Personal Wealth Management /

Yield Curve Flips Positive, Sentiment Doesn’t

The US yield curve has a positive slope again, but we still wouldn’t read into it.

The US yield curve has been back in positive territory for two weeks, and pundits are starting to notice. Yet, in a fascinating sign of sentiment, they aren’t cheerful. Some warn the curve could re-invert. Others point out that the curve often turns positive again before a recession, supposedly putting us that much closer to doomsday now. But to us, these viewpoints read way too much into the yield curve’s alleged timing signals while ignoring what it means in the first place.

The yield curve, which shows the difference between long- and short-term interest rates, is a good forward-looking indicator. For one, an inverted curve—with short rates above long—has preceded nearly every US recession since WWII. However, inversion isn’t a timing tool. Rather, it is a signal of credit markets’ health. Banks borrow at short rates, lend at long and profit from the spread. Hence, a positively sloped curve—long rates above short—means lending is profitable, creating incentive for banks to lend to a wide swath of borrowers. A flat or inverted curve implies lending is less profitable—or unprofitable—which can tighten credit, starving the economy of capital. If inversion is sufficiently deep, widespread and lasting, it can lead to recession as a lack of credit forces businesses to cut back.

After a brief blip into inversion in March, on May 24 the US yield curve inverted and stayed that way for most of the next four-and-a-half months. Several curves in Europe followed suit, even inverting the global yield curve for a spell. But on September 5, long-term interest rates began rising. On October 14, the US curve officially un-inverted (or, if you prefer, unverted).

Exhibit 1: The Yield Curve Is Positively Sloped Again

Source: FactSet, as of 10/23/2019. US 10-Year Treasury yield (constant maturity) minus 3-Month Treasury yield (constant maturity), 1/2/2019 – 10/22/2019.

Folks clinging to fears offer a few reasons why “unversion” isn’t necessarily a positive development. One school of thought cites yield curves’ tendency to return to positive territory before a recession actually begins, arguing the return to normal suggests recession might be closer than many think. In our view, this reads too much into yield curve wiggles and ignores the history of false signals. Even if the theory ends up correct eventually, it doesn’t help investors decide what to do in the here and now. Another says the unversion isn’t that meaningful because it happened for “technical” reasons (e.g., the Fed’s planned short-term bond purchases) and enthusiasm over US/China trade talks, not a general change in investors’ economic outlook. We think this errs in ignoring why the curve matters in the first place. It matters less why it inverts/uninverts because the signal for banks, and the effect on their eagerness to lend, is roughly the same.

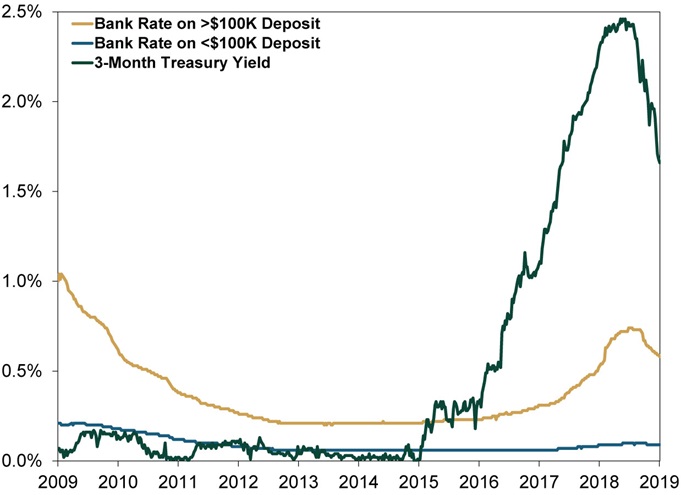

Even with the unversion, our viewpoint hasn’t changed. We still think pundits are making too big of a deal out of it. Practically, not much has changed. The yield curve isn’t meaningful because it is a gauge of expectations, as many allege. Rather, as noted earlier, it influences banks’ profits and lending. But it isn’t a perfect guide. Banks don’t borrow and lend at government rates. Their funding costs and loan rates are both set in the open market. As we noted when the curve inverted in March, banks’ funding costs have trailed US government rates since the Fed began raising overnight rates, thanks to a glut of deposits relieving banks of the need to compete for funding by offering higher rates. These rates remain low.

