Personal Wealth Management / Market Analysis

A Greece-y State of Affairs

Is the eurozone at risk of a Greek contagion?

Greece is the word these days, and to many, the word doesn't sound good. Syriza's coalition government is fraying, and there is already talk of a new unity government to prevent a "Grexit." Prime Minister Alexis Tsipras sought a bailout from Russia[i] and received Russian "President" Vladimir Putin's "moral support and long-term cooperation" (along with unspecified offers to buy state assets). Greece restated its claims Germany owes it about €280 billion ($300 billion) in WWII reparations. Greek banks are issuing government-guaranteed debt to keep themselves afloat. After repaying a €458 million IMF loan Thursday, leaders claim they lack cash for April's state salary and pension obligations. Greece is turning into a swirling saga of allegation and denial, wild ideas and tame rejection-possibly a case of game theory gone awry. Yes, things are increasingly bizarre, with pundits ever-surer Greece is hurtling toward a eurozone exit. And hey, anything is possible, despite all participants' well-demonstrated penchant for kicking the can. Whatever the outcome, though, markets have long since moved on from Greece-we see no evidence a Greek contagion is at all likely or a threat to the rest of the eurozone, let alone global markets.

While Greece's hubbub has some new twists, it's the same movie we've seen since 2010. Treasury payments loom, banks are hemorrhaging cash, government needs money, creditors have conditions, politicians are politicking, and everyone fears Greece will eventually have no choice but to leave the euro and print fistfuls of drachmas to stay afloat. This time Greece has about €6 billion due to various creditors over the next four weeks and needs to pay state employees, but the government claims its coffers are depleted-hence their effort to unlock €7.2 billion in previously agreed (and recently extended) bailout funding.

Compounding matters, the ECB has cut off its primary lifeline for Greek banks, leaving them to get cash from the Bank of Greece (which then taps the ECB). Cash banks are accessing by using their own short-term commercial paper as collateral-paper that carries a Greek government guarantee, hence meeting the central bank's requirements. If a bank fails, the technical term would probably be "kablooey." Will Greece miss payments, defaulting? If so, will default mean bye-bye euro? Will bank failures force it out of the eurozone? Tsipras promises he and his cabinet will work through this weekend's Easter holiday to reach an agreement at April 24's meeting of eurozone finance ministers. They've all compromised before and could do so again, but, you know, game theory. Germany might be less willing to help with those WWII demands (and related threats to seize German assets) swirling.

But here's the thing: Surprises move markets. No matter how bad things get in Greece, would it really be a surprise? Some followers of Sentix's "Contagion Risk" index argue yes, highlighting the fact only 36.8% of respondents expect one or more countries to leave the euro within the next year[ii]-interpreting it to mean the majority will be caught unaware and are too complacent. That's juuuuuuuuuuuuuust a bit of a stretch, in our view. One, it's a survey-it tells you only what people say, not necessarily what they do. Two, just because 63.2% of respondents evidently don't think Greece will leave doesn't mean they aren't aware it is possible, haven't heard the chatter or even based some investing decisions on it. And regardless of whether or not people believe Greece will go, is anyone truly surprised by anything that has happened this year? Nothing here is new. Greece has been a basket case for five years-ancient history in markets, if not Greek culture. In those five years, they've had two defaults, two bailouts, four governments, a dozen or so standoffs with creditors and well over a thousand media articles hyping their imminent departure, which often use one of two portmanteaus coined for the feared event.[iii] Wobbly banks? The last four years have been one slow bank run.

