Personal Wealth Management / Market Analysis

Witching Days Don’t Scare Stocks

Quadruple witching days don’t bode ill for stocks.

Double, double toil and trouble. So crowed the witches of Macbeth. Were they alluding to the future, and in particular, quadruple witching day? Maybe![i] If you are a trader, quadruple witching might give you the heebie-jeebies. However, stocks’ behavior on the latest quadruple witching day shows once again that if you are a long-term investor, the impact is fleeting and negligible. The things that keep by-nature short-term focused traders up at night needn’t spook you.

Quadruple witching refers to the day several types of security contracts expire: stock futures, stock index futures, stock options and stock index options. The latter two expire the third Friday of every month, but all four contracts’ expirations coincide with the third Friday of March, June, September and December—the last month of the quarter. As market participants buy and sell to replace expiring positions, some worry increased trading volume could drive volatility. But last Friday was a quadruple witching day, and it was about as placid as they come. The S&P 500 fell -0.03%, which rounds to flat.[ii]

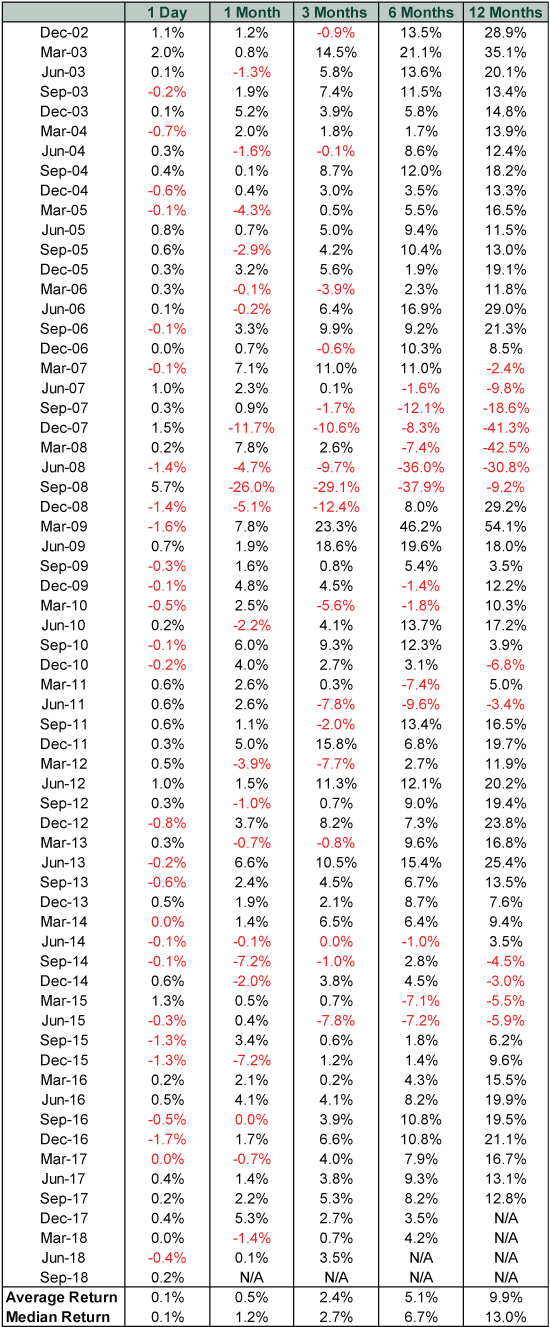

This isn’t a one-off. Quadruple witching days began when single stock futures started trading in November 2002.[iii] Since then, we have had 64 quadruple witching days. Global stocks ended the day down on 27 of them—about 42% of the time—with a median return of 0.1%.[iv] More importantly, quadruple witching days don’t beget longer market weakness. Here is a table covering all the quadruple witching days since December 2002, as well as their forward 1-month, 3-month, 6-month and 12-month returns.

Exhibit 1: Global Stocks Aren’t Afraid of Witches

Source: FactSet, as of 9/24/2018. MSCI World Index return with net dividends for quadruple witching days (the third Friday of March, June, September and December), 12/19/2002 – 9/24/2018.

