Business 401(k) Services / Plan Administration

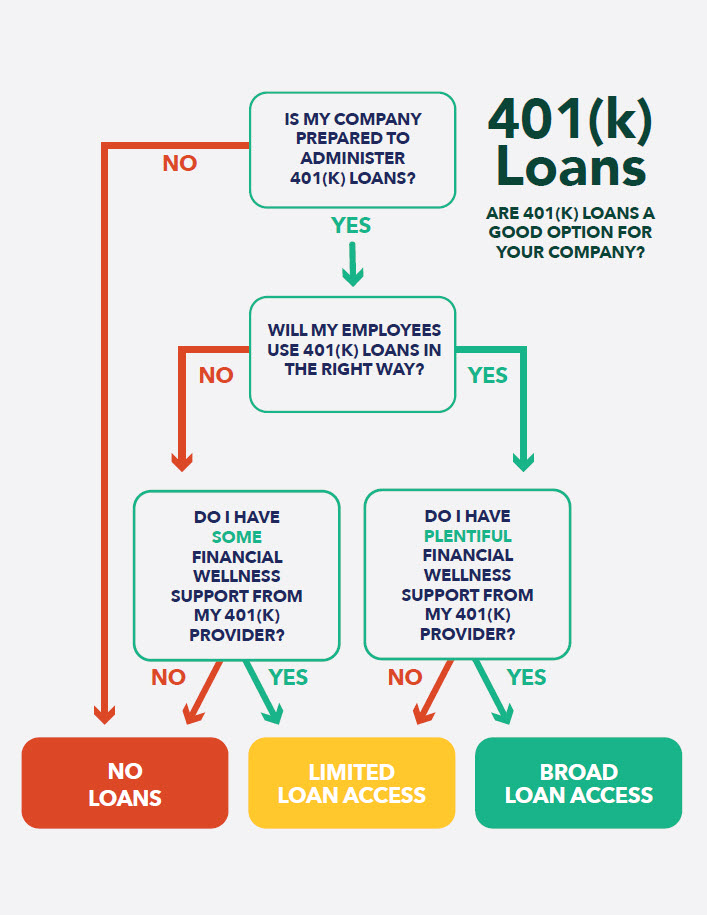

401(k) Loans: A Good Option for Your Company?

As many as 87% of employees enrolled in a 401(k) have access to a loan of some kind, but is offering a 401(k) loan option a good decision for your company? It’s not always a simple “yes” or “no” question. I regularly have a discussion on this very topic with employers when designing 401(k) plans. Here’s how I see it.

On one hand, offering loans can go a long way towards helping employees feel more comfortable enrolling in your company’s 401(k) plan. Employees like knowing that they can have access to their savings in a pinch. In the right circumstances, a 401(k) loan can be a viable way for your employees to get short-term funds in an emergency situation.

On the other hand, 401(k) loans are frequently misused. When utilized incorrectly, they can pose a real threat to someone’s retirement preparedness. They also require a lot of extra administrative oversight, which might not be easy for some employers to support.

Depending on your situation, you might have success offering 401(k) loans with broad access for your employees, or you might do better offering limited loans or avoiding loans altogether. To help you see where you fall on this spectrum, I’ve developed a flowchart.

With the answers to three “yes” or “no” questions, you can get a better understanding of what it would take to offer 401(k) loans, and whether it’s a good option for your company or not.

1. Is My Company Prepared to Administer 401(k) Loans?

Adding loans to your plan will require a number of new processes for organizing amortization schedules, determining what to do in the case of a missed loan payment or default, and also managing another line item in payroll for contributions to pay back loans.

The easiest way to determine whether your business is ready to take on this responsibility is to review what it’s like to manage payroll currently. For example, managing payroll data for 401(k) could be a fairly automated process for some employers, while others handle this information manually. You know best what your payroll process looks like. If the idea of adding even more complexity gives you anxiety, you may not be ready to offer 401(k) loans—that puts you at our first destination, No Loans. If not, you can move one step further to a question about your employees.

