Personal Wealth Management / Economics

Quick Hit: Reopening Drove Up April’s Prices

Under the hood, April’s US Consumer Price Index was far cooler than the headline read.

Almost a week after the report hit, April’s US Consumer Price Index (CPI) reading is still garnering tons of attention—and stoking lots of fear in the process. We have spilled many pixels on this already, arguably too many, and we don’t intend to belabor the point here. However, one aspect that we think is going underreported is just how much skew reopening drove. Here is a quick look under the hood that reveals this quite clearly.

First, to be clear, we aren’t referring to the 4.2% y/y inflation rate.[i] That, as we noted recently, was a garbage number—hopelessly skewed by the depressed April 2020 reading that serves as the denominator. Rather, we are referring to the 0.8% m/m rise—the largest since June 2009.[ii] Actually, without rounding, that figure was 0.77%.

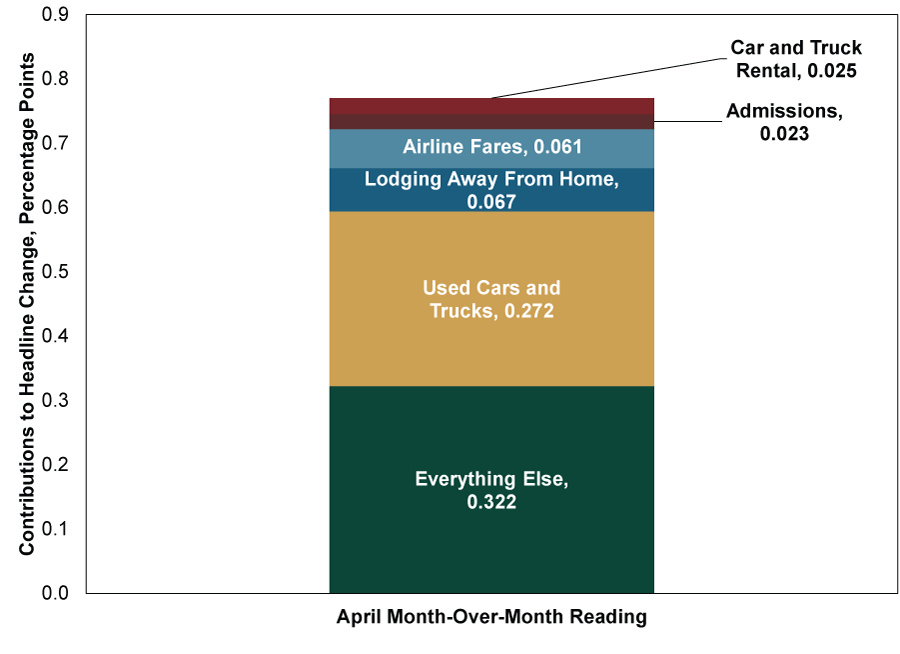

Underneath that headline number, there are a couple hundred or so subcategories. Five of them—used cars, car and truck rental, airline fares, admissions (to the movies and sports events) and lodging away from home (hotels/motels)—accounted for 0.448 percentage point of April’s monthly increase. These five categories, which account for 5.061% of the overall CPI basket, accounted for more than half the monthly gain. Exhibit 1 shows you this visually, if you are that kind of learner.

Exhibit 1: Reopening Drives CPI Higher

Source: US Bureau of Labor Statistics, as of 5/14/2021.

For four of the five, the connection to reopening is quite obvious. The one exception is used car and truck prices, which rose 10.0% m/m and added 0.272 percentage point to the headline rise, the biggest contributing subcategory by far. Some pundits, like Matthew Klein at Barron’s and Paul Krugman in The New York Times, came up with plausible-seeming explanations. The former tied it mostly to car rental companies liquidating their fleets a year ago—and scrambling to rebuild them now. The latter mostly pinned it on semiconductor shortages impacting new vehicle production. Whichever of these are right—or even if both are wrong and some other cause or causes explains the jump—we strongly doubt used car prices will continue rising at April’s white-hot rate.

The same holds for the more obviously reopening-related areas. It all adds up to a report that actually illustrates the likely fleeting nature of recently rising inflation measures, despite all the hullabaloo it drove. To us, that suggests investors reacting to fearful headlines could easily be committing an error.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Quick Hit: Durably Broad-Based Growth2026-07-29

-

Market Analysis On the Chop in the Oil Market2026-07-29

-

Politics Takaichi Raises Japan’s Wall of Worry2026-07-27

-

In The News Why Kevin Warsh should think twice about hiking interest rates — even as anxiety over the Iran war grows2026-07-27

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today