Business 401(k) Services / Start a 401(k)

What Business Owners Should Know About OregonSaves

Many states are committed to making it easier for Americans to save for retirement, for some states this includes providing a system that gives more American workers access to a retirement plan.

Oregon has been a leader in this charge by providing the OregonSaves Plan, and implementing legislation requiring businesses to provide a retirement plan for their workers.

It’s important for business owners in Oregon to understand how this legislation affects them, and to know their options. We’re here to help. This Frequently Asked Question blog provides important information for business owners in Oregon including details of the OregonSaves program, alternative choices and more.

What Is OregonSaves?

OregonSaves is a mandate requiring all Oregon business owners to provide a retirement plan to their employees. The mandate was effective starting November 2017 and requires business owners to either sponsor a 401(k) plan (or other qualified retirement plan) or adopt the state-run OregonSaves retirement plan.

How Does The OregonSaves Plan Work?

The OregonSaves plan is a payroll-deducted Roth IRA that is run by the state of Oregon. If an employer adopts the OregonSaves plan, all of their W-2 employees are eligible to participate (including part-time workers). The program is auto-enrolled at 5%, which means unless employees proactively opt out, they will be automatically enrolled to contribute 5% of after-tax income into the plan.

What Features Are Included In The OregonSaves Plan?

The OregonSaves plan includes the following features:

- Auto-enrollment at 5% (i.e. employees will be automatically enrolled to contribute 5% in the plan unless they proactively opt out annually)

- Auto-escalation (i.e. employee contributions will be automatically increased by 1% annually (up to 8%) unless they proactively opt out annually)

- Annual contribution maximum of $7,000

- Roth only contributions (no pre-tax option)

- Does not allow loans

- Does not allow employer contributions

- Limited to employees with annual income < $165,000;

Do Employers Have To Offer The OregonSaves Plan?

Oregon business owners do have to offer a retirement plan, but it doesn’t have to be the OregonSaves Plan. Business owners who offer a 401(k) (or other qualified retirement plan) may be exempt from the mandate but must certify their plan with the state of Oregon. Other qualified retirement plans could include 403(b), SEP IRA, and SIMPLE IRA.

