Personal Wealth Management / Market Analysis

Understanding MLPs

Though pitched as stable, high-yielding investments, master limited partnerships face tough sledding as oil tumbles.

Oil took it on the chin again Monday, hitting seven-year lows as it became increasingly evident the supply glut won't abate any time soon. The latest confirmation came from Opec, which didn't slash production quotas at an apparently acrimonious meeting Friday.[i] Now many Energy firms are preparing for another lean year in 2016, with some reportedly weighing dividend cuts. Even Master Limited Partnerships (MLP), long loved for their occasional tax advantages and high yields, are getting sucked into the vortex-and catching many unitholders off guard, due to the way these securities are often sold. MLPs themselves are a fine thing and, like most asset classes, have their day in the sun as well as the rain. But they aren't risk-free, and in our experience, too many investors don't quite understand those risks. As with any investment, it's important to look past the sales pitch and understand what, exactly, you're buying.

Our beef here isn't with MLPs. It's with the frequent sales tactics. MLPs are often pitched as tax-friendly, high-yielding income securities-bond replacements, if you will. They are also pitched as steady investments in Energy infrastructure that aren't vulnerable to oil prices' swings. Prospective buyers might hear analogies likening oil and gas transportation revenues to bridge toll, claiming pipeline charges will stay constant even when oil and gas prices are low, as producers will still have to transport the stuff.

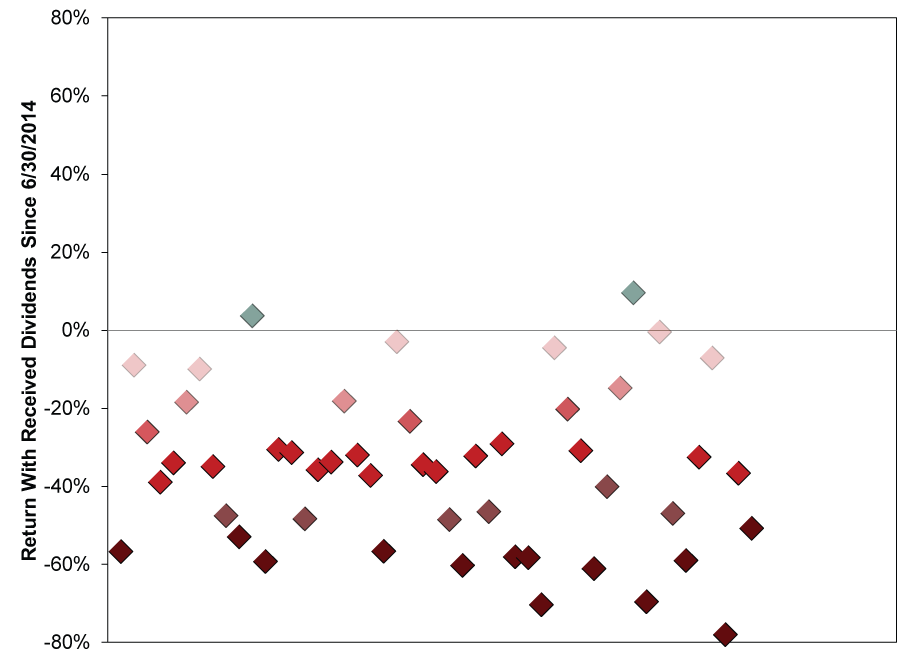

Like most things that sound like a can't-miss deal, these claims deserve some scrutiny-and they don't hold up. Yes, MLPs are high-yielding, but as ever, yield is only one component of return. Price movement matters, too, and MLPs have taken a bloodbath since June 2014, just like oil prices. Of the Alerian MLP Index's 49 constituents, 47 are negative since June 30, 2014, with a median total return of -37.3%. For folks who didn't reinvest the distributions, the median return is -34.9%. But company-specific returns vary wildly, from 9.6% to -77.9% (Exhibit 1).

Exhibit 1: Scatterplot of Alerian MLP Index Constituent Returns Including Dividends Received Since 6/30/2014

Source: FactSet, as of 12/7/2015. Alerian MLP Index constituent returns with received dividends, 6/30/2014 - 12/4/2015.

The point to seeking high-yielding securities, in the eyes of many investors, is to avoid dipping into principal. But realistically, if you buy an MLP and it falls -35% including the dividends you received, your principal has been hit hard either way. This is why we urge investors not to fixate on yield, pure and simple. You must always consider total return.

MLPs are far more oil-price sensitive than advertised. Though MLPs aren't a direct play on oil firms' revenues, oil prices influence production, which in turn drives oil transportation and, by extension, pipeline charges. Price changes are a signal to producers-goose production when prices are high, and cut back when they're low. Thus falling oil prices make it extremely likely production will eventually fall, reducing the amount of oil and gas transported, and hitting transportation (and other infrastructure) firms' revenues. While production hasn't yet fallen significantly, markets are efficient and pretty good at pricing in widely anticipated future changes. US oil production's eventual fall is widely anticipated. Hence why many expect MLPs to cut their distributions in 2016 as revenues drop.