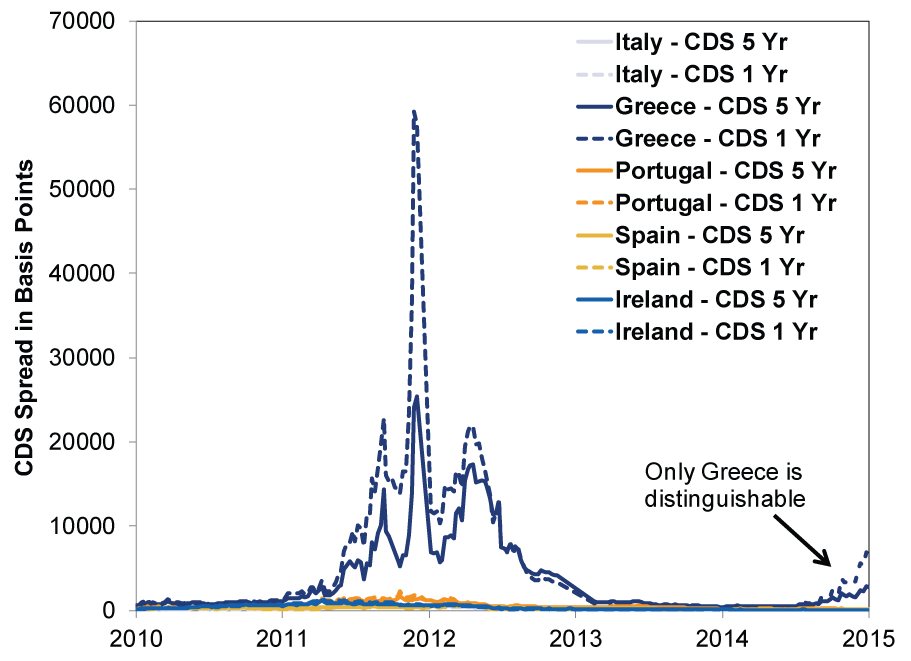

Don't take our word for it-ask the market! It will tell you that yes, Greece is a mess, but it isn't a ginormous risk for other countries. Greek credit-default swaps-the cost of insuring debt against default (relative to Germany, considered the Continent's lowest default risk)-are rising fast. (Exhibit 1) But other peripheral nations' debt insurance costs have barely budged. Considering all liquid markets price widely known information near-simultaneously, it's highly likely Portuguese, Irish, Spanish and Italian CDS markets have already factored in Greece's default risk.

Exhibit 1: 1 & 5 Year CDS Spreads from April 2010 - April 2015

Source: FactSet, as of 4/9/2015. From 4/9/2010 - 4/9/2015.

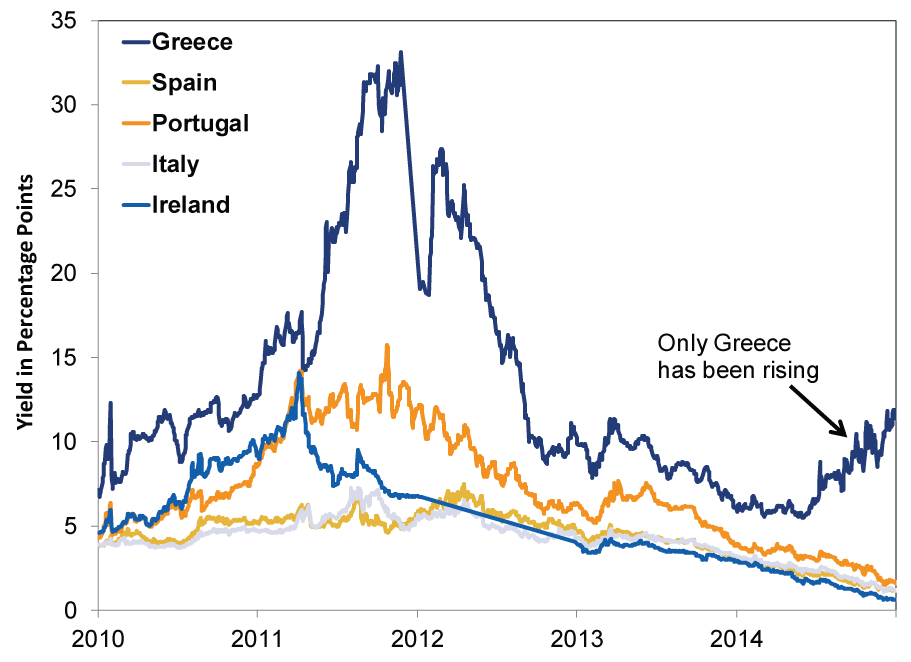

Bond yields show the same. Investors demand a heck of a premium to lend to Greece. Not so much for everyone else. The other peripherals blipped a bit when Syriza was elected in January, but they quickly settled, reflecting the fact Greece is Greece and its problems are its own. (Exhibit 2)

Exhibit 2: Eurozone Periphery 10-Year Bond Yields

Source: FactSet, as of 4/9/2015. From 4/9/2010 - 4/9/2015.

