Personal Wealth Management / Market Analysis

S&P’s Shifting Opinion

Standard and Poor’s (S&P) was busy Friday, downgrading nine eurozone nations—including previously AAA France and Austria. But these actions seem far less material than many presume.

It appears Standard and Poor’s has fixed their sovereign-downgrade button.

After November’s erroneous French downgrade notice, which the ratings agency attributed to a technical error, on Friday France’s finance minister said his office received a memo stating S&P had downgraded France from AAA to AA+. Hours later, S&P confirmed France is among nine eurozone sovereigns downgraded: Austria will be similarly lowered from AAA to AA+; Italy, Portugal, Spain, Cyprus, Malta, Slovakia and Slovenia were also downgraded. The other eight eurozone nations will keep their ratings—including AAA-rated Germany and the Netherlands. However, most of the media attention was on France.

S&P’s rationale is mainly eurozone politics. In its view, the bloc’s leaders may not have acted sufficiently to quell peripheral debt issues’ “systemic” problems. (Which begs the question, if the issues cited are systemic, why weren’t all 17 downgraded?) Whatever your opinion of S&P’s rationale (in our view, politicians doing more can be quite undesirable), it’s important to note the lack of actual, material impact ratings changes have historically had on nations’ finances.

As we often write, markets tend to move most on surprises—reflecting anticipated events before they actually occur. And many in the media have had a hyper-focus on French and eurozone ratings for months (see here, here or here for examples), particularly since S&P’s blanket everything-eurozone’s-on-negative-credit-watch warning issued December 5. The fact so many expected a downgrade—even blogged in major media publications about non-downgrades—makes it seem the surprise power to materially affect markets for long likely isn’t there. And apparently agreeing, French 10-year bond yields rose to 3.06% Friday—a mere 0.03% higher than they started the day.

Yet many still fear a lower rating will drive French yields higher, increasing its debt-service cost. And maybe so, but let’s not forget: S&P’s US downgrade last August immediately preceded a relatively consistent decline in US 10-year interest rates. And as we showed in the graphs here, that’s the norm historically when AAA-rated sovereigns are downgraded. So should French bonds respond the way precedent suggests, perhaps French President Nicolas Sarkozy should send S&P a hearty, ”Merci beaucoup.”

Others fret the EFSF, which issues its own debt, could be negatively impacted since the fund is mostly backed by Germany and now lower-rated France. It too could potentially lose its AAA. And sure, its possible EFSF rates rise. But Friday, EFSF 10-year rates fell by 0.04% to 3.108%. That rate is lower than the 3.659% the day S&P put most of the eurozone on negative credit watch. And amid French downgrade chatter, the EFSF smoothly auctioned 3-year debt just last week at 1.77%. And as to fears about potential banking system blowback, the ECB moved earlier in an effort to address this.

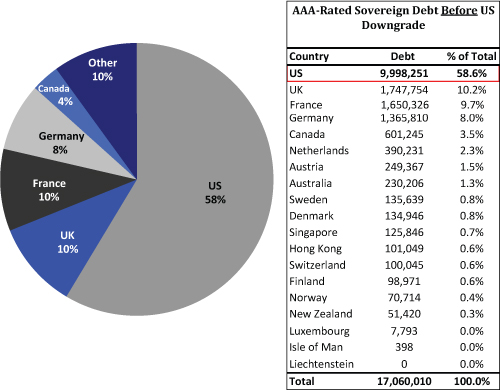

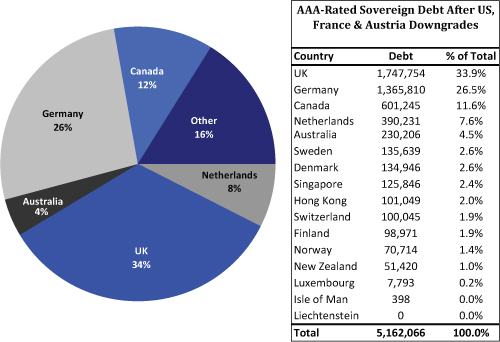

For even those investors who choose to heed credit raters’ opinions and seek only the highest-rated debt, the supply of AAA-rated sovereign debt has fallen almost 70% in the last six months. Investor demand could easily exceed this, thus likely making AA+ the new AAA for some. Exhibit 1 shows the global AAA-rated sovereign debt as of July 2011. Exhibit 2 shows the current.

Exhibit 1: Global Distribution of AAA-Rated Sovereign Debt Securities By Issuing Country, as of July 2011

Sources: Thomson Reuters, Bloomberg Finance, L.P. Debt figures in millions of USD; ratings from Standard and Poor's.

Exhibit 2: Current Global Distribution of AAA-Rated Sovereign Debt Securities

Sources: Thomson Reuters, Bloomberg Finance, L.P. Debt figures in millions of USD; ratings from Standard and Poor's.

Fellow credit raters Fitch and Moody’s have each recently said France’s rating isn’t on their chopping blocks in the immediate future. But should that change, which isn’t impossible considering the raters’ long history of herd-think, recall their ratings are merely opinions. And for all Friday’s handwringing over S&P’s, a multitude of evidence suggests it’s an opinion that hasn’t much fussed bond markets historically.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Volatility How Investors Should Think About the Ceasefire2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today