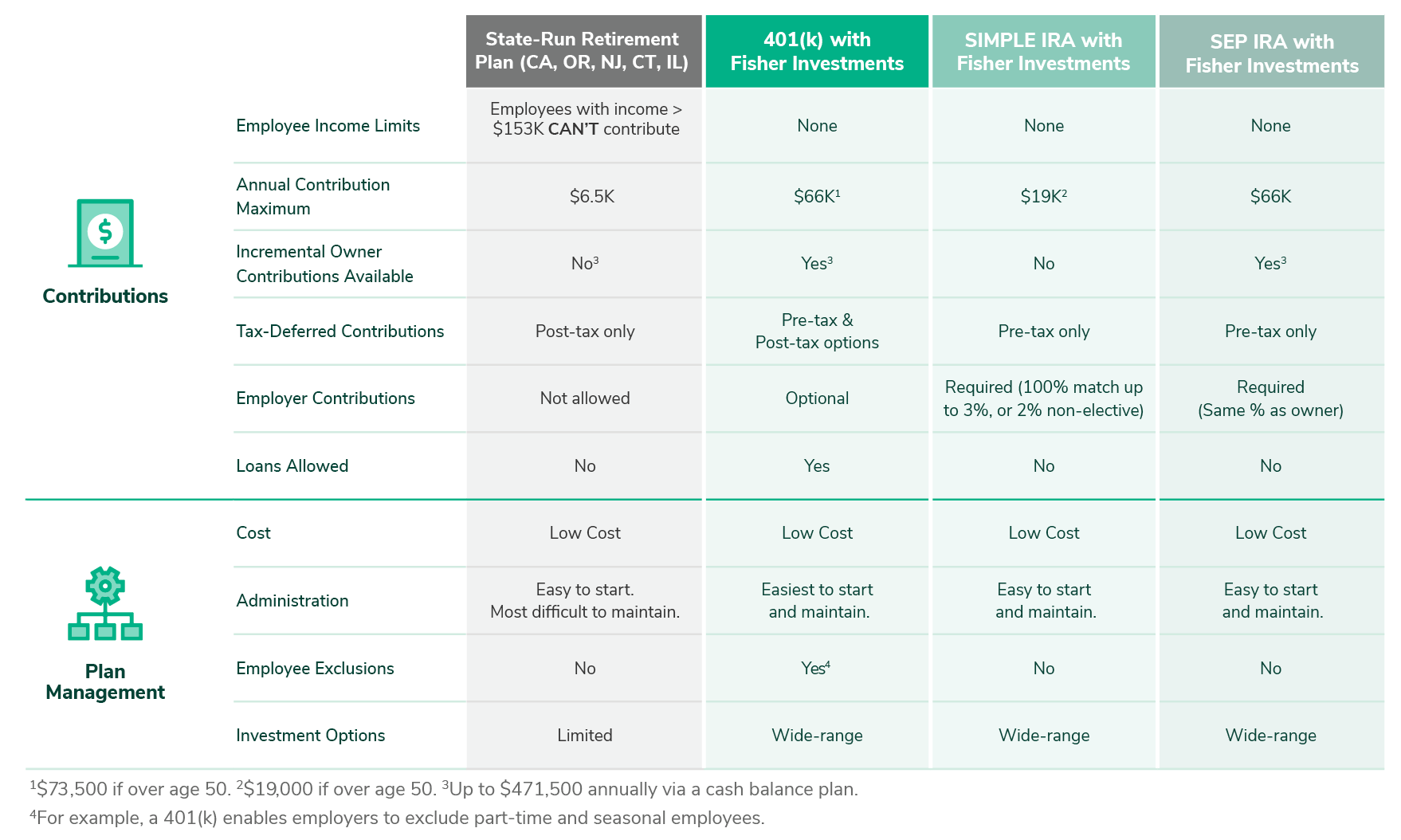

How Does OregonSaves Compare to Other Plan Options?

See how OregonSaves compares to other retirement plan options in this state-mandated IRA comparison chart here:

Does OregonSaves Apply To All Businesses?

OregonSaves applies to any employer who has 1 or more W-2 employees age 18 or older in Oregon. This includes non-profits.

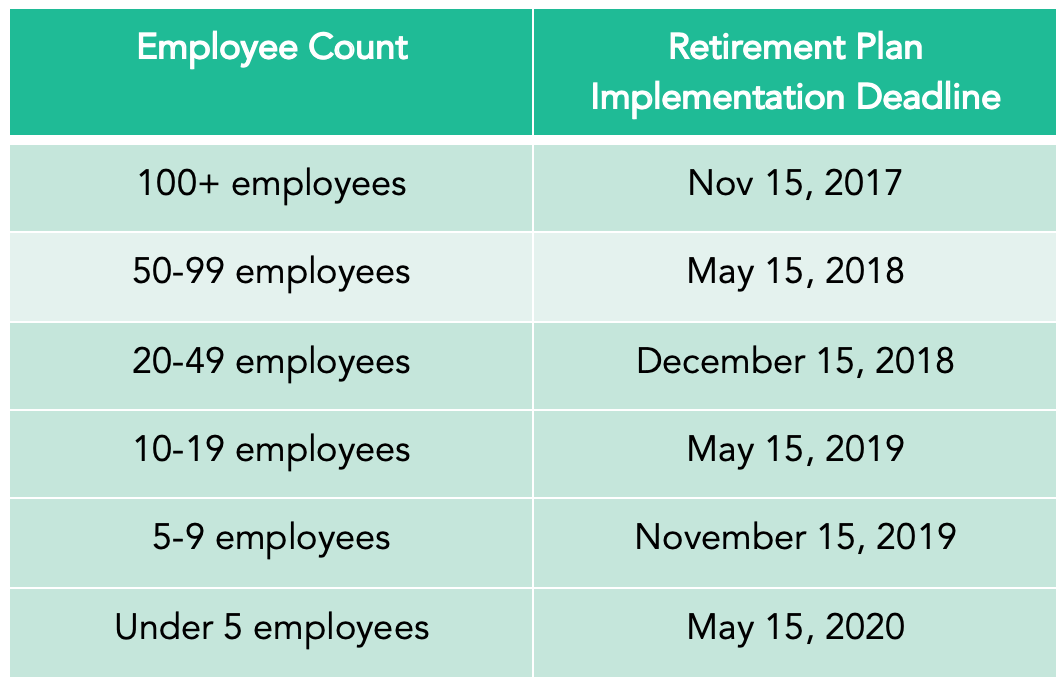

When Is The Deadline To Implement A Retirement Plan In Oregon?

