Personal Wealth Management / Market Analysis

When Not to Trade

Election-night volatility led to wildly incorrect market forecasts, showing the folly of trading around major news events.

Editor's Note: Our political commentary is nonpartisan and non-ideological by design as political bias is a dangerous investing error. We favor no political party or candidate and assess politics solely for potential market impact.

On Tuesday night, most TV networks flipped between two visuals: the electoral map, and plunging S&P 500 futures markets. For extra flavor, some threw in the freefalling Mexican peso, sharp dives in foreign stock markets and rising gold prices (allegedly a safe haven during times of crisis).[i] The media seized on these snapshot trends and the obvious conclusion: Investors were fleeing to safety, and those who didn't join them would suffer steep losses Wednesday and beyond. Yet within a few hours of markets' opening, that theory was bunk. Most of those moves reversed, and stocks finished the day up. Volatility could very well resurge, but for now, consider this crucial lesson: Don't trade around major news events expecting markets to respond a certain way to the outcome.

The following charts detail some of foreign markets' (and gold's) hourly moves on November 8 - 9. They show Tuesday evening's fears of a sustained decline were overwrought-after just a few hours, the trends garnering so much attention had disappeared. S&P 500 futures pared many of their losses before the opening bell on November 9. The index itself did open lower, but by day's end, it was up. Foreign markets lost ground as the votes were counted, but they, too, bounced back swiftly.

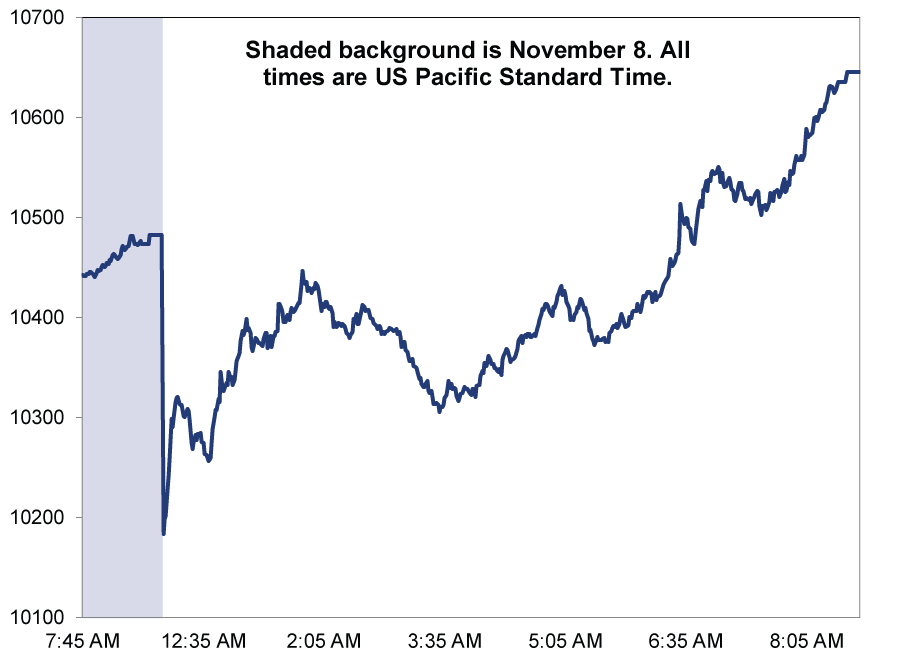

Exhibit 1: German DAX

Source: Factset, as of 11/10/2016. Deutsche Boerse AG German Stock Index (DAX), selected hours from November 8 - 9, 2016.

