Personal Wealth Management / Market Analysis

Will Inflation Pound UK Growth?

Looking past the headlines, the UK economy appears healthier than many think.

Among the economics community, this was-and remains-a common assumption: Britain's vote to leave the EU will have economic consequences. In particular, many pundits point to the pound's post-vote fall and argue inflation's coming, with dire effects on consumption. While consumption remained firm the first few months following the vote, early 2017 retail sales data were soft as inflation jumped-spurring claims Brexit bears' calls weren't wrong, just early. But now data are emerging suggesting this slowdown was temporary and broader fears overblown. To us, this saga illustrates how detached sentiment-largely tied to Brexit-is from reality.

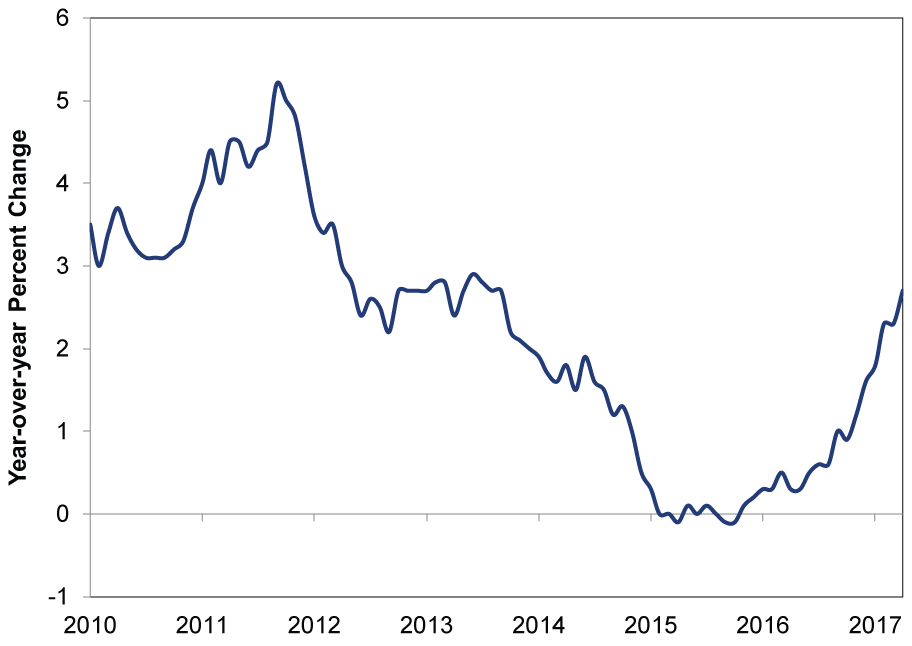

Since the pound plunged in the Brexit vote's wake, folks have feared it would bring high inflation and sink consumer spending-and, by extension, the UK's consumer-driven economy. All last year, the country looked resilient. Even as inflation inched up, household spending and the broader economy stayed strong. But earlier this year, folks worried the tide was turning. Before April, retail sales fell in four of five months, and GDP growth slowed to 0.3% in Q1 as services output-the biggest recipient of consumer spending-also slowed to just 0.3%.[i] Meanwhile, inflation kept marching higher, hitting a three-year high of 2.7% y/y in April. (Exhibit 1) Retail sales volumes rose 2.3% m/m that month,[ii] but most observers couched it as a one-off with more weakness to come as inflation keeps rising and biting.

Exhibit 1: UK Consumer Prices Index

Source: Office for National Statistics, as of 5/19/2017. Consumer Prices Index year-over-year percent change, January 2010 - April 2017.

While this sounds compelling, we see several reasons to question it. A weaker pound does raise the cost of some imported goods, but it isn't a uniform, across-the board effect as some companies hedge and others trade in foreign currencies. Plus, consumer prices are mostly a function of supply and demand in the end market. Companies can't always pass on higher input costs. Then too, imported goods don't account for the bulk of consumer spending. Domestic services receive the lion's share, and they are largely unaffected by currency movements. To the extent the pound has impacted some prices, this doesn't necessarily mean they keep rising. The pound's fall was (so far) a one-time event, with a -16% slide from Referendum Day to October 17.[iii] More than 10 percentage points of that drop occurred by July 5, and since reaching that mid-October low, it has risen a bit to sit about 10% below pre-Brexit. In a matter of months, the reference points for year-over-year calculations should be more favorable.

Other forces driving inflation in recent months should fade soon, too. Energy math, as big a driver in Britain as America, should become much tamer as the year wears on and today's relatively higher prices look back to higher year-over-year benchmarks. Transport costs-the primary driver of April's jump-should revert from their usual Easter surge, which looked even bigger this time since Easter came in April. Last year, it was in March, distorting the year-over-year calculation.