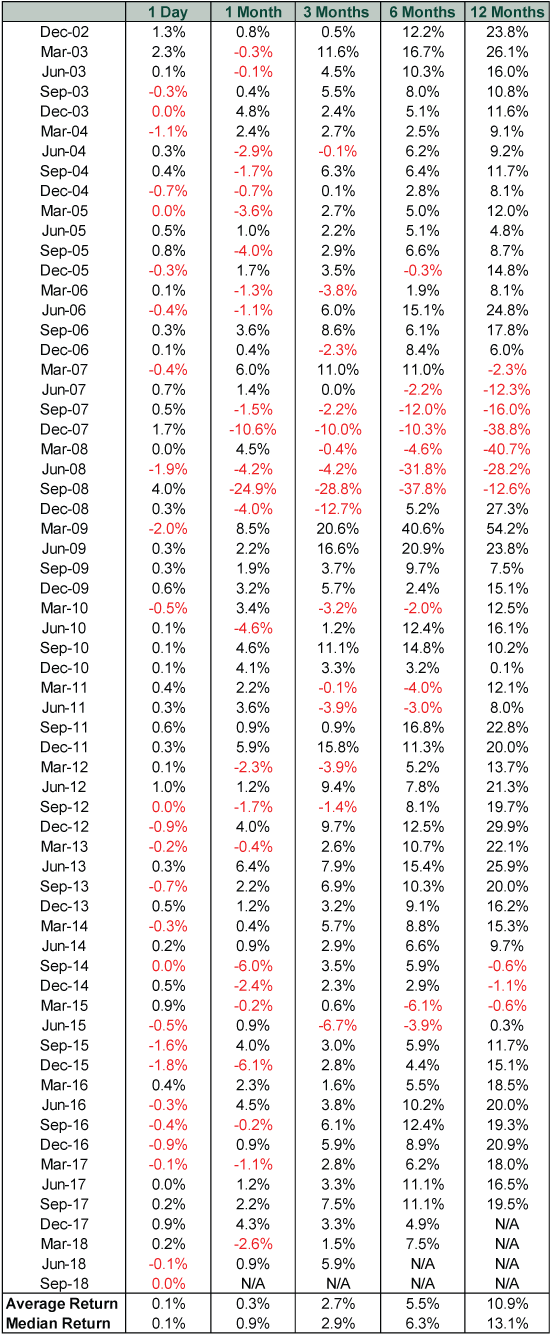

Here is the same table for the S&P 500.

Exhibit 2: US Stocks Aren’t Afraid of Witches, Either

Source: FactSet, as of 9/24/2018. S&P 500 Total Return Index for quadruple witching days (the third Friday of March, June, September and December), 12/19/2002 – 9/24/2018.

For long-term investors, this is a timely reminder not to let a single day of market activity dictate investment decisions. Even though trading volume is higher on quadruple witching days—they saw an average of 3.6 billion S&P 500 shares change hands compared to the non-witching day average of 2.7 billion shares[v]—that doesn’t automatically mean stocks will suffer. Yes, higher trading volumes could lead to higher volatility, which could hurt prices. But they could also bring the good kind of volatility that boosts stocks—or no volatility at all! After all, more trading can mean more liquidity and small price swings.

Though financial media often try to pin the day’s market activity on one or two eyeball-grabbing events, global capital markets are far more complex than that—any factor could end up affecting prices. For example, the soap opera in Italian politics could knock Italian markets. But why would that drama spill over to US markets? Similarly, why would US midterm uncertainty meaningfully affect Italian stocks? Plus, even if you could determine what influenced stock prices on one day, this has no bearing on what will happen the next day. Liquid markets also price in all widely known information, and quadruple witching days aren’t sneaking up on anyone. As Fisher Investments’ Bill Glaser succinctly put it back in March: “As ominous as it sounds, quadruple witching is essentially meaningless for long term-investors. … While it can lead to increased volume, it's a misperception it leads to increased volatility – sometimes it can on an already volatile day, but other times it doesn't.”

If you are a trader, you may have quadruple witching dates circled on your calendar since you will probably be busy that day. For long-term investors, though, volume has no real bearing on market direction and is no reason to jump out of your portfolio. Most importantly, volume doesn’t alter the economic, political and sentiment demand drivers stocks care about most.

[i] But probably not.

[ii] Source: FactSet, as of 9/27/2018. S&P 500 total return on 9/21/2018.

[iii] Before that, they were triple witching days.

[iv] Source: FactSet, as of 9/24/2018. Median MSCI World Index return with net dividends on quadruple witching days, 12/20/2002 – 9/24/2018.

[v] Source: FactSet, as of 9/27/2018. S&P 500 volume of shares traded, 12/20/2002 – 9/24/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Chart of the Day: Oil’s Substitution Effects, Illustrated2026-06-03

-

Economics Rising Credit Card Delinquencies in Context2026-06-02

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today