Personal Wealth Management / Market Analysis

Are Stocks Headed Into Foreign Territory?

What should investors make of non-US stocks' outperformance year-to-date?

So something rare for 2017 happened Tuesday: Stocks fell kinda bigly.[i] Rather predictably, the media flipped from fretting the "Trump rally's" sustainability to fretting its end-a common ritual since the election, perhaps exacerbated when daily returns were big. However, despite all the handwringing over the Trump rally, this reality may surprise investors: Markets outside America have led recently, which is hard to square with claims all the upside is tied to lofty expectations of US-specific political developments. Now, non-US stocks' year-to-date outperformance shouldn't be overstated, as investors haven't "missed out" on any leadership rotation yet. But this could be a sign of things to come later, especially as uncertainty falls outside America.

First, we would be remiss if we didn't (again) refute the continued assertions of a "Trump rally." Since Election Day, the S&P 500 is up 10.4%[ii]-a nice run over the past four-plus months. Headlines frequently questioned this rally's sustainability, arguing markets were rising on hopes of Trump pushing a Republican (read: business friendly) agenda, including deregulation and fiscal spending benefiting certain sectors. (This, of course, is an argument relying on markets' selectively viewing only these ideas and overlooking protectionist talk and weird border taxes, but we digress.)

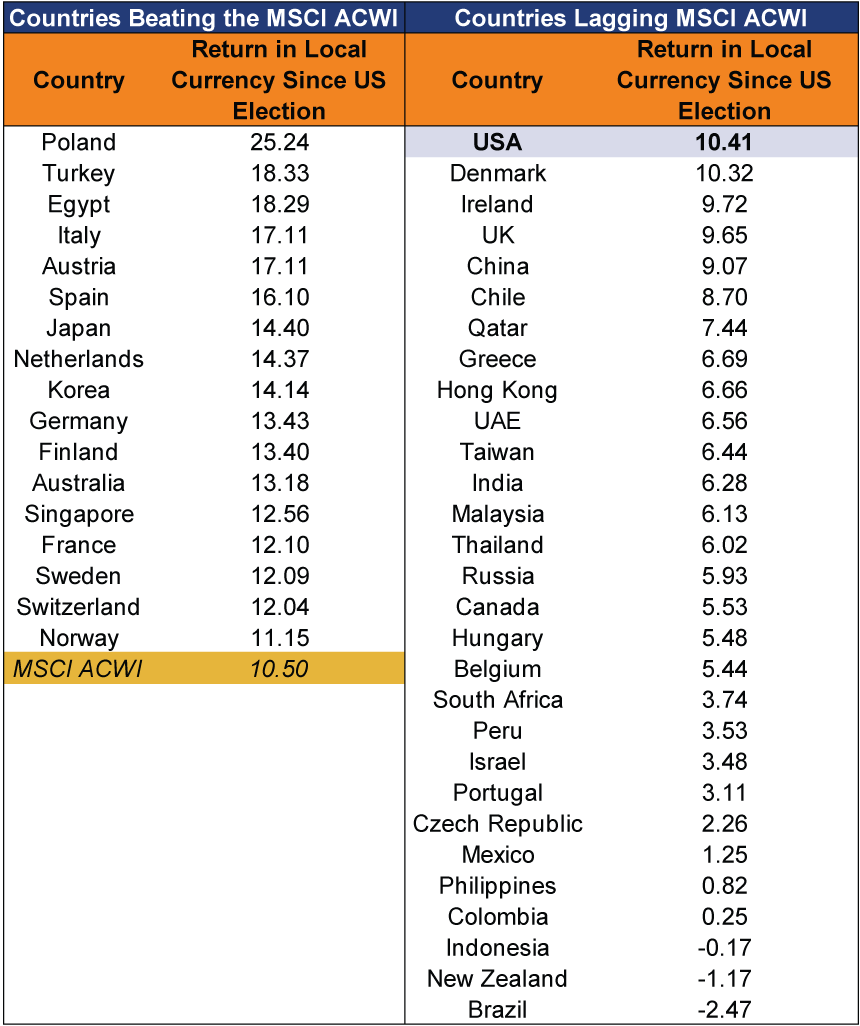

Yet in our view, the Trump rally is a myth. For one, presidential power over markets is vastly overrated. Bombastic rhetoric can add to day-to-day volatility, but presidents lack the power to bend the country to their whim.[iii] Second, if Trump truly were great for markets, US stocks should be near the top of the leaderboard after his election last November. Yet they aren't. After building a small lead as of Monday's market close, the US fell behind the MSCI ACWI[iv] after Tuesday's pullback (in USD). Moreover, since the presidential election, the US lags 17 other countries in the MSCI ACWI. See Exhibit 1, which denominates returns in local currencies to eliminate currency conversion skew. (For the same table in USD, click here. The US does a little better here, but only slightly-and still trails 14 other countries).

Exhibit 1: America's Post-Election Rally, Revisited

Source: FactSet, MSCI All-Country World Index local currency total returns by country, percent change, 11/8/2016 - 3/21/2017.

Investors have started noticing foreign markets are doing well, and some worry they have missed out,[v] especially after one outfit said world stocks are at their most expensive in almost two decades. However, we suggest not overstating this outperformance. Since 2017's start, the S&P 500 has returned 5.2% compared to the MSCI World ex. USA's 6.8%.[vi] A 160 basis point lead is nice, but not huge either (and one exacerbated by Tuesday's returns-as of Monday, that figure was 30 basis points).

