Personal Wealth Management / Market Analysis

Think Global, Invest Global

Despite recent US outperformance, a global strategy still provides many benefits.

Photo by Leonello Calvetti/Getty Images

Monday, the S&P 500 price index notched its first new high since May 21, 2015, capping a challenging streak that tried even the steeliest investors. While global markets have rallied sharply, they haven't yet reached new highs, likely reminding some of US stocks' leadership in this bull market-and perhaps spurring some to wonder if a global approach is worth it. But recent US outperformance doesn't negate the big benefits a global approach provides. Jumping the global ship now in favor of the US doesn't make much sense.

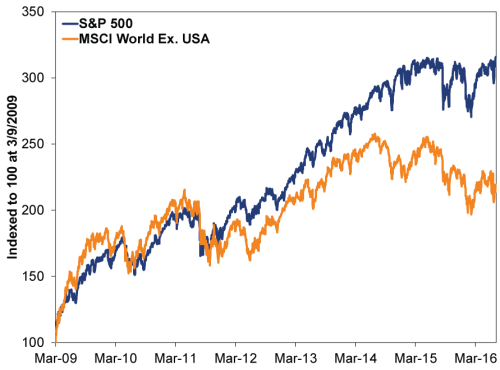

In 2009, foreign stocks outperformed domestic-and remained in the lead through mid-2011. Since then, though, US stocks have beaten foreign by a sizable margin, a gap that has led many global investors to question their foreign holdings.

Exhibit 1: US Versus Foreign, 2009 - 2016

Source: Global Financial Data and FactSet, as of 7/11/2016. S&P 500 Total Return and MSCI World ex.US monthly returns 12/31/2009 - 6/30/2016.

But as that 2011 shift illustrates, leadership often rotates. During the 2002-2007 bull market, US-centric investors may have been pleased to see the S&P 500 rise 121%, but investors who had a global approach fared much better, as the MSCI World Index climbed 158%-driven by non-US developed-world stocks' 213% rise.[i]

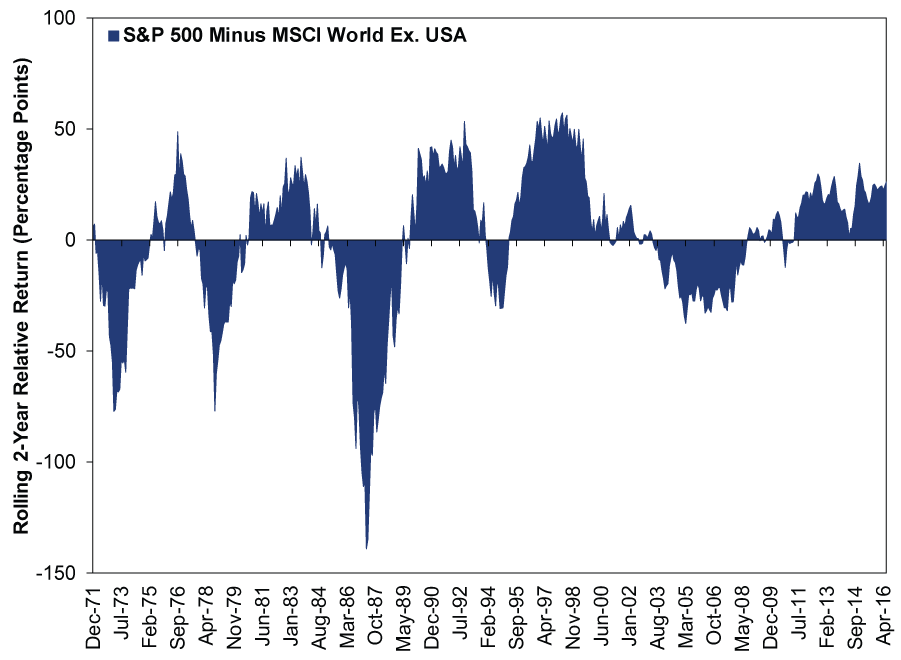

Exhibit 2: US and Foreign Outperformance Rotates

Source: FactSet and Global Financial Data, Inc., as of 7/11/2016. Rolling 2-year returns for the MSCI World Ex. USA (with net dividends) and S&P 500 (total return) indexes, monthly, 12/31/1971 - 6/30/2016.

