Personal Wealth Management / Market Analysis

Will a Higher Deficit Lead to Doom?

Unlikely.

Earlier this month, in the wee hours of a Friday morning, President Trump signed into law a bill funding government through September 2019, to the collective relief of many who (oddly, to us) fear government shutdowns. But the bill brought its own worries! Along with funding government, the bill suspended the debt ceiling and boosted spending on defense and non-defense areas. Add this spending to the recent tax cut, and many pros are bemoaning big potential deficits ahead. Some say the Federal deficit will hit $1 trillion by 2019 and comprise 5% of GDP, triggering a cornucopia of related fears. Is this spending package appropriate for an economy close to full employment? Isn’t adding to the national debt unsustainable? Could it inflame inflation and cause the economy to overheat? Will a high deficit late in the economic cycle hinder the government’s ability to combat the next recession? In our view, these worries are misguided—a higher deficit shouldn’t imperil the US economy or derail stocks.

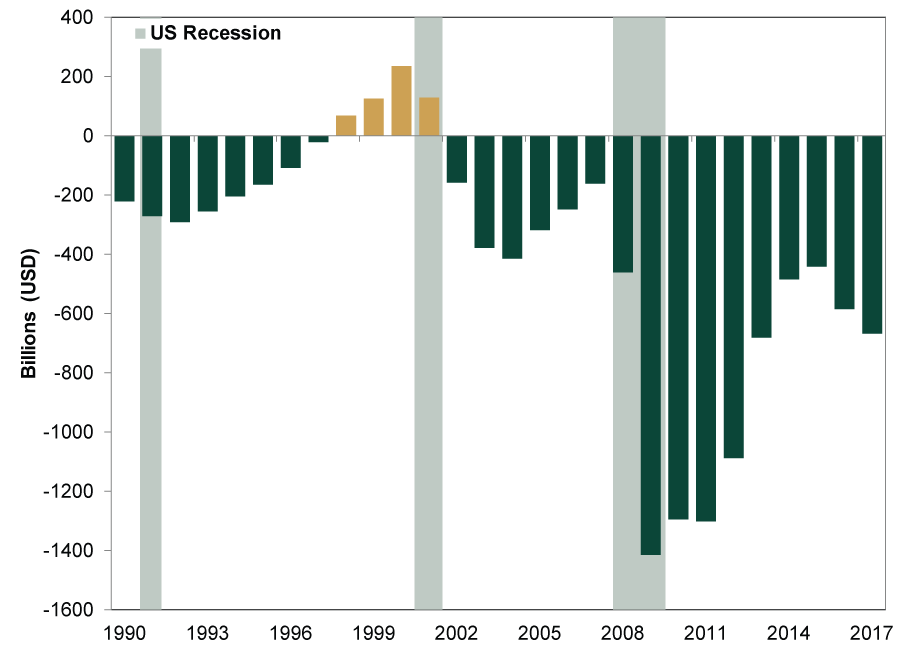

First, history shows high deficits don’t cause recessions or bear markets. Exhibit 1 shows federal surpluses and deficits since fiscal year 1990 with recessions highlighted.

Exhibit 1: US Federal Surpluses and Deficits Since Fiscal Year 1990

Source: St. Louis Federal Reserve Bank, as of 2/13/2018. US fiscal year ends on September 30 each calendar year. Recession dating from NBER.

Rising deficits typically trail, rather than lead, recessions. Intuitively, this makes sense: The government usually starts stimulus programs that add to a deficit after economic troubles manifest themselves. And if rising deficits trail recessions, they also trail bear markets. Stocks are the ultimate leading indicator, and typically, stocks start pricing in weaker economic conditions far before the official data catch on.

