Personal Wealth Management / Politics

Your Best Hedge Against Beltway Theatrics

Hint: It involves owning stocks.

At the risk of stating the obvious, things have been rather eventful in Washington, DC the last couple weeks, and stock market volatility has accompanied the theatrics. The S&P 500 suffered its worst day in months on Tuesday and even with a late-week comeback, it inched downward for the second week in a row. As we wrote a few days ago, political scandals aren't inherently bearish, nor are heads of states' impeachments or resignation (not that we believe either is likely, as we also explained). However, if you're worried about the goings on, that is not a reason to exit stocks. Rather, in our view, your best hedge against all the leaks, innuendo and rumors in DC is a global portfolio.

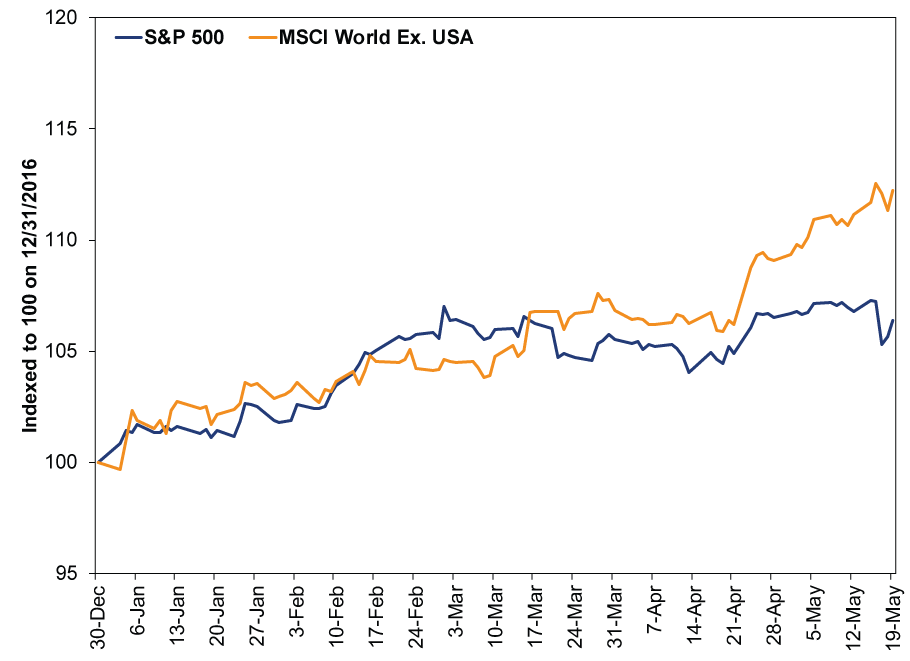

Global investing's biggest benefit is diversification-including diversification against political risk in any one country. Case in point: While US stocks dipped a bit recently, non-US stocks rose. Non-US stocks are handily beating the US year to date, and their lead widened as America's political theatrics heated up. As we type, their year-to-date return is nearly double the S&P 500's.

Exhibit 1: To Hedge Against US Political Risk, Invest Globally

Source: FactSet, as of 5/22/2017. S&P 500 Total Return Index and MSCI World Ex. USA Index with net dividends, 12/31/2016 - 5/19/2017.

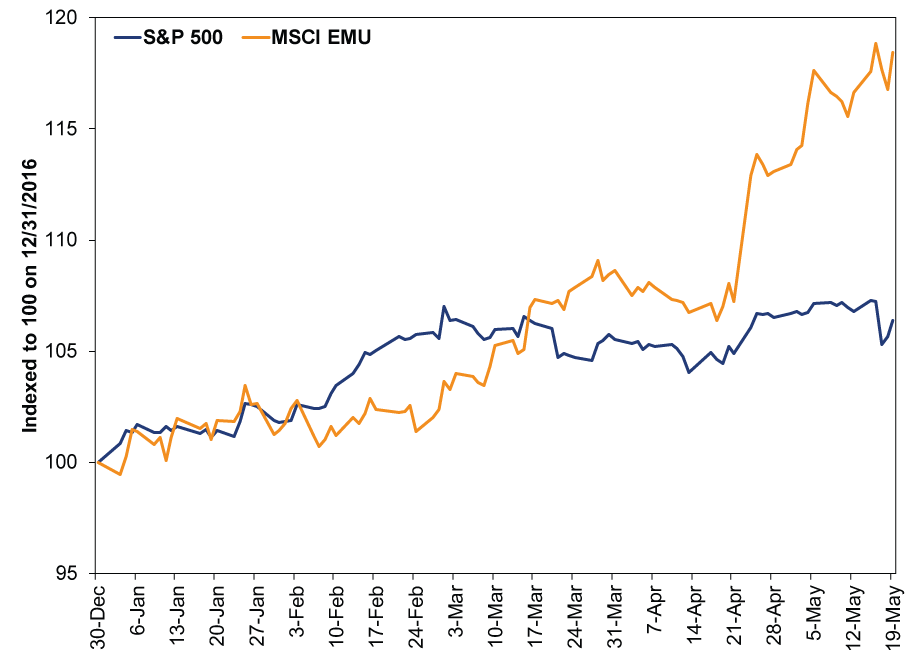

The great thing about investing globally is, not all countries are in the exact same situation, letting you capitalize on happier trends in other places. Political uncertainty might be rising a wee bit in the US right now, but it is not up across the board in all of the MSCI World Index's 22 other countries. In much of Europe, for example, it's falling-first with the Dutch election, then the French election, then some regional German elections, and most recently Sunday's Socialist Party leadership election in Spain. Talk of early Italian elections has died down a bit, and Germany's federal election in September looks likely to extend the status quo of a pro-euro coalition government. This clearing fog has been great for eurozone stocks, whose year-to-date returns are almost triple the S&P 500's.

Exhibit 2: Eurozone Stocks Love Falling Political Uncertainty

Source: FactSet, as of 5/22/2017. S&P 500 Total Return Index and MSCI EMU Index with net dividends, 12/31/2016 - 5/19/2017.

While today's other widely hyped risks to US stocks are similarly overstated, non-US exposure is also a hedge against them. Worried about the Citigroup Economic Surprise index for the US spending the last several months in negative territory? Own eurozone stocks-Citi's Economic Surprise Index for the eurozone is high and rising. Worried about America's flattening yield curve? Well, most curves in Europe have steepened. Worried S&P 500 valuations are inflated and show sentiment is getting too hot? P/E ratios are lower in Europe, where sentiment is only just starting to warm up after years of post-crisis blues. And if for some reason you think S&P 500 earnings growth is too low at 13.7% y/y in Q1, you can always take comfort in the MSCI EMU's 31.3% Q1 earnings growth.[i] That last one is a joke, but only sort of.

Again, we aren't saying any of what has transpired in US politics over the last two weeks is inherently a risk for US or world stocks. Not based on what information is out there already. Nor has anything fundamentally changed. Washington DC is still gridlocked, and it would be even if the last two weeks never happened. We still think US stocks will have a fine year, and we don't believe excluding them from a diversified global portfolio right now makes sense. But we think owning a large chunk of non-US stocks alongside them is the best way not only to limit your risk, but to capitalize on opportunities the world over.

[i] FactSet Q1 2017 blended earnings growth estimates for the S&P 500 and MSCI EMU Indexes as of 5/22/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today