All that said, to paraphrase Milton Friedman, inflation is always and everywhere a monetary phenomenon, and money supply is growing gangbusters-a factoid oddly omitted from every piece of inflation coverage we've seen in recent months. March UK M4 ex[iv]money supply increased 7.1% y/y and, except for February's 6.6% growth, has been over 7% since July 2016.[v]Similarly, lending rose 5.4% y/y in March, moderating somewhat from 7%+ growth rates last fall, but still adding plenty of fuel to the tank.[vi] We find it sort of remarkable that with such high money supply and loan growth, inflation is as low as it is. Even if prices inch a bit higher over the next few months, it isn't necessarily an economic negative. If the UK could handle inflation near 5% earlier in this cycle, it can probably handle this.

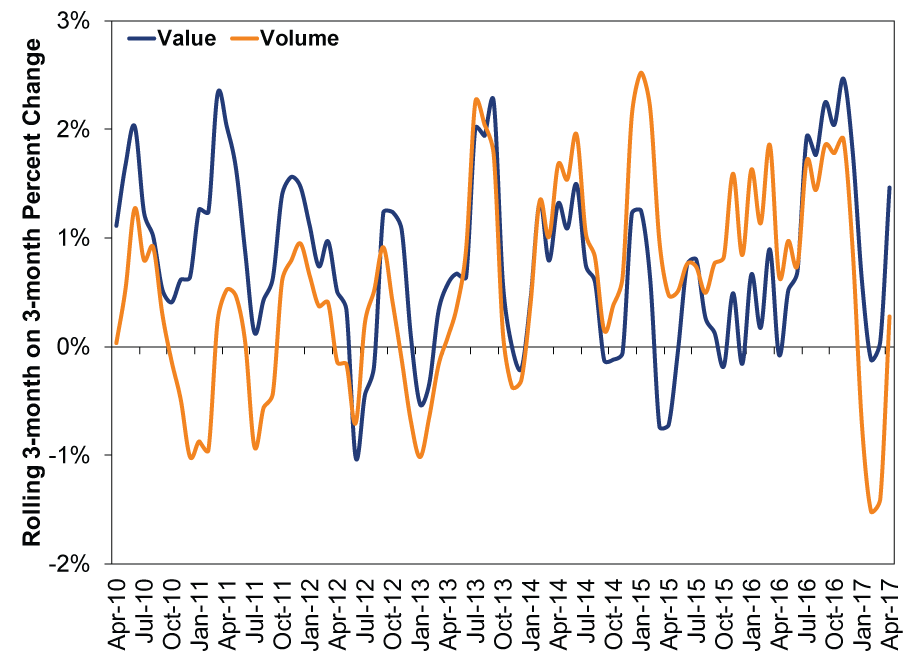

Not to overemphasize any one month's data, but there are signs the UK economy and consumers are moving past their early-2017 soft patch. While sales volumes (quantity bought) have been lackluster recently, sales values (amount spent) have mostly risen. To better view underlying sales trends obscured by month-to-month volatility, the UK Office of National Statistics prefers rolling 3-month growth rates-granted they're more backward-looking, but they make it easier to see trends. As shown in Exhibit 2, sales volumes trended lower in Q1, before rebounding in April. But the trend in sales values dipped only slightly in February and is now rising robustly again, much as it did after the handful of other sharp pullbacks earlier in this expansion. Only time will tell if the rebound continues, but for now this seems like preliminary evidence consumers continue to spend with higher prices (albeit one lacking a counterfactual-maybe folks would have bought even more if prices were lower!).

Exhibit 2: UK Retail Sales

Source: Office of National Statistics, as of 5/22/2017. Retail Sales Value and Volumes, 3-month percent change of 3-month rolling sum, April 2010 - April 2017.

Besides, retail sales are only 30% of household consumption, which continues growing thanks to services spending. More forward-looking indicators suggest growth is carrying on in Q2. April's services purchasing managers' index (PMI)-representing 80% of GDP-rose from 55.0 to 55.8, a four-month high. PMI compiler Markit noted new business expanded at the fastest pace this year with demand strong at home and abroad. April's manufacturing PMI (10% of GDP) rose from 54.2 to 57.3, a three-year high, with new orders also rising. And swift lending suggests there is ample capital to fuel growth ahead.

Although it may be hard to see through the inflation fog, the UK economy is healthy, which UK stocks already perceive-they're outperforming the world year to date. If stocks were anticipating bad times ahead, would that be happening? As inflation one-offs fade, election uncertainty is resolved and Brexit takes shape, solid underlying growth should become clearer, likely boosting markets further. Brexit uncertainty continues weighing on sentiment-as all the recession chatter can attest-but we think reality paints a considerably brighter economic picture.

[i] Source: Office for National Statistics, as of 5/22/2017.

[ii] Ibid.

[iii] Source: Bank of England, as of 5/19/2017. Effective exchange rate index, Sterling (Jan 2005 = 100), 1/2/2014 - 5/18/2017.

[iv] Excluding other intermediate other financial corporations (OFCs), which the Bank of England considers more economically relevant-"nonfinancial" money supply and lending, essentially.

[v] Source: Bank of England, as of 5/19/2017.

[vi] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today