Personal Wealth Management / Market Analysis

Sorry, the Fed Isn’t That Powerful

Widening the Fed’s mandate probably widens the potential for error, in our view.

In recent years, it has become ever-more popular to presume that the Fed can use its ability to create or destroy bank reserves and exert influence over short and long rates to exert quasi-magical influence over just about anything, leading to calls among politicians and pundits to widen its mandate. Many attribute the 2009 – 2020 bull market and the current one to its “stimulus” moves like quantitative easing. Many others attribute the labor markets’ pre-coronavirus health to it—one end of its “dual mandate” to balance labor market health and inflation. Still others blame the Fed for low wage growth over the past few decades, claiming it focused too much on the inflation end of that mandate. All the contradictory claims have now seemingly jumped the shark and veer off into presuming the all-powerful Fed should get additional responsibilities—some push it to act as lender of last resort for Main Street, municipalities and just about everything else. Many further presume the Fed should use monetary policy to target social outcomes or other political causes. But whatever you think of these ideas, the trouble is they presume clout, competence and efficacy the Fed hasn’t historically demonstrated. Those who want to widen the Fed’s mandate would do well to remember: Any time you want the Fed to do more, they have more to mess up.

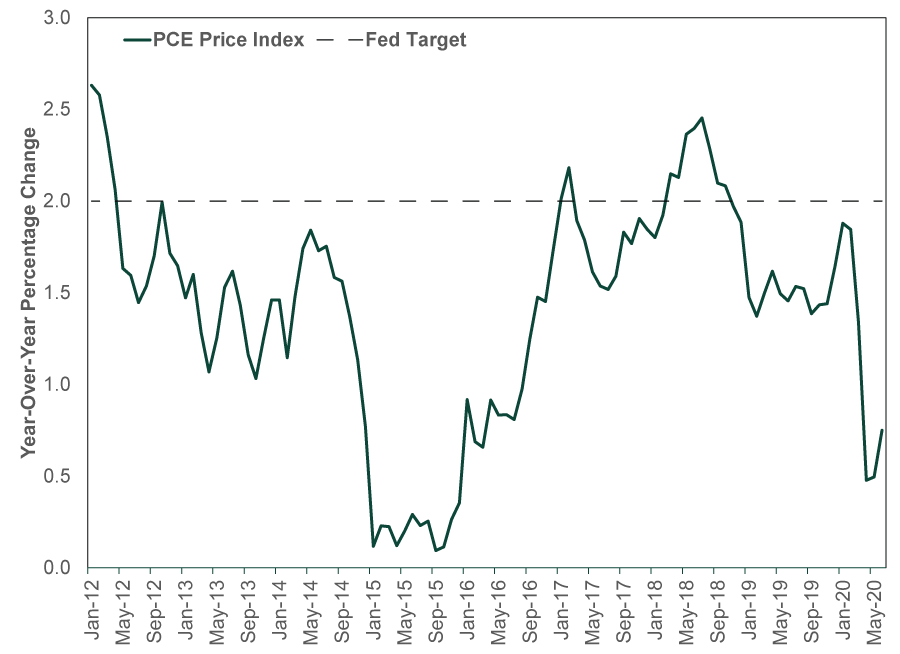

The Fed’s current mandate, as summed up by its Chicago branch, is to “achieve both stable prices and maximum sustainable employment.” Since January 2012, the Fed has interpreted “stable prices” as a 2% year-over-year inflation rate (based on the Personal Consumption Expenditures Price Index, not the Consumer Price Index and not the “core” version of either gauge that excludes food and fuel). In this span of time, the actual PCE inflation rate has been within 0.2 percentage point above or below the target in 19 months … out of 102.[i] For the first several years, as inflation drifted further below the target, everyone feared deflation was setting in.

Exhibit 1: Missing the Target

Source: Federal Reserve Bank of St. Louis, as of 8/5/2020. PCE Price Index, January 2012 – June 2020.

The grand irony is that this stretch of severe disinflation occurred as the Fed pursued a policy, known as quantitative easing (QE), whose stated goal was to boost prices. By purchasing long-term bonds, the Fed reduced long-term interest rates, which it believed would spur demand for credit and get more money moving through the economy—a recipe for faster inflation. As Nobel laureate Milton Friedman summed up, inflation is too much money chasing too few goods. Basically, the Fed thought QE would enable more money to do more chasing.

But it actually did the opposite, because it flattened the yield curve—the spread between long-term and short-term interest rates shrank. This wasn’t good news, because banks pay short-term interest rates for funding, charge long-term interest rates for lending, and profit off the spread between the two. When the spread is big, potential profits are big, and banks have ample incentive to lend broadly. With more potential reward, they can take more risk and lend to a much wider swath of borrowers. When the spread is slim, banks have much less reward to take risk and generally lend to only the most creditworthy. So even as demand for loans rises, supply diminishes, and lending grows more slowly. Loan growth was overall sluggish throughout QE’s lifespan—and negative for a long stretch of it—weighing on money supply growth and inflation.

Going further back, the Fed has a long, long history of keeping its foot on the gas pedal too long and then jamming the breaks too hard once inflation bubbles up. This herky-jerky monetary policy contributed to many of the economic ups and downs of the 20th century, and it is why Friedman quipped that replacing the Fed with a computer that ensured a steady, predictable money supply increase over time would yield much better results. We doubt the late, great economist’s viewpoint would be different today, considering the Fed hasn’t acquitted itself terribly well since his death. It could even be sowing the seeds of its next great foible today, if it doesn’t appropriately rein in this year’s massive money supply increase before velocity picks up materially from its currently record-low rate. (Not that hot inflation is at all likely in the near future, but Fed error on this front is a risk we watch for.)

So, we ask: If the Fed isn’t terribly good at fulfilling a key plank of its core mandate, why should we think giving it more responsibility is so sensible? Why should we expect it to suddenly avoid any and all unintended consequences and stop sleepwalking into risks and errors? If it can’t meet its inflation target, why would it be able to meet other specific targets, some of which are light years removed from monetary policy?

Most central banks worldwide base policy exclusively on inflation targets. That doesn’t even ensure they get it right—see Japan and the eurozone, which have missed their 2% target rates by an even wider margin than the Fed. That the Fed has to balance this with employment only complicates their jobs. Doubly so considering tying employment, wages and inflation was debunked in academic circles before the Humphrey Hawkins Act even became law. We can’t see how adding more complexity will help generate better policy.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today