Personal Wealth Management / Market Analysis

Hidden Earnings at Home and Abroad

Don’t let the slowdown in headline earnings growth fool you...

While many wonder how tax cut proposals, Brexit chatter, Mifid, Trump tweets and Fed-head appointments might affect stocks, a key market driver remains healthy: earnings. As Q3 earnings season winds down, corporate earnings remain strong. But headlines focused on lower overall growth rates so far might have you thinking otherwise—with 98% of S&P 500 firms reporting as of 11/27, FactSet estimates Q3 earnings grew 6.3% y/y.[i] The slowdown from Q2’s 10.2% gets all the ink, but under the hood, we think reality is better than appreciated.

As in recent years, one industry skewed earnings—but with a twist. For the last couple years, the Energy sector distorted data. Dramatic oil price swings skewed sector earnings yuuugely. First, plunging oil depressed profits in 2015 – 2016. Then it flipped when oil prices and Energy firms’ earnings stabilized. Profits weren’t enormous, but growth rates flew thanks to meager comparison points from the prior year. But that impact is waning now. This time, the insurance industry is making a healthy reality harder to see. Hurricane-related losses drove a -63% y/y decline in earnings for the group.[ii] Omit insurance, and expected Q3 earnings growth improves to 9.0% y/y as of 11/27.[iii] But even with the distortions, earnings largely beat expectations. At Q3’s end, analysts expected earnings to grow 3.1% y/y.[iv] The current growth rate is more than double that, and it is due to sales, not cost-cuts. Revenues—up 5.8% y/y as of 11/27—are generally beating expectations.[v]

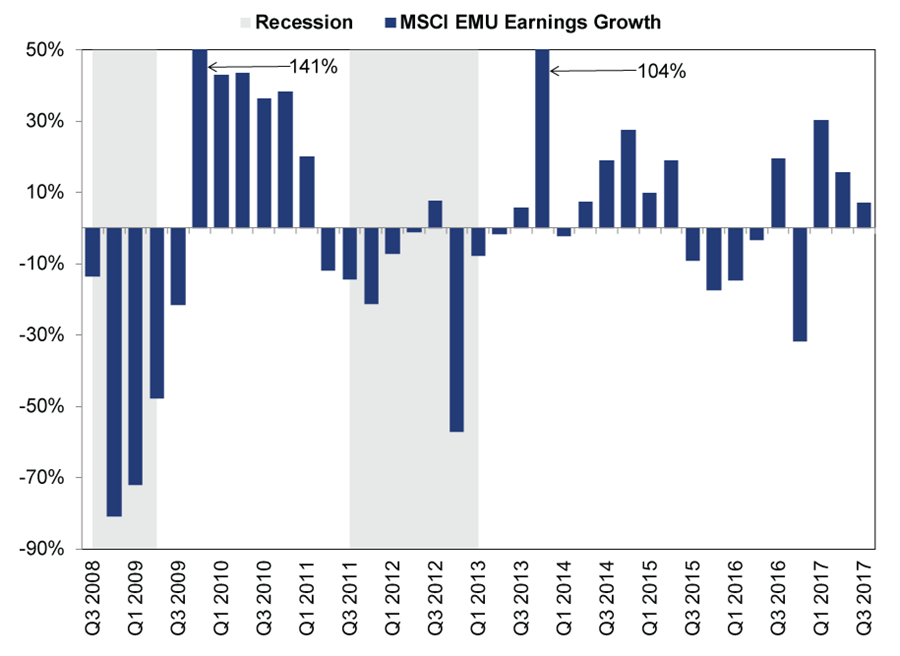

A similar story has unfolded in Europe, where earnings also slowed after rip-roaring growth in 2017’s first half. Hurricanes are to blame there, too. FactSet estimates a -57% y/y loss for the industry in Q3, depressing their estimate of headline earnings growth to 7.0% y/y.[vi] Exclude insurance, and estimated MSCI EMU earnings growth improves to 17.2% y/y.[vii] As in the US, one-off losses in one area are obscuring underlying strength. Most sectors—and even most other Financials—fared well. For example, bank earnings jumped 29.7% y/y.[viii] For the most part, earnings are strong and the outlook is optimistic.

The party may just be getting started in Europe. Economic fundamentals are generally improving. Q3 eurozone GDP increased at its fastest annualized rate since 2011. Yet sentiment there still lags the US. Back-to-back quarters of US GDP growth over 3% have boosted confidence and reduced the likelihood of upside surprise, particularly considering a couple dodgy components (falling imports and rising inventories) goosed the latest results. But investors have a different perspective on Europe. While the last US recession ended eight and a half years ago, only four years and change have passed since the eurozone emerged from its sovereign-debt-crisis-driven downturn. Many remain focused on widely discussed risks like euroskepticism, debt, a (perceived) lack of inflation and more. Lower expectations for eurozone data make positive surprise more likely than in America. That’s a backdrop we think eurozone stocks should love.

Exhibit 1: Year-Over-Year MSCI EMU Earnings Growth

Source: FactSet, as of 11/27/2017. Year-over-year percentage change MSCI EMU quarterly earnings, 9/30/2008 – 9/30/2017. Y-axis truncated due to extreme values post-recession.

Looking ahead, earnings should keep growing globally. Analysts expect Q4 S&P 500 earnings to grow 10.0% and revenues to increase 6.3% y/y as of 11/27.[ix] The Conference Board’s US Leading Economic Index (LEI) points to that growth continuing, a tailwind for Corporate America’s sales and profits. The same goes for the eurozone, where LEI is near 10-year highs and rising. Meanwhile, a steepening yield curve bodes well for future growth. The trend of accelerating loan growth and growing money supply should continue. Moreover, the ECB recently announced it will begin tapering its wrongheaded quantitative easing program, removing yet another headwind. All told, we expect the economic backdrop in the US and eurozone to continue supporting rising profits. As folks continue warming to this reality, we believe they should keep bidding up stocks.

[i] FactSet, as of 11/27/2017. Blended Q3 2017 S&P 500 earnings growth.

[ii] Ibid. Blended Q3 2017 earnings growth for the S&P 500 Insurance industry group.

[iii] Ibid. Blended Q3 2017 S&P 500 earnings growth excluding the Insurance industry group.

[iv] Ibid. Expected Q3 2017 S&P 500 earnings growth on 9/29/2017.

[v] Ibid. Blended Q3 2017 S&P 500 revenue growth.

[vi] Ibid. Blended Q3 2017 earnings growth for the MSCI EMU Index and Insurance industry group.

[vii] Ibid. Blended Q3 2017 MSCI EMU earnings growth excluding the Insurance industry group.

[viii] Ibid. Blended Q3 2017 earnings growth for the MSCI EMU Banks industry group.

[ix] Ibid. Expected Q4 S&P 500 earnings and revenue growth.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

-

Market Analysis Investors Are (Still) Fighting the Last War on Inflation2026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today