Personal Wealth Management / Market Analysis

COVID-19 Highlights the Perils of Relying on Dividends for Cash Flow

Companies’ responses to COVID-19 provide another investing reminder: Dividends aren’t assured.

Editors’ note: MarketMinder doesn’t make individual security recommendations; those mentioned here are part of a broader theme we wish to highlight.

With COVID-19 responses squelching sales, many companies are looking to build up cash reserves to help get through lean times. For some, that puts dividend payouts in the crosshairs. In our view, this is a timely, albeit tough, reminder for investors about the limitations of relying on dividend-paying stocks alone for cash flow.

As COVID-related restrictions disrupt normal business, companies are seeking myriad ways to stay afloat. One easy target: dividend payouts. Per one research outfit’s analysis, more US firms have suspended or canceled dividends this year than in the past 10 years combined. On April 30 Royal Dutch Shell, one of the UK’s most well-known dividend stocks, cut its payment for the first time since World War II.

Some observers warn reduced or suspended dividends signal businesses are in greater trouble than widely appreciated. While cutting a dividend clearly appears like acknowledgment of the stresses hitting a business, assuming it means much more seems like a stretch. During rough patches, dividends are often one of the first things to go when companies need cash in anticipation of weathering a downturn. Importantly, a suspension doesn’t necessarily mean firms are in trouble, either. For example, the ECB asked eurozone banks to suspend dividends and buybacks until at least October—a request with at least a few political overtones.

From an investing perspective, dividend cuts have spurred several misperceptions. One argument getting headlines, primarily in Europe: Dividends are the primary source of stocks’ returns. This is based largely on the fact the FTSE 100’s price returns were negative over the past five years, while its total returns were positive. If companies cut dividends now, some think it could take years for stocks to get back to 2019’s levels. Even on our shores, one popular notion is that dividends are a way for investors to at least get something during bear markets—and if those payouts dry up, where will return come from?

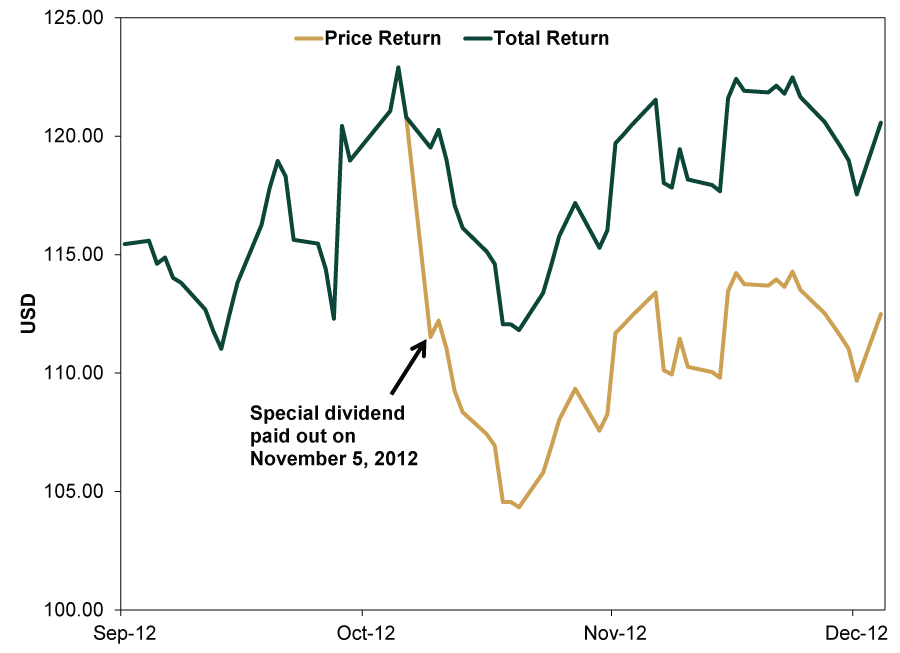

In our view, this misunderstands what dividends are. They aren’t bond interest. When a company pays a dividend, the stock price falls by the dividend cash amount. This can be difficult to see due to daily market volatility. But it is possible to show this. Consider a real-life example when a company paid out a large, one-time dividend. In 2012, Wynn Resorts paid a special $7.50 dividend. The company’s stock price fell rather steeply on the day it was paid. But as Exhibit 1 shows, its total return—price movement plus dividends paid—didn’t.

Exhibit 1: Wynn Resorts’ Special 2012 Dividend

Source: FactSet, as of 5/5/2020. Wynn Resorts, price vs. total return, 9/28/2012 – 12/31/2012.

This goes a long way toward explaining the large gap between the FTSE 100’s price and total returns. The UK market has always been heavy on dividend stocks due to its large exposure to banks and huge Energy firms—common dividend payers. If companies don’t make those payments, they don’t subtract from the stock price. This is why we focus on total return—price movement plus reinvested dividends. The latter is one component to consider, but it shouldn’t dictate how you invest.

Many investors like dividend-paying stocks since they use the payout for cash flow. But as recent suspensions and cancelations illustrate, dividends aren’t a “safe” source of cash. Relying on them can be precarious since they aren’t assured. Plus, dividend stocks are still stocks, which are subject to short-term volatility. In our view, if you have regular cash flow needs, it is best to identify the dollar amount and build a portfolio that keeps this in mind. Perhaps that includes some fixed income to help dampen volatility swings. Maybe it means you use a combination of interest, dividends and stock sales to meet cash flow needs. But it is unlikely to mean investing with an eye toward maximizing dividends.

Finally, focusing on dividend payers alone can mean missing out on large swaths of the global stock market. For example, Information Technology comprises nearly 20% of the MSCI World compared to just about 7% of the MSCI World High Dividend Yield index.[i] Prioritizing dividend stocks over others can mean a suboptimal portfolio mix, depending on market conditions.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History COVID-Panic’s Lockdown-Low Anniversary2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today