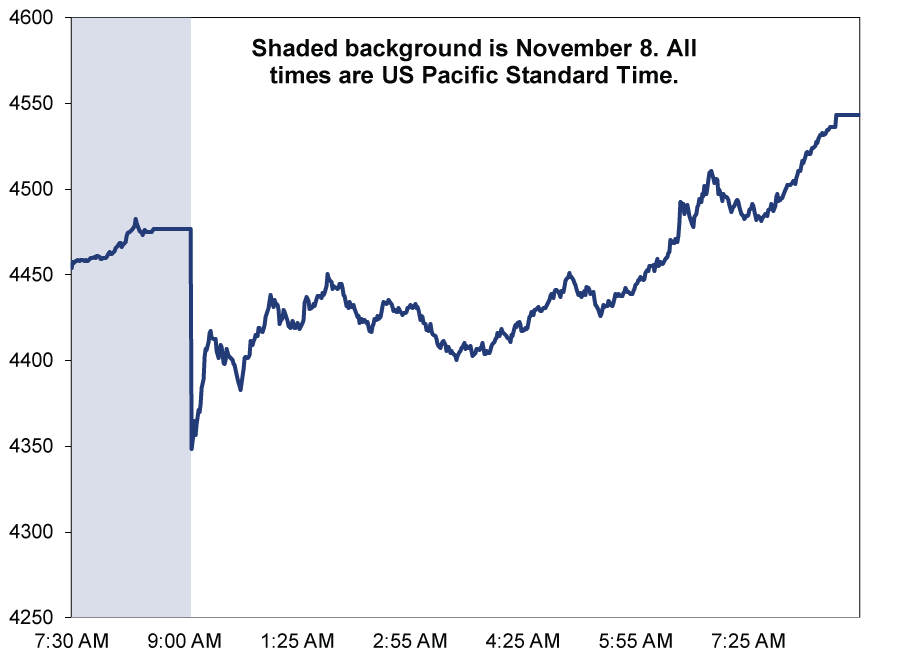

Exhibit 2: Japanese TOPIX

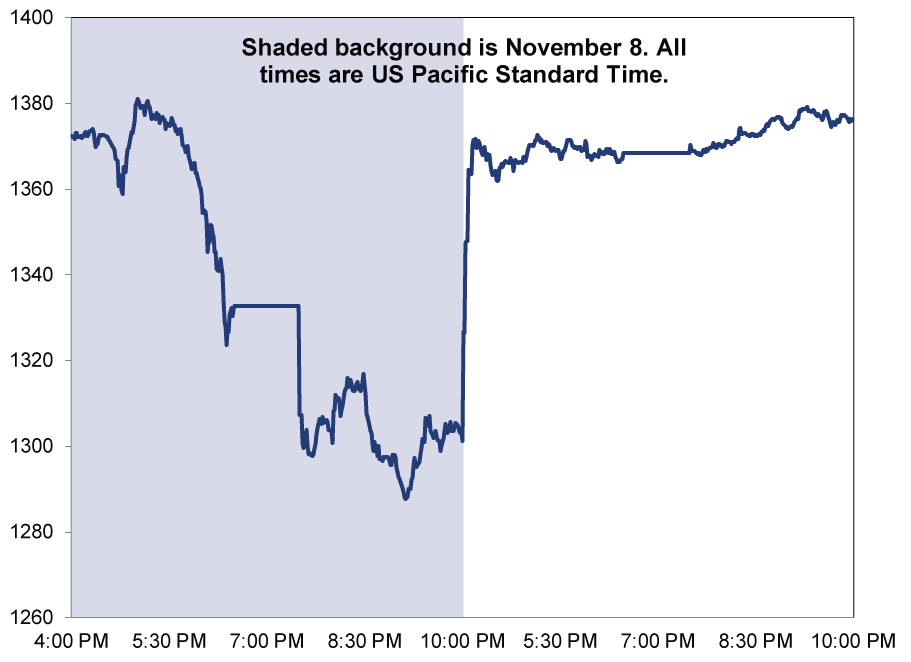

Source: Factset, as of 11/10/2016. Tokyo Stock Price Index (TOPIX), selected hours from November 8 - 9, 2016. Exhibit 3: French CAC 40

Source: Factset, as of 11/10/2016. Continuous Assisted Quotation 40 (CAC), selected hours from November 8 - 9, 2016.