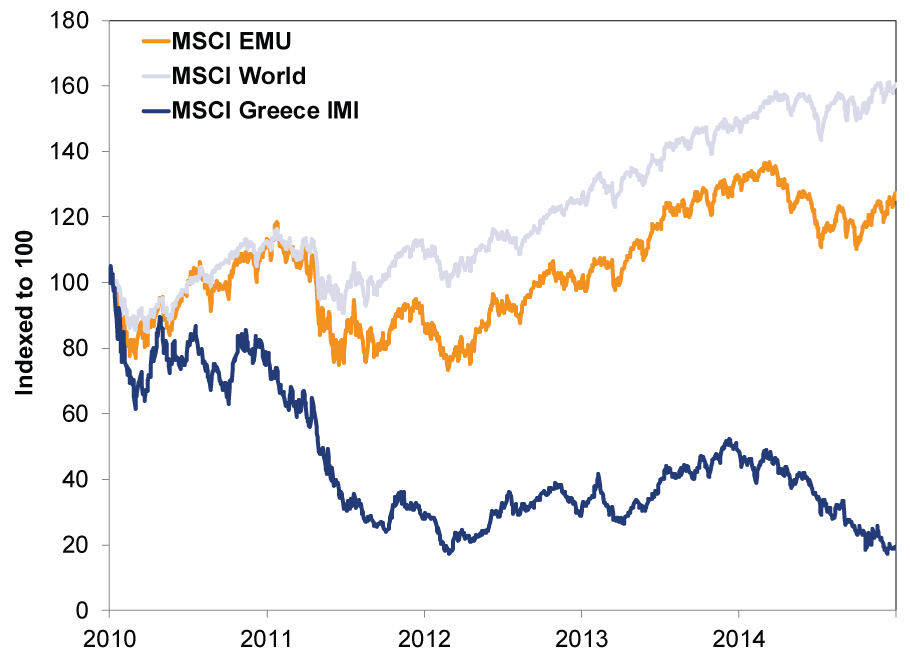

Stocks show it, too. World and eurozone stocks rose through Greece's tragedy and are rising still. Greek stocks suffered-the MSCI Greece IMI[iv] has lost nearly 81% since 4/9/2010. Markets there reflect every bit of the severe recession, political turmoil, fiscal trauma and banking crisis. But markets elsewhere have rationally risen, knowing Greece's increasing financial isolation within the eurozone, stronger banks, economic and fiscal improvements in other peripheral nations and robust institutional firewalls mitigate the impact outside Greece. (Exhibit 3)

Exhibit 3: Greek, Eurozone and World Stocks Since April 2010

Source: FactSet, as of 4/9/2015. MSCI European Economic and Monetary Union Total Return Index, MSCI World Total Return Index and MSCI Greece IMI Total Return Index, from 4/9/2010 - 4/9/2015.

So whether Greece compromises, defaults and leaves the euro, defaults and stays in the euro (as it did in 2012), or decides to form a Russo-Ottoman Empire with Putin and Turkey[v], markets have moved on. They aren't stressing. As loud and tense as the drama may get, we've seen this movie before-and it doesn't end badly for the bull.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] With love, we presume.

[ii]Over 96% of whom said "and by one or more we mean Greece, duh."

[iii] Grexit and the accidental Greek euro exit, the Grexident.

[iv] IMI stands for Investible Market Index, a gauge covering 99% of the market capitalization in a given country or region.

[v] Incredibly unlikely if you know the history here.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today