Just as foreign stocks' outperformance from 2002 - 2007 didn't mean they were perma-superior, US outperformance in this bull doesn't mean domestic stocks are inherently best. No one category is permanently better than any other. All well-constructed, broad benchmarks tend to yield very similar returns over the long run, and a blended strategy of both US and foreign provides benefits to investors.

A global portfolio is by nature more diversified and thus less volatile. At times either the US or foreign performs especially well while the other trails, and having a mix of both provides a smoother ride over time than investing solely in one area. Diversification also reduces the risk of being overly exposed to political and economic risks or sentiment overhang in any one area. For Brits, a global portfolio is a hedge against Brexit uncertainty. For eurozone investors, a global portfolio hedges against bank jitters and negative rate fears. And for Americans, a global portfolio is the answer to any of today's common (largely political) fears.

Being confined to one category also closes off opportunities. A foreign-only portfolio would not have benefited from booming US Tech stocks in the 1990s, and a US-only strategy would have missed out on foreign stocks' outperformance in the 2000s. Japanese stocks far outpaced the US during the 1980s. During the 1970s when oil shocks, high inflation and a brutal bear market caused middling US returns, foreign stocks fared much better. The US may be the big boy on the block, accounting for over half of global developed markets, but sometimes great opportunities knock in other parts of the world too.

Some suggest investing in multinational US companies that derive a lot of sales in other countries provides global exposure, eliminating the need to invest in foreign stocks. But this isn't quite right. US multinationals correlate much closer with other US stocks than foreign-you intuitively know this from the preceding charts and data. After all, the S&P 500 is market cap weighted, so the very biggest-typically US multinational firms-influence performance most. Yet differences persist between foreign and US. Why? Factors other than where a company generates its revenue-such as taxes and regulations, the political landscape, central bank policies and overall sentiment towards the region-often impact returns more.

Why not invest globally, but go all in on the region that's leading, then switch to the other category when it leads? If it were possible to accurately forecast turning points consistently over time, then yes, this would be a winning tactic. Most investors don't like seeing underperforming stocks in their portfolio. It's natural to want only what's going up the most. Yet while we do believe region and country leadership can be forecast, timing it is imprecise and you must always remember you could be wrong. Then, too, many investors fall prey to recency bias, chasing after the category that just did the best. If you load up on a hot category, thinking it will continue to lead, your returns will suffer if that theory proves wrong. Repeating this error-by, for example, piling into US stocks in 1999 and then loading up on foreign in 2007-may risk not just underperforming, but not achieving your long-term financial goals. Staying global, and retaining holdings even in areas you don't think have as bright an outlook is exercising wise humility.

Now, many claim currency movements mitigate or negate global investing's benefits as a strong home currency reduces the returns of foreign stocks. That has been true in the US since 2014. But this is myopic. Just as no country's stock market permanently outperforms, no currency does either. There will be times when the dollar is strong, as it has been lately, but there will also be times when it's weak, boosting foreign returns. Throughout the 2002-2007 bull market, foreign stocks' 213% rise in US dollars was 138% in their native currencies. Over time, currency movements-and their impact on foreign returns-will balance out. This doesn't mean, though, that foreign will always underperform when the dollar is strong. Currency movements aren't the only factor influencing foreign stocks and, as a result, there have been times when foreign outperformed alongside a strong dollar. In the 1980s, the dollar was strong and foreign stocks outperformed.

Diversification reduces risk, but this also means not everything in your portfolio will be doing well at the same time. You'll probably always have a portion of your portfolio you hate. It's hard to appreciate sometimes, but that's a good thing, not bad. While right now that nagging portion may be foreign stocks, we believe the argument to invest globally is compelling.

[i] Source: FactSet, as of 7/12/2016. S&P 500 total return, MSCI World Index with net dividends and MSCI World Ex. USA Index with net dividends, 10/9/2002 - 10/9/2007.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Oil Prices, UK Politics, Tech Stocks

2026-06-26

2026-06-26 -

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today