Exhibit 2: Bank Funding Costs Remain Low Relative to Treasury Yields

Source: FactSet, as of 10/21/2019. Three-month Treasury yield (constant maturity), national jumbo and non-jumbo deposit rates, 10/16/2009 – 10/18/2019.

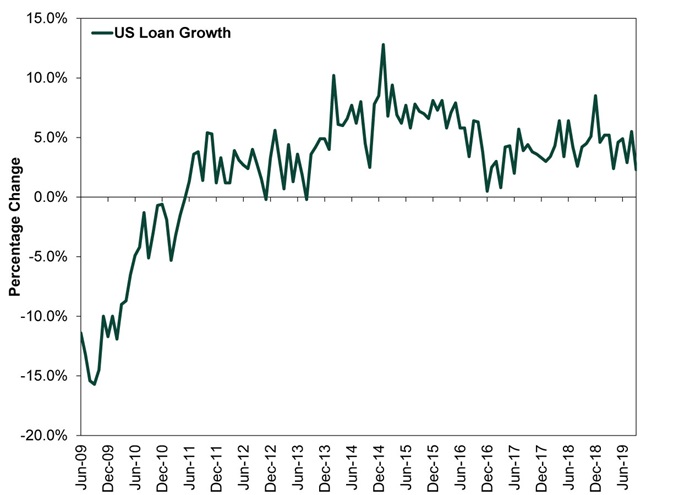

Similarly, mortgage rates and prime business loan rates exceed long-term government bond yields, as one would expect given the higher credit risk involved. Thus, even while the yield curve was inverted, banks enjoyed decent loan margins, keeping loan growth alive and well. Banks were also—and remain—able to take advantage of even cheaper funding in Europe and Japan, where short rates are negative, to further juice loan profits in the US. Exhibit 3 illustrates how loan growth keeps humming along regardless of recent yield curve wiggles.

Exhibit 3: US Loan Growth During the Current Expansion

Source: Federal Reserve Bank of St. Louis, as of 10/28/19. Month-over-month percentage change in loans and leases in bank credit, seasonally adjusted annual rate, June 2009 – September 2019.

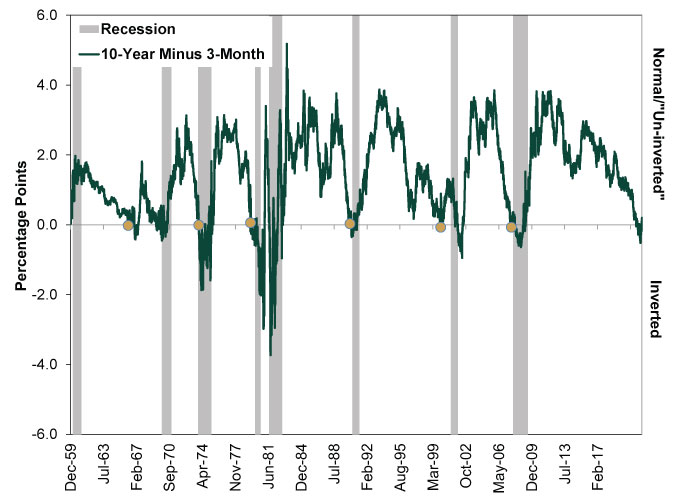

It is true that the yield curve sometimes uninverts before recession begins. But it is also true that not every inversion precedes recession. False signals have happened, and they can give folks the wrong impression of what lies ahead. Today’s unversion just tells you that this could be a false signal …or a prelude to recession. That isn’t very helpful, in our view.

Exhibit 4: Inversion Isn’t an Instant Recession Trigger

Source: Global Financial Data and FactSet, as of 10/24/2019. US 10-Year (constant maturity) Treasury yield minus 3-Month (constant maturity) Treasury yield, 12/31/1959 – 10/23/2019. Recession dating via NBER. Pre-recession initial inversion dates indicated in yellow.

The recent unversion doesn’t prove recession isn’t looming, but we don’t think it needs to. Markets and the economy have persevered throughout 2019, despite the curve flipping between positive and negative along the way. A return to a slightly positive slope in the yield curve is nice, but it hardly changes anything when assessing the US’s current economic outlook, which remains better than many appreciate.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today