Personal Wealth Management / Politics

The Voters Have Spoken

What to expect from markets under a President Trump.

Photo by Scott Olsen/Getty Images.

Editors' Note: Our political commentary is nonpartisan and non-ideological by design as political bias is a dangerous investing error. We favor no political party or candidate and assess politics solely for potential market impact.

The voters spoke, and while the final few precincts are trickling in, Hillary Clinton has conceded the race and Donald Trump will be America's next President. The Republicans will keep both houses of Congress, losing only a handful of seats. S&P 500 futures plunged as the news developed, but later cut losses. In our view, you should stay cool: Short-term volatility is normal, and this too should pass. Looking forward, markets move most on the gap between reality and expectations. People fear Trump's campaign pledges, but politicians' promises rarely become reality. As Trump does less than people fear, we expect markets to get plenty of relief. In our view, a less-bad-than-feared Trump should be a positive surprise for stocks in 2017.

Tuesday night's theatrics remind us of the Brexit vote: Now, as then, the real losers are the pollsters, media and political sages who presumed polls were airtight. As markets closed Monday, most pointed to gains in the S&P 500 and record inflows into the biggest US-listed Mexican ETF as signs Clinton would win-just as UK stocks' gains on June 23, Brexit day, supposedly telegraphed a Remain win. When Leave pulled ahead as votes were tallied, the pound and stock futures tanked-just as S&P 500 futures tanked Tuesday night, as a Trump victory grew likelier. In the two trading days after the Brexit vote, world stocks fell -7.1%, and UK markets lost -5.6%.[i] But on day three, the tide turned. Investors who based their forecasts and decisions on polls got over their shock, and stocks recovered. It wouldn't surprise us at all if we saw a similar drop this time-volatility tied to a winner people didn't expect and most in the investment world didn't want-but it, too should pass. The immediate reaction to Brexit didn't tell you how things would ultimately be, and nor does the immediate reaction to Trump. Markets will readjust and move on. The more they see Trump can't do as much as he says, the happier they should be.

Expectations Versus Reality and a Bit of History

While politics are just one driver-and it's premature to forecast economic and sentiment drivers-political winds should boost stocks next year as markets treat Trump the way they'd normally treat a new Democratic president.

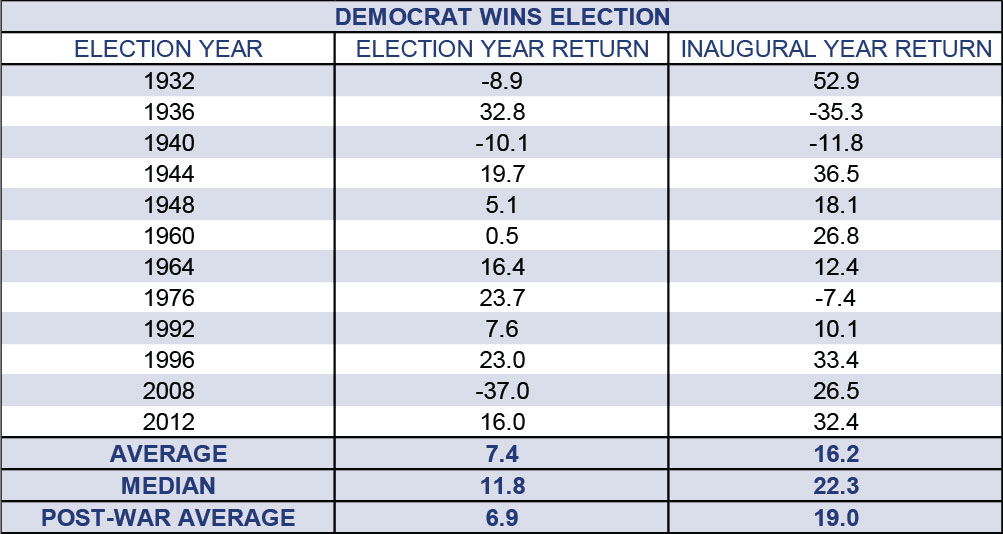

Historically, when Democrats win, returns are below-average in the election year-just 7.4%, since 1928-and stronger in the inaugural year, averaging 16.2%.[ii] Under Republicans, it's the opposite-stronger returns in the election year (15.5% on average) and weaker the next (0.7%).[iii] Presidents' tendency to break campaign pledges gets much of the credit for this, in our view. Usually Democrats run on anti-business platforms, making investors run for the hills, and then relieve markets when they don't see most of those promises through. Either they moderate, already eyeing re-election campaigns and the need to keep Independents in the fold, or Congress gets in the way. Republicans, meanwhile, usually make pro-market promises, boosting sentiment when they win, but disappointing investors the next year when they, too, get very little done.

