Personal Wealth Management / Market Analysis

How Emerging Markets Fit in a Global Portfolio

Emerging Markets have been hot this year-how should investors play the broad category?

With nearly three-fourths of 2017 in the books, global stocks are up nicely-hoorah! However, one segment of the market looks particularly tantalizing: Emerging Markets (EM). They are up nearly 30% year-to-date and are outpacing developed world markets-including the US-and enticing all comers. While we too are generally optimistic about EM presently, that doesn't mean we'd encourage investors to make a broad categorical play without delving deeper. Whether you're dabbling in EM as a global investor or have more exposure, it's important to consider country-specific nuances. Investors must differentiate among EM opportunities because they aren't a homogenous category, and specific sector drivers likely have a big influence on performance.

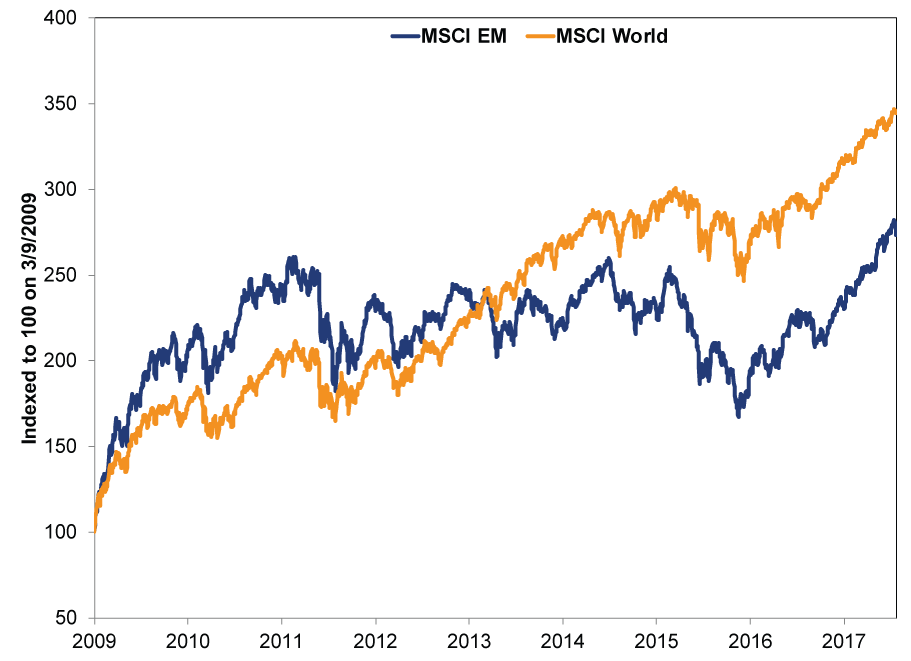

First off though, it's important to understand a few things. While EM nations tend to grow faster than the developed world, their stocks aren't inherently superior. Stocks are stocks, and everything has its day in the sun and the rain. EM stocks have had some great times, but they have lagged developed markets for most of this bull market. While the MSCI World has returned about 245% since March 9, 2009, the MSCI EM is up only about 174% since the same date.[i] (Exhibit 1)

Exhibit 1: MSCI Emerging Markets Vs. MSCI World Since March 2009

Source: FactSet, as of 9/28/2017. MSCI EM and MSCI World Index returns with net dividends, from 3/9/2009 - 9/27/2017. Indexed to 100 on 3/9/2009.

However, after enduring their own bear market and a long flat stretch, Emerging Markets are roaring. They bottomed on January 21, 2016-a couple weeks before the most recent global stock market correction ended-and have been climbing ever since (notwithstanding a couple short pullbacks). The MSCI EM beat the developed nation-only MSCI World last year (11.2% vs. 7.5%), and that streak has continued into 2017: Year-to-date, MSCI EM is up 27.4%, almost doubling the MSCI World's 15.6%.[ii]

While some EM exposure may make sense for a globally minded investor, beware treating EM as a broad, uniform category. EM countries vary in both their sector concentrations and economic and political development. For example, Korean markets are heavily tilted toward Tech. In the MSCI Korea, Information Technology comprises nearly 50% of market cap-much higher than the MSCI Emerging Markets index's 28%.[iii] However, MSCI Korea's 10% Consumer Discretionary market cap mirrors the MSCI Emerging Markets' slice-representative of the growing consumer classes common in more developed markets.[iv] Korea also exhibits some political qualities of a developed market, like respect for rule of law. President Park Geun-hye was impeached and removed from office earlier this year, and while the story seemed straight out of a Korean soap opera, the legislature and judiciary were transparent and functioned as designed. The people then selected Park's successor, Moon Jae-in, via free election. Korea lags in some respects-MSCI cites lingering capital controls when declining to add it to developed-market indexes-but overall, it has a lot in common with developed markets. The OECD even considers it developed.

Compare that to Pakistan, which just joined the MSCI Emerging Markets Index this year. The MSCI Pakistan consists of just six constituents. Three are Financials, two are Materials companies and one is in Energy: a sign the country has a ways to go to develop its private sector. There is also a lot more political uncertainty. The Pakistani Supreme Court surprisingly removed Prime Minister Nawaz Sharif from office for corruption in July-the third time he has been removed as PM. Corruption is more common in EM, and this scandal set off a spate of political uncertainty. An interim PM is serving until next year's general election, and potential candidates are already positioning themselves for power, ranging from the ousted Sharif's younger brother to a firebrand cleric.

While these two examples may be on the opposite side of the spectrum, investors can apply this exercise to other EM too. Taiwan? Its equity markets are similar to Korea's, and political corruption isn't as problematic as other EM.[v] South Africa's local markets skew heavily toward Consumer Discretionary and Financials, but its political situation is much more tumultuous. Prime Minister Jacob Zuma is embroiled in a corruption scandal and has pursued face-saving moves (e.g., changing a mining charter) to win popular support and maintain his clout. Markets have probably priced in the persistent uncertainty, but it isn't likely to abate any time soon.

Because EM nations diverge so much on an individual basis, investors should keep each country's domestic capital markets in mind when considering investment opportunities. If you're a global investor looking to add some EM exposure, don't dwell on GDP growth rates-which are backward-looking and not indicative of stock returns. Instead, see EM as a chance to gain exposure to global sector themes you expect to do well in the near-term future. If you are bullish toward Technology, it makes sense to look at opportunities in Taiwan and China. Maybe Korea, too, though regulatory risk seems somewhat higher there at the moment. These three countries combined account for about 95% of total market cap for the MSCI Emerging Markets Technology index.[vi] Similarly, Russia and Brazil are appropriate places to look if you think global Energy will do well looking ahead. Investing in Mexico means you're probably adding to your portfolio's Consumer Staples, Materials or Telecom allocation-the country's three biggest sectors. While we caution against loading up on any one sector or geography-don't forget that no matter how sure you are about a category, you could always be wrong-we believe taking strategic EM positions based on global sector themes can add value for investors.

Looking ahead, we believe the market cycle is around the bull's final third-a time when big, quality growth stocks tend to do best. Globally, the Tech sector fits the bill, and EM has some of the biggest, highest-quality Tech names. In our view, looking at EM opportunities in this space is another way to add non-US Tech exposure, which we believe should do well for the foreseeable future.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today