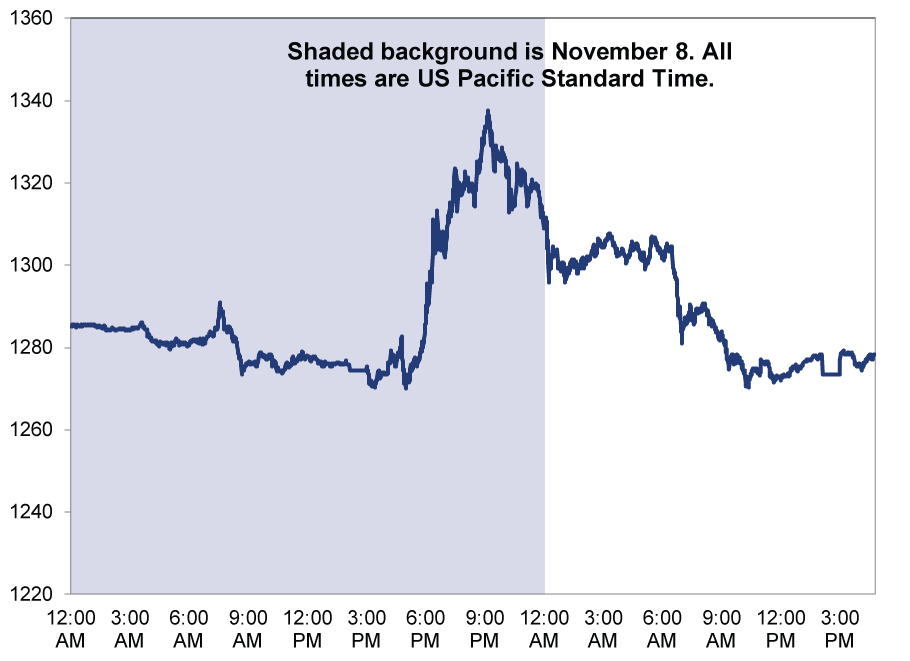

Exhibit 4: Gold

Source: Factset, as of 11/10/2016. New York gold spot price, continuous. Selected hours from November 8 - 9, 2016.

Overall, it seems pretty clear investors who followed polls and conventional wisdom registered their instant panic in futures markets. Markets priced that fear quickly, as they always do, then moved on as cooler heads smelled buying opportunities. This reminds us a whole lot of Brexit, when futures selloffs and initial UK stock losses sparked great fear. The first two trading days after the vote, the MSCI UK fell -5.6%. But then it bounced. By June 29, it closed above pre-vote levels. Through Thursday's close, it's up 9.3% since the vote.[ii]

Trading around much-anticipated events such as elections is dangerous. As Wednesday's moves demonstrate, markets move fast-faster than heads can cool and second thoughts arise. One moment it may appear you've sidestepped new lows that are sure to come, and the next you're staring at a surprise rebound you didn't participate in. In investment lingo, you've been whipsawed. Sadly, this scenario is all too common-when you're up late at night, and the unexpected happens and markets seem like they're going a bit nuts, it's natural for emotions to take over and drive investment decisions. Humans' fight-or-flight mentality is innate. Huge, highly covered events often arouse it. But resisting the temptation to react is vital. Brexit taught this lesson in June, and now investors have another opportunity to learn it.

Too often, pundits extrapolate sharp market movements around a major event-even if they last just few hours or days-far into the future. Investors tuning in get confident-sounding forecasts based on a teensy slice of backward-looking stock price data, biases and assumptions. None truly predict markets' future.

Our advice at such times: Stay cool, and think of the entire time horizon your assets need to work for you. Markets' initial reaction to one event, however fearful, has next to no bearing on long-term returns. We aren't saying politics have no impact, but markets move on probabilities, not possibilities. They care about what presidents do, not what they say. On Tuesday night, investors got no insight on what President Trump will actually do in office. That will take time to discover, as he shapes his cabinet and solidifies a legislative wish list. Only then can investors rationally assess probabilities and weigh them against prevailing expectations.

On that point, consider: Where are expectations currently, and what is the likelihood reality exceeds them over the next 12 - 18 months? This, after all, is how markets think. Expectations started pretty low, as initial volatility suggests, and markets have priced in that fear. Maybe it resurges over the coming days or weeks, and wobbles return. But over time, the reality of a gridlocked Beltway should reassert itself. Trump campaigned with minimal support from Republican Party stalwarts, many of whom directly opposed his candidacy. Neither side can mend those fences overnight, particularly given Trump's ideological pedigree doesn't align well with some Congressional Republicans, and the party holds only a slim majority. Intraparty gridlock is still gridlock, likely constraining Trump's campaign promises and lowering the chances for the type of huge, sweeping legislation markets dislike. As long as sentiment-which has warmed the last couple days-doesn't overshoot and economic fundamentals remain healthy, a benign legislative agenda should give this bull market ample reason to grind higher.

[i]It isn't that, by the way.

[ii] Source: FactSet, as of 11/11/2016. MSCI UK Index total returns, 6/23/2016 - 6/27/2016 and 6/23/2016 - 11/10/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today