Trump isn't your typical market-friendly Republican. Anti-trade talk scared the pants off Corporate America. No Fortune 100 CEO endorsed him. Hostile Wall Street Journal op-eds were a regular occurrence. His corporate tax cut might appear pro-businesses, until you realize he'd end deferred taxation of US firms' overseas profits, instead taxing them immediately. Most investors saw little to cheer and everything to fear-just as they typically do with new Democratic presidents.

That sets expectations at rock-bottom, which stocks like. It won't take much for markets to get a positive surprise-a President Trump that does less than feared and is less bad than feared should do it. When markets expect disaster, anything less than disaster is a relief, and relief brings rallies. Returns this year are fully consistent with a feared election outcome, which we believe tees up markets for big, happy political surprise potential for 2017.

Exhibit 1: History of Returns Under Democrats

Source: Global Financial Data, as of 11/4/2016.

Gridlock, Gridlock, Gridlock

While Republicans maintain control of Congress, Trump will likely be at loggerheads with his own party. A good-sized chunk of the GOP's Congressional firmament was part of the #NeverTrump movement. Several refused to endorse him. Some publicly said they'd vote for Hillary Clinton. Trump doesn't forget these things. Those who were at war with him during the campaign will be at war with him in Congress. They might be relegated to the back of the bus within the Republican Party hierarchy, but they'll fight back. They can still point to their victories and say "Hey, voters picked me and my platform, and I won't back down-I'll trump Trump." This bloc should be a powerful resistance within the GOP.

A GOP, we should add, that won't have a filibuster-proof majority. Even if all the #NeverTrumpers drank some funny Kool-Aid and got on board with everything The Donald wanted, Democrats could talk any sweeping new laws to death.

Then, too, Trump isn't winning with a huge mandate. However lopsided the Electoral College might ultimately look, anyone staying up late Tuesday night knows it was close. America didn't broadly tip one way-this wasn't a landslide a la Reagan or Obama. It was narrow split between urban and rural voters, much as Brexit was.

Ronald Reagan once said truly great presidents might get three or four major initiatives passed-we're talking hugely popular guys with big mandates and dynamite horse-trading skills. If they're less skilled, have less support or waste political capital on partisan bickering and party in-fighting, they get less done. President Obama enjoyed a Democratic supermajority during his first two years, and he got just two big laws-Dodd-Frank and the Affordable Care Act-and both were watered down significantly from initial proposals. A President Trump with a thin Republican majority and intraparty resistance probably does even less.

Don't Overrate Presidential Politics

It is crucial not to overrate the presidency in your market outlook. Politics are only one driver of demand for stocks, the others being economics and sentiment. America is also only about 25% of world GDP, so actions taken by the US government do not have the reach to unilaterally affect the world economy. Many also overrate presidents' ability to enact change unilaterally. The Constitution limits their power, requiring Congress to approve most tax-and-spend and legislative decisions. Trade policy is a wild card, as Congress has ceded some authority to the president, but that isn't reason to be bearish today. US presidents have a long history of spouting anti-trade rhetoric on the campaign trail, then U-turning once in office. Bill Clinton campaigned against NAFTA, then signed it. Ditto for Barack Obama and the free-trade deals with South Korea and Colombia. Threatening tariffs against China over currency manipulation and "dumping" subsidized exports is basically a campaign requirement, but no one ever follows through.

Political reality could easily get in the way of Trump's trade pledges. Legally, perhaps he could pull the US from NAFTA. But alienating all those in the services, logistics and retail sectors whose jobs depend on NAFTA would be an odd move indeed. Remember, a first-term president's goal is always to be re-elected. Everything else comes second. In other words: Watch what he does, not what he says.

The Executive Branch can issue executive actions and regulatory shifts, but these are narrow in scope and subject to challenge in court. Two June decisions illustrate this perfectly, one involving Department of the Interior regulations governing fracking on federal lands, the other regarding President Obama's shielding select undocumented immigrants from deportation. In both cases, several states challenged the feds authority on constitutional grounds. The courts agreed. Love or hate the rulings, the law is the law. The law governed all. Markets will slowly realize this. While many are unhappy (and others joyous) over the presidential election's result, remember: It is only one vote affecting one third of the US government, one of three drivers affecting a quarter of world GDP. It isn't the be-all, end-all.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today