Personal Wealth Management /

Too Much Twitter Over IPOs?

Is the recent spate of IPOs a sign of bubble trouble?

The infamous Pets.com sock puppet—a reminder of the circa-2000 IPO excesses. Photo by Scott Gries/Getty Images Entertainment.

These days, the financial press sure seems atwitter over IPOs. A certain high-profile social media company is set to debut, and some gush over a host of recent offerings—even those whose revenues aren’t quite up to snuff. If that sets off your bubble radar though, fear not—today’s IPO landscape is far different from 2000’s.

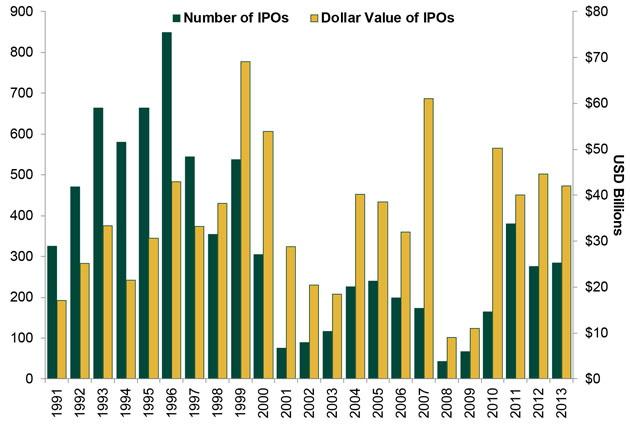

For one, the IPO “comeback” is a bit overstated. The sheer number of offerings is rising but nowhere near the lofty heights of the late 1990s. In dollar terms, issuances are about on par with the mid 1990s, but the rise comes after years of rather depressed levels. (Exhibit 1)

Exhibit 1: US IPO Activity

Source: Bloomberg, as of 10/28/2013. 2013 figures are through 9/30/2013.

Overall, new offerings have been quite muted since the late 1990s. Partly because sentiment was guarded after the Tech bubble burst, but likely also due to the regulatory headaches from Sarbanes-Oxley. The accounting burdens that come with going public are much heavier today than 15 years ago, and many start-ups have opted to seek buyouts instead of IPOs. Others have likely chosen to stay private longer than they otherwise would have. For example, absent SarbOx, would Facebook have stayed private as long as it did? The rise in IPOs of recent years could just be an unleashing of pent-up activity as firms and underwriters digested the new regulatory reality.

The unleashing of this pent-up activity seems partly related to firms with less than $1 billion taking advantage of April 2012’s Jumpstart Our Business Startups Act (the JOBS Act). This act exempts such firms, called Emerging Growth Companies (EGCs), from some of SarbOx’s most onerous requirements. One report from law firm Latham & Watkins suggested EGCs accounted for nearly three quarters of IPO activity in the JOBS Act’s first year of life.

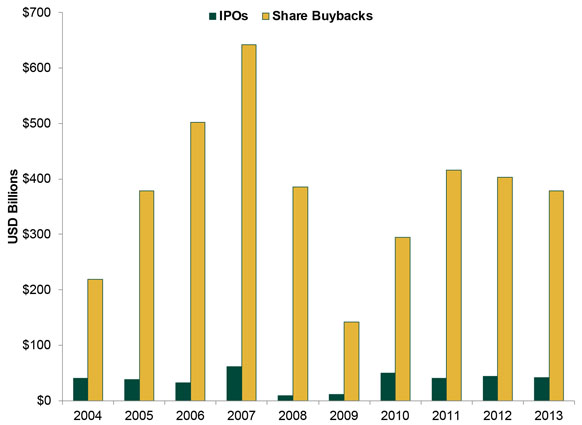

That said, whatever the reason for recent offerings, if they lead to a material increase in stock supply without a corresponding increase in demand, it could be a negative. However, this isn’t the case. Stock supply is falling. As shown in Exhibit 2, S&P 500 share buybacks have dwarfed IPOs. In Q3 alone, buybacks exceeded total offerings since 2011. They also exceeded the $85.9 billion in new 2013 offerings globally as of 9/26. Shrinking stock supply and rising demand is fundamentally bullish.

Exhibit 2: S&P 500 Share Buybacks

Source: Thomson Reuters, Bloomberg, as of 10/28/2013. 2013 figures are through 9/30/2013.

Some say the real concern isn’t from rising stock supply, but sentiment—that rising demand for firms with shaky finances suggests investors are getting euphoric. There certainly does seem to be a disconnect between sentiment and reality, but not in the way most people think. Unlike in 2000, for every article proclaiming profits don’t matter, many more point out potentially weaker fundamentals. The vast majority of investors don’t appear to believe “Likes” are the new profits. On balance, there appears to be a healthy amount of skepticism. And IPOs are the only arena where one could really accuse headlines of being sunny. Most other news—even good news—is cast in a rather dour light. Irrational exuberance seems a long way off. In fact, bubble fears are basically self-deflating. In a true bubble, media mostly cheerleads and investors commonly argue away deteriorating fundamentals. Not only are folks not commonly building such bullish arguments, fundamentals are actually improving.

Plus, valuations aren’t going through the roof—according to a recent Wall Street Journal piece, recent tech IPOs are trading at 5.6 times sales, compared with 26.5 times sales in 1999. Overall and on average, revenues are stronger today (profits, however, are another story). And while some Tech IPOs (ahem, Twitter) may have yet to turn a profit, IPOs from other sectors outweigh Tech issuance, and many of these firms are higher-quality. Would one categorize, for example, Energy firms selling fracking-related technology, the same as social media?

And not all IPOs are technically new companies! Private equity firms have taken a number of corporations private in recent years, and some of these have started trickling back to the market. For example, Blackstone took the Hilton hotel group private in October 2007 and filed to take it public again last month.

In our view, the IPO fascination is more telling about another sentiment gap: investors’ too-dour view of stocks overall. Some say folks are flocking to IPOs because they’re the only firms with strong growth potential. Never mind that the S&P 500—well-established firms—is continually clocking new highs. With capex, sales and profits rising—and the global economy reaccelerating—firms have plenty of fuel for future growth.

Sure earnings have slowed a bit lately—with nearly half of S&P 500 firms reporting as of October 25, aggregate Q3 share-weighted earnings growth was 2.3%—but this is normal as bull markets progress and year-over-year comps become more difficult to beat and firms reach the limits of earlier productivity gains. As bull markets progress, firms usually have to raise production to keep pace with demand, bumping up costs. Then, revenue becomes a more significant driver of earnings growth. Revenues have slowed in recent quarters, but many firms reported this was tied to the eurozone recession and some slower-growing Emerging Markets. Now, with growth picking up globally—the eurozone out of recession, Emerging Markets (most notably China and Korea) growing faster, Japan still kicking (for now) and the US poised for faster growth once quantitative easing (QE) ends, the stage seems set for nice revenue growth looking forward. In other words, there should be plenty to surprise folks who think IPOs provide the only chance for strong returns.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Around the World in Tax Policy Talk2026-05-15

-

Expert Commentary This Week in Review | US Inflation, US-China Visit, Fed Chair Confirmation

2026-05-15

2026-05-15 -

Market Analysis Reader Mailbag: May 20262026-05-14

-

Politics The UK’s Political Ructions Hide a Better-Than-Feared Economy2026-05-14

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today