2. Will My Employees Use 401(k) Loans in The Right Way?

Once you’re prepared to administer 401(k) loans, the next step is to imagine how your employee base will use loans. If you choose to offer loans, will your employees use them in the right way? There are some uses for loans—a short-term need for funds, like an emergency home repair, for example—that are better than others. Retirement savings need to stay invested to keep an employee on track for retirement, so the use of 401(k) loans outside of emergencies is not ideal.

Generally speaking, a good use of 401(k) loans meets the following criteria:

- There is no alternative option. Taking a 401(k) loan should be a last resort. If no other option exists to cover the emergency need—no savings, no credit card, no quick insurance payout, for example—a loan might be the right option.

- The employee will be able to continue saving and earning interest while repaying the loan. Most 401(k) loans are set up to be repaid over 5 years. That’s a long time for an employee’s retirement savings to not be invested or earning any interest. Additionally, for some employees, repaying a 401(k) loan will mean they will not be able to continue contributing new savings to their 401(k) account. In these situations, a loan can take a big cut out of someone’s retirement savings.

- There is little risk of default. When an employee with a loan leaves your company, their loan will most often be due in full within 60 days. If that isn’t paid, the balance will be taken out of their 401(k) savings, and they’ll also have to pay taxes and a 10% early withdrawal penalty. I’ve seen loan defaults like this virtually wipe out a person’s savings. It’s not pretty.

With this checklist in mind, one way to determine how easy it will be for your employees to use loans in the right way is to consider how often people change jobs. If you’re in an industry with a lot of turnover, there could be a higher potential for default as employees leave and find their loans come due quicker than they’d planned.

Whether you’ve decided that your employees are likely to use 401(k) loans correctly or not, there’s one more question to answer to determine your best course of action, and it has to do with financial wellness.

3. Do I Have Sufficient Financial Wellness Support From My 401(k) Provider?

If you answered “no” to our last question—“Will my employees use 401(k) loans in the right way?”—you may still be able to offer loans as long as you do receive plenty of financial wellness support from your 401(k) provider. While you may receive some level of support, “sufficient” support means having access to a wide range of resources to help employees make good decisions with the plan, like one-on-one counseling; educational resources about budgeting, debt management, and retirement planning; and tools like retirement calculators.

Without this kind of support, you may end up at No Loans. If you do get this help, then you’ve arrived at Limited Loan Access. This means you may want to offer loans, but with certain restrictions like offering only one loan at a time per employee, or increasing fees or interest rates to encourage correct use.

I recently assisted an employer—the owner of a business in the auto industry—who fit perfectly into the category of offering limited loan access. For years, he’d offered loans to his employees out of his own pocket, but he was interested in exploring another way to provide this service to his employees. His HR administrator was hesitant to manage 401(k) loans because of the extra administrative work. This employer chose to limit loans to one per employee, and to also require that employees come to us for counseling before moving forward with a loan. He made this decision to limit the number of loans within the plan, and also to decrease his personal risk.

If you answered “yes” to our question about employees being likely to use loans in the right way, then you may be in a good position to offer Broad Loan Access. As long as your 401(k) provider is dedicated to offering financial wellness support, your employees may benefit from easily accessible 401(k) loans. Otherwise, you can consider offering Limited Loan Access to encourage your employees to only use loans under the right circumstances.

There are pros and cons to every final decision you can make about offering 401(k) loans in your plan, but I hope this clarifies your decision making process. Whatever your choice, keep in mind that while loans can be a valued part of your company’s 401(k) plan, they aren’t the most important part. Keep focused on the true benefit of your plan: Helping your employees save for a secure retirement.

See our Business 401(k) Insights

Resources and articles to help your business with retirement plan support, optimization and administration.

Business 401(k) Resources by Topic

-

401(k) Plan Optimization Your Interests First1/1/2023 12:00:00 AM

-

Plan Administration How to Find the Best 401(k) Provider1/1/2023 12:00:00 AM

-

Plan Administration 401(k) Employee Services1/1/2023 12:00:00 AM

-

401(k) Plan Optimization Investment Analysis1/1/2023 12:00:00 AM

Contact Us

One of our 401(k) business specialists would love to talk to you about your company’s retirement plan needs.

Call Us

Get Me Started