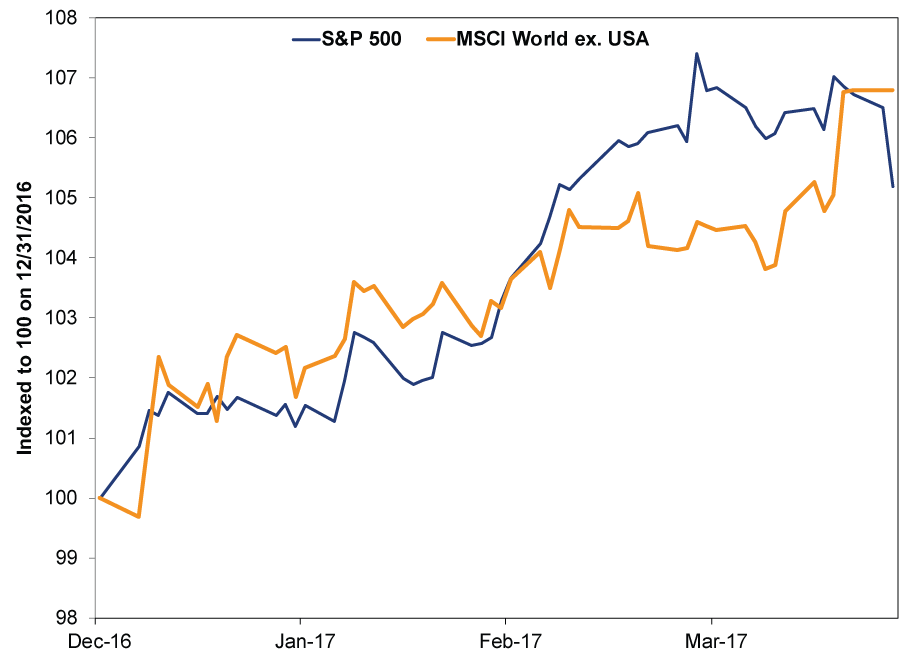

Some of these jitters over foreign stock performance may be tied to recency bias. US markets have beaten foreign for four straight calendar years. Over that stretch, investors can easily fall prey to the misperception that US stocks always lead-part of the common myth one style/country/category of stocks is innately superior. Thus, if higher expectations for the US are baked in, seeing foreign do better could be a jolt. Yet another category doing better isn't terribly surprising. Leadership rotates among countries and sectors, and all have their time in the sun and rain. Moreover, non-US's lead hasn't been steady throughout the year. (Exhibit 2)

Exhibit 2: US Stocks vs. Foreign Stocks Since Start of the Year

Source: FactSet, as of 3/20/2017. S&P 500 Total Return vs. MSCI World ex. USA, from 12/30/2016 - 3/20/2017.

As Exhibit 2 shows, foreign stocks only recently moved ahead. Before that, US and foreign exchanged the lead multiple times. A leadership shift, if that's what we're seeing now, often entails some waffling before taking hold, so don't be surprised if the US reclaims the lead for a bit.

That said, foreign markets have ample positive drivers, particularly Europe, which seems poised to benefit from falling political uncertainty. The UK and US experienced this phenomenon last year following the Brexit referendum and US presidential election. Political uncertainty weighed on sentiment before dissipating after the votes passed. 2017 is Western Europe's turn. The first domino already fell after the Dutch parliamentary elections last week. Polls at the start of year showed the anti-euro Party for Freedom (PVV) winning the most seats in Parliament, sparking chatter of anti-euro populism sweeping the Continent. However, their numbers suffered as the election approached, and after election day, the PVV did worse than expected, essentially tying for second place with several other centrist parties. The French presidential election is up next, and here too, the anti-euro populist wave seems more bark than bite. Centrist candidate Emmanuel Macron's poll figures are rising, and while much can change between now and the first round of voting in April, the Front National's Marine Le Pen's chances haven't meaningfully improved. Brexit negotiations will also start soon, further reducing uncertainty on that front. Sentiment across the Atlantic has lagged the US, but as various forms of uncertainty get resolved, investors should get relief and start unconsciously recognizing reality is far better than they feared-a bullish upside surprise.

While the "Trump rally" grabs headlines, it mischaracterizes reality: US stocks aren't the only game in town, and thus far in 2017, they aren't even the best. This is a prime example showing how globally diversified portfolios trump those heavily allocated to a single country-particularly for long-term, growth-oriented investors. Leadership among countries, sectors and styles constantly shifts without warning. Go global to mitigate the risk of being skewed too heavily to any one area.

[i] Note, there is nothing out of the ordinary about broader markets falling more than a percentage point in a day. Happens all the time during bull markets. It's just been a while.

[ii] Source: FactSet, as of 3/22/2017. S&P 500 Total Return index, from 11/8/2016 - 3/21/2017.

[iii] Even though the media acts otherwise.

[iv] The MSCI ACWI includes Emerging Markets, so it's an even broader gauge of the global stock market. The MSCI World-which we commonly refer to here on MarketMinder as a good global equity index-covers 23 developed economies.

[v] Or, as the kids would say, they are experiencing FOMO (fear of missing out).

[vi] Source: FactSet, as of 3/22/2017. S&P 500 Total Return and MSCI World ex. USA (net dividends, in USD). From 12/30/2016 - 3/21/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Expert Commentary This Week in Review | Consumer Confidence, Iran Developments, Bond Yields

2026-05-29

2026-05-29 -

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today