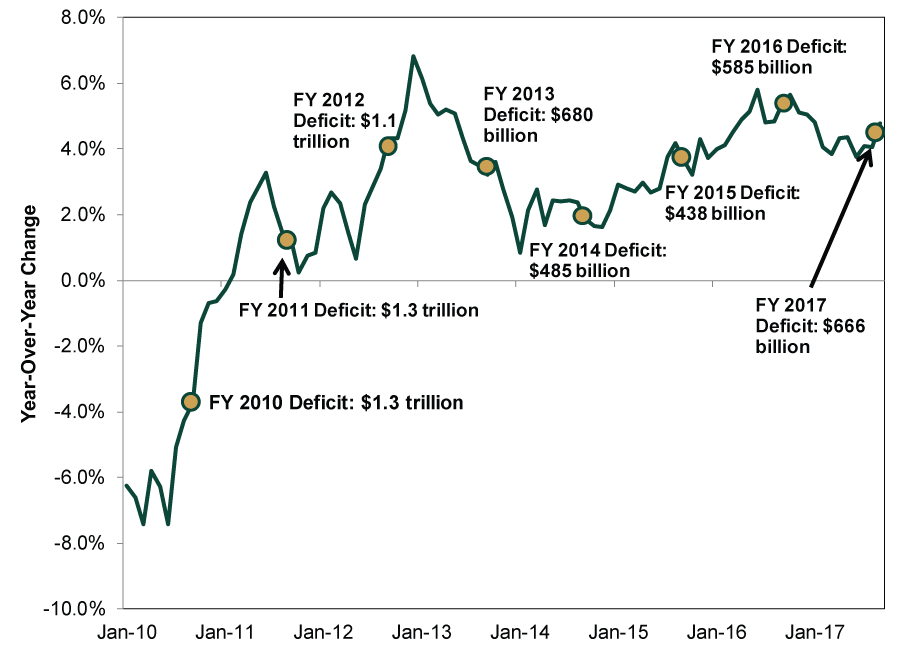

Higher deficits don’t automatically mean higher inflation—and increased risk of overheating the economy—either. Inflation hasn’t exceeded a 3.0% year-over-year rate since January 2012, when the deficit was also around $1 trillion. If a higher deficit back then didn’t cause high inflation that enflamed the economy, we don’t see why it would be so different today. Remember, inflation is always and everywhere a monetary phenomenon: a case of more money chasing a limited number of goods and services. Rising money supply typically leads to higher inflation. But contrary to conventional wisdom, the government isn’t the primary driver behind money supply growth. Yes, US Treasury bonds are a component of M4 money supply, but in our fractional reserve banking system, banks provide most of the money. If trillion dollar deficits allegedly mean more money sloshing around in the economy, why has money supply growth picked up as the deficit has gotten relatively smaller?

Exhibit 2: Deficits Don’t Drive Money Supply

Source: Center for Financial Stability and St. Louis Federal Reserve Bank, as of 2/15/2018. M4 year-over-year percent change, January 2010 – January 2018.

As for whether or not the government will be short-handed in fighting the next recession, this is pure conjecture and speculation. Contrary to ominous headlines, we don’t know when the next recession will start. That means we don’t know what tools Congress will and won’t have at its disposal. What we do know: Even with the recent uptick, borrowing costs for US sovereign debt remain near generational lows. Though the absolute level of debt sounds high, the government has a lot of wiggle room. Plus, the absolute level of debt isn’t as important as a country’s ability to service it—that is, make its interest payments. For fiscal year 2017, the US paid $263 billion in debt interest—or 7.9% of the government’s $3.3 trillion in tax revenue. We aren’t arguing the US should just pile on debt endlessly. But true debt problems would require years of sky-high interest rates and runaway spending[i]—exceedingly unlikely to materialize within the next 30 months, which is about as far ahead as stocks look. That means Uncle Sam should have capacity to borrow to fund stimulus if a recession strikes within the next few years.

Plus, on a practical level, we think the importance of fiscal stimulus during a recession is overstated. While we agree fiscal stimulus can help when liquidity is tight and demand needs prodding, the business cycle—not government spending—determines when a recovery happens. Fiscal stimulus merely jumpstarts recoveries that would have eventually happened anyway—helpful, but not essential. The eurozone emerged from its 2011-2013 regional recession without any sort of broad stimulus plan. Places like Spain went the other direction and endured some tough austerity reforms. They are now enjoying some of the fastest economic growth in the eurozone’s 19-quarter-long GDP growth streak.

This bull market has plenty of positive drivers that suggest stocks still have fuel to rise higher. In our view, fretting the projected higher federal deficit is rehashing several old false fears that have yet to cause a recession or meaningfully spook stocks. These false fears’ persistence signals broad euphoric sentiment still remains a way off.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today