Personal Wealth Management / Market Analysis

ECB Says 25 Banks Were Undercapitalized 10 Months Ago

We dissect the ECB's stress test results so you don't have to.

The ECB released the long-awaited results of its asset quality review (AQR) and stress tests Sunday, confirming what some documents leaked last week: 25 banks failed, collectively undercapitalized by €24.6 billion. But 12 have already made up their shortfalls, leaving 13 banks on the naughty list. They have two weeks to tell authorities how they'll raise the remaining €9.5 billion and nine months to raise it, and all the healthy banks have one less axe hanging over their heads. The tests' completion relieves some of the eurozone's regulatory uncertainty-a positive-but it probably doesn't trigger a rapid rise in loan growth.

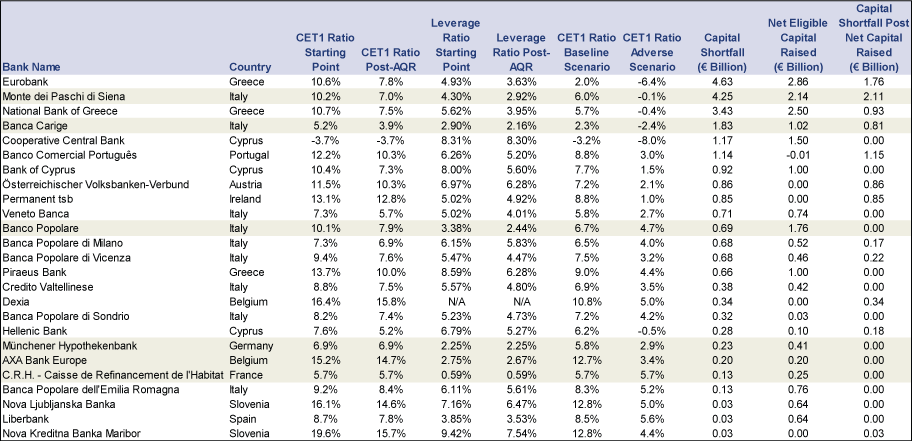

The tests themselves contained few surprises. Of the 25 failing banks, 17 were from the eurozone periphery-nine from Italy, three from Greece, three from Cyprus, and one apiece from Spain and Portugal. No supersized banks failed-most were small regional lenders. Italy's oldest (and third-largest) didn't make the cut-though it has been much maligned for some time now; nor did Portugal's largest (by market cap). Belgium's Dexia, already under government administration for failing in real life, failed in the make-believe future, too. One French and one German bank failed, but both have already made up their tiny shortfalls. Here's a chart:

Exhibit 1: The ECB's Naughty List

Source: European Central Bank, as of 10/26/2014. CET1 stands for Common Equity Tier 1, the benchmark capital ratio. Shaded lines indicate banks that didn't meet the minimum leverage ratio after the AQR.

The asset quality review was similarly benign. It identified €136 billion in previously unknown non-performing loans and ordered €48 billion in writedowns. Tiny, compared to tens of trillions in the entire eurozone banking system. The impact is even tinier considering €37 billion of those writedowns "did not generate a capital shortfall," according to the ECB's PowerPoint presentation. In other words, this isn't 2008.

So what next? We'll know in two weeks how failing banks will plug their holes, but some combination of stock offerings, contingent convertible bond offerings, asset sales and mergers wouldn't surprise. That list is most notable for what it doesn't include: The ECB isn't closing anyone down.[i] Past statements had intimated they might, which likely contributed to the heavy bank deleveraging over the past year. That they aren't pulling the plug on anyone yet is a welcome sign of flexibility.

However, this isn't an all-clear. As some observers have pointed out, 14 banks technically passed the European Banking Authority's companion stress test but finished in the nether region-above the 5.5% minimum Tier 1 capital ratio after the "adverse scenario," but below 7%, which will be the minimum once Basel III capital rules are phased in. That doesn't happen in the eurozone until 2018, but the UK was an early adopter, and two of the UK's big four banks landed in that capital purgatory. So it seems safe to assume regulators will be keen to learn what these banks' capital plans are.[ii] Which will probably make these banks a tad less eager to lend than they otherwise might be.

The ECB also didn't stress-test banks' leverage ratios-another forthcoming Basel III metric, which measures banks' Tier 1 capital relative to total (not risk-weighted) assets. Beginning January 1, 2018, eurozone banks must meet a 3% leverage ratio requirement, and the jury is out on whether banks will be penalized for falling below 3% during the "adverse scenario" of future stress tests. If so, this adds another wrinkle: The ECB did make banks report leverage ratios, and 17 fell below 3% after factoring in the AQR. Of these, 11 passed the stress test, which is bound to raise regulators' eyebrows.

Banks face other headwinds too, like the ECB's quasi-quantitative easing, which likely keeps yield curves flatter, making lending less profitable and constraining supply. The rise in non-performing loans also makes their balance sheets less flexible-the non-performers are deadweight that further shrink the supply of credit. Factor in Basel III implementation on the distant horizon, and banks have another incentive to be a bit stingy. So while banks do have clarity on whether their balance sheets comply with the ECB's new rules, they might not be able to do a ton with that clarity. The days of massive deleveraging might be over-a hugely welcome development-but we don't exactly expect the lending floodgates to open.

On the bright side, the tests do seem to have boosted confidence in a way the 2010 and 2011 stress tests didn't. Those exams were widely criticized for being too loose, especially after Belgium's Dexia and Cyprus's Laiki passed the tests only to fail spectacularly in real life. The criteria this time were tougher (though arbitrary), and the ECB seems to have struck the right balance-failing enough banks to give the tests credibility, but not enough to freak people out. They also published over one million datapoints on individual banks' finances, in an effort at being open-kimono and letting the market judge who's strong and who isn't. Most observers seem to accept that the banking system, broadly, is in ok shape. They aren't shouting from the rooftops that banks are surefire guaranteed to stay afloat the next time things go south-and nor should they, considering the "adverse scenario" probably doesn't match the next crisis[iii]-but the test and AQR seem to have eased concerns that a mass of toxic sludge lurks on eurozone bank balance sheets.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] At least, we guess, as long as they submit "credible" capital-raising plans. Whatever that means.

[ii] Though the kicker for the UK will be the Bank of England's stress tests, which wrap on December 16. BoE people have promised their test will be way tougher than the ECB's.

[iii] It also doesn't account for any decisions banks make between then and now, like how much to lend and to whom. Nor does it account for potential earnings between then and now, which could further boost capital buffers.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today