The deadline to implement a retirement plan in Oregon depends on how many W-2 employees (18 or older) your business has:

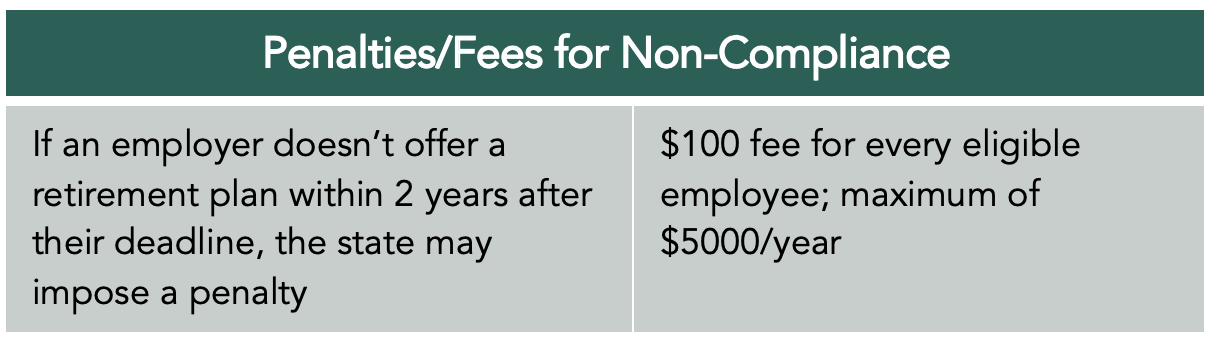

What Are The Penalties For Non-compliance With OregonSaves?

Companies who fail to comply with the OregonSaves mandate could be subject to a fee of up to $100 per eligible employee. Good news, it’s really easy to comply by setting up a 401(k) plan (or another qualified plan)—click here to find out how.

How Much Does OregonSaves Cost??

The OregonSaves plan cost is 1.05% of assets; this fee is deducted from each employee account balance. For example, if an employee has $100K in the retirement plan, $1,050 a year will automatically be deducted out of their balance. There is no direct cost to the employer, but there are substantial administrative tasks that need to be carried out by the sponsor on an annual basis.

What Do Employers Have To Do To Administer The OregonSaves Plan?

OregonSaves creates a significant administrative burden for the employer.

Employers must:

- Submit an employee census to OregonSaves annually

- Track eligibility status for all employees

- Provide enrollment packets to all employees 30 days after date of hire

- Track whether each employee has opted in or out

- If employee doesn’t opt out within 30 days of notification, set up 5% payroll deduction

- Answer questions from employees who have been auto-enrolled

- Manually auto-escalate all employees annually (unless they’ve opted out)

- Repeat auto-enroll process annually for all employees who have opted out

- 6-month look-back for auto-escalation:

- Track if employee has been participating for 6 months with no auto-escalation

- Provide 60-day notice that they will be auto-escalated Jan 1st if they do not opt out again

- Hold open enrollment every 2 years

- Auto-enroll anybody who hasn’t been participating for at least 1 year (these have to be tracked)

Fisher Investments provides affordable, hassle-free solutions that reduce the administrative burden on employers. Explore your options here.

See our Business 401(k) Insights

Resources and articles to help your business with retirement plan support, optimization and administration.

Business 401(k) Resources by Topic

-

401(k) Plan Optimization Your Interests First1/1/2023 12:00:00 AM

-

Plan Administration How to Find the Best 401(k) Provider1/1/2023 12:00:00 AM

-

Plan Administration 401(k) Employee Services1/1/2023 12:00:00 AM

-

401(k) Plan Optimization Investment Analysis1/1/2023 12:00:00 AM

Contact Us

One of our 401(k) business specialists would love to talk to you about your company’s retirement plan needs.

Call Us

Get Me Started