate. While many question the accuracy of China’s official data—a fair critique—private global businesses confirm the country’s economy has been improving. For example, US industrial lubricant producer WD-40 reported total sales were down -14% y/y in its fiscal quarter ending May 31, 2020—yet China sales were up 26% in the same period.[v] Bulten AB, a Swedish manufacturer, reported China factory production is back to pre-pandemic levels, and Starbucks has said 90% of its Chinese cafes are back to pre-pandemic hours.[vi]

In our view, Chinese data are a loose preview of what awaits other major economies, in the sense that reopening timing and progress are key to growth trends. However, we also suggest investors take care when comparing China’s GDP growth rates to major developed economies’. Though China has reported seasonally adjusted quarterly GDP since 2011, many experts are skeptical about the methodology used—preferring the year-over-year growth rate instead. Year-over-year calculations tend to be less volatile but are also more backward-looking than the quarter-over-quarter or annualized rates commonly used in the developed world.[vii] China’s Q2 2020 growth is calculated using Q2 2019 as the denominator. Hence, matters from way before COVID hit could affect growth rates and trends. Further, data for months and quarters after the lockdowns ended could still see the negative influence of Q1 2020’s contraction, as it remains part of the year-over-year math. This has the superficial effect of making China’s contraction and rebound appear less dramatic when compared to the US, which reports an annualized quarterly growth rate, or the UK, which primarily reports at quarter-over-quarter rates. No calculation is inherently superior, but understanding the differences can help clear up nuances headlines tend to gloss over.

Regardless of the calculation method, GDP won’t tell you where the economy is headed, let alone what forward-looking stocks will do next. However, the many doubts surrounding China’s positive Q2 are more evidence of the “Pessimism of Disbelief,” in which skepticism colors any and all positive news—like evidence of a recovery in the world’s second-largest economy. This phenomenon is common at the beginning of bull markets—partly why we think a new bull has begun.

[i] Source: FactSet, as of 7/16/2020.

[ii] National Bureau of Statistics of China, as of 7/16/2020.

[iii] See note i.

[iv] Ibid.

[v] “China’s Economy Appears Back on Track, but Challenges Remain,” Jonathan Cheng, The Wall Street Journal, July 16, 2020.

[vi] Ibid. and “Starbucks says it lost $3 billion in revenue in latest quarter due to coronavirus pandemic,” Amelia Lucas, CNBC, June 10, 2020.

[vii] An annualized GDP growth rate usually compounds a quarterly rate and presents the result as if growth persisted at that clip for an entire year.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 22 - June 262026-06-29

-

Market Analysis Global Vs. Local: UK Bond Yield Edition2026-06-29

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-06-29

2026-06-29 -

Expert Commentary This Week in Review | Oil Prices, UK Politics, Tech Stocks

2026-06-26

2026-06-26

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today