Personal Wealth Management / Economics

Will a Jobless Recovery Hinder Stocks?

Jobless recoveries are the norm, not the exception.

As the latest business surveys showed improving economic output across the developed world, headlines trumpeted a new concern: a potential “jobless recovery.” Though businesses reported increased activity overall, they were also still cutting headcount, and recent US initial jobless claims reports showed layoffs are rising for the first time since March. Many worry budding economic green shoots will wither if millions remain out of work. But this development isn’t unique: Most recoveries are “jobless” early on. While the magnitude may be large, nothing in the latest reports is a unique or different risk to stocks than in most historical bull markets.

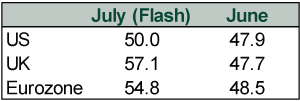

IHS Markit’s July flash purchasing managers’ indexes (PMIs) showed ongoing economic improvement in the US, UK and eurozone. All composite readings (services plus manufacturing) were at or above 50, indicating a broad return to expansion for the first time since COVID went global.

Exhibit 1: IHS Markit Composite PMI

Source: IHS Markit, as of 7/28/2020.

While PMIs are timely, they reveal only the breadth of growth—not the magnitude. July readings add more evidence of the economic benefits from countries’ easing COVID restrictions, but skepticism about a recovery remains—particularly since PMIs and other data show continued labor market weakness. IHS Markit economists warned ongoing headcount reductions in both the UK and eurozone may hurt future consumer demand. While the US PMI noted job-shedding eased in July, some worry this is fleeting—especially after the past two weekly jobless claims reports showed minor upticks (due largely to seasonal adjustments). Many seem convinced a meaningful economic recovery can’t take hold until jobs return.

This all fuels a popular question: How could global stocks basically be flattish for the year—and up 45% since their March 23 low—when major economies are in recession and hemorrhaging jobs?[i] In our view, the answer is simple. Stocks are looking much further into the future—normal in early bull markets—while most other economic data are backward-looking. For example, jobs data are late-lagging indicators, representing past business decisions. They result from economic growth, rather than causing it. Similarly, measures like PMIs provide a snapshot of how the economy is faring. While the insight will vary—PMIs are more timely but lack the detail of a comprehensive GDP report—these metrics also indicate what the economy just did.

In contrast, stocks are leading economic indicators and focused primarily on the next 3 – 30 months. They factor in all widely known information and value companies’ future earning power. During the throes of a bear market, stocks focus on the immediate conditions lying ahead—the short end of that 3 – 30 month range. Once they get a sense of how big the economic contraction will be and how long it will last, stocks start looking towards the longer end of that 3 – 30 month period and weigh far future earnings. This is what we believe stocks did this year: They reckoned first with the COVID-driven fallout and upcoming recession. After digesting this information, stocks moved on—looking ahead to future profits even before the economic downturn officially ends.

Moreover, recent US history—which we focus on here for consistency with stock market data, recession dating and unemployment numbers—shows “jobless recovery” fears aren’t novel.[ii] In November 2009, a headline cried, “Stop the ‘Jobless Recovery’ Madness!” and its accompanying article warned, “An economy that isn’t creating employment opportunities simply isn’t doing its job.”[iii] Though the unemployment rate peaked at 10.0% in October 2009 and didn’t return to the prior expansion’s low for eight years, stocks and the economy improved well before that.[iv] An S&P 500 bull market began in March 2009 while an economic expansion started that July.[v] In January 2003, a New York Times headline asked, “Is There Such a Thing as a Jobless Recovery?” and one interviewed economist worried weakening consumer spending would derail the economy.[vi] While the unemployment rate peaked at 6.3% in June 2003, the recession had ended in November 2001 and a S&P 500 bull market had begun in October 2002.[vii] Almost thirty years ago, when economist Nicholas Perna popularized the term “jobless recovery” in October 1991, a recession had ended seven months earlier in March while the S&P 500 was already a year into a bull market.[viii] Yet the unemployment rate didn’t peak until June 1992.[ix]

We don’t dismiss the human reality behind high unemployment figures, but for investors, it is critical to sort through the data that do and don’t matter to stocks. In our view, the widespread expectations that a recovery won’t take hold until jobs return are a brick at the base of the wall of worry—common to see in new bull markets.

[i] Source: FactSet, as of 7/28/2020. MSCI World Index returns with net dividends, 12/31/2019 – 7/27/2020 and 3/23/2020 – 7/27/2020.

[ii] Source: Global Financial Data as of 10/23/2019 and NBER as of 7/28/2020. Statements on S&P 500 bull market dating based on S&P 500 Index Price Level from 5/29/1946 – 12/31/2013.

[iii] “Stop the 'Jobless Recovery' Madness!” Colin Barr, CNN, November 6, 2009.

[iv] Source: Federal Reserve Bank of St. Louis, as of 7/28/2020. Unemployment rate, October 2009, May 2007 and March 2017.

[v] See note ii.

[vi] “The Nation; Is There Such a Thing as a Jobless Recovery?” Alex Berenson, The New York Times, January 26, 2003.

[vii] See note ii and iv.

[viii] “Consumer Sales Post Rise of 0.7%” Sylvia Nasar, The New York Times, October 12, 1991. See also note ii.

[ix] See note iv.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today