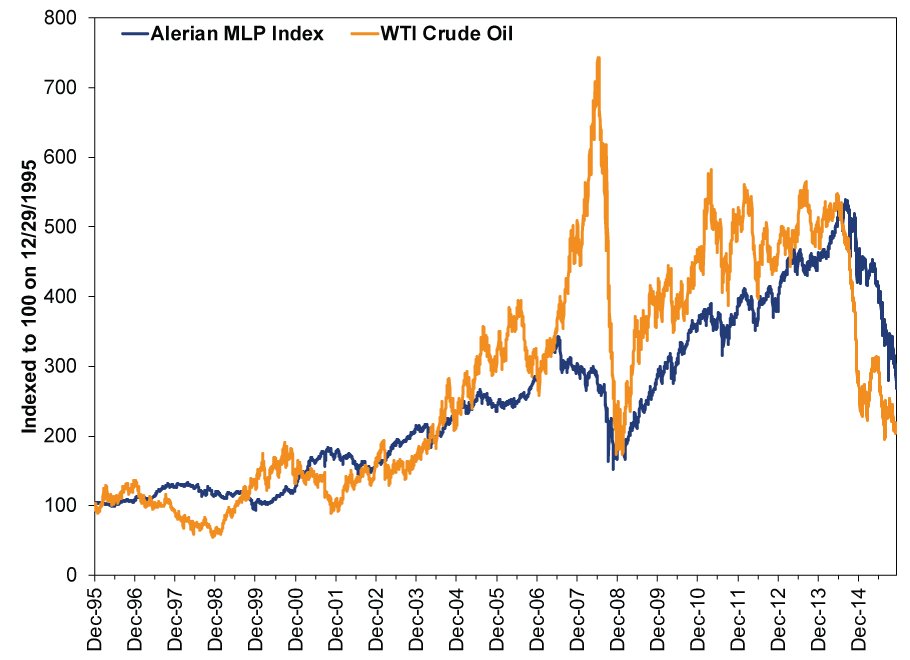

History shows MLPs and oil prices have a strong relationship. Exhibit 2 tracks the Alerian MLP Index and WTI crude oil prices since 1995. Though oil's swings are wilder, directionally, the two track quite closely. The correlation coefficient is 0.83-high, and not coincidental.

Exhibit 2: MLPs and Oil

Source: FactSet, as of 12/7/2015. Alerian MLP Index and West Texas Intermediate crude oil, 12/29/1995 - 12/4/2015. Indexed to 100 on 12/29/1995.

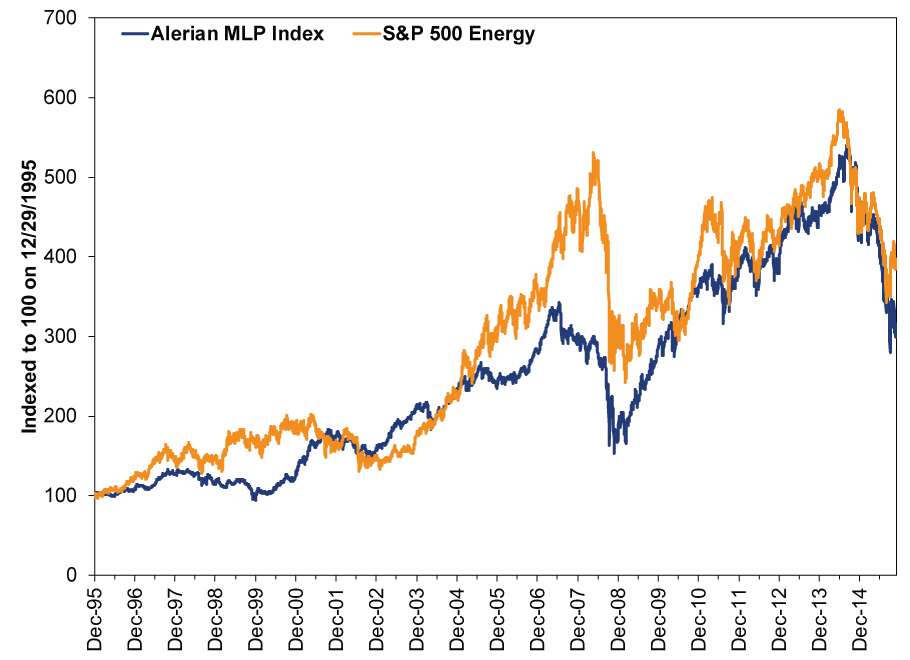

The widely held misperception about MLPs and oil prices leads to a glaring error: overconcentration. In our experience, many investors fail to look beyond the high yield and consider MLPs as equity investments in the Energy sector. We still, even now, see investors approach us with big positions in MLPs and Energy stocks, mentally accounting for the MLPs as an income investment and the Energy stocks as part of their diversified stock portfolio. Unfortunately, this isn't diversified at all. MLPs don't just track oil prices. They also track Energy stocks extremely closely, as Exhibit 3 shows.

Exhibit 3: MLPs and Energy Stocks

Source: FactSet, as of 12/7/2015. S&P 500 Energy Index and Alerian MLP Index total returns, 12/29/1995 - 12/4/2015. Indexed to 100 on 12/29/1995.

The Energy sector is currently just under 7% of the S&P 500, by market capitalization.[ii] (On June 30, 2014-before oil's bloodbath began-Energy was about 10.9% of the S&P 500.[iii]) An investor with just 10% of their portfolio in MLPs and the rest in an S&P 500 Index fund would have about 16% of their holdings in Energy firms-a huge overweight. It isn't unusual for folks to have even greater exposure to MLPs, ratcheting up sector-specific risk. A diligent financial professional should at least apprise you of this, if not outright dissuade you. This was especially true as MLPs racked up strong gains earlier in this bull market, and it reminded us a lot of folks who plowed into Tech stocks in the very late 1990s. (But on a smaller scale-Tech was nearly 30% of the S&P back then. Energy as a whole never approached that this time.)

MLPs' tax benefits also deserve more scrutiny than salespeople give them. It's true the limited partnership structure allows the firm to reduce its own tax liability. And it's true the MLP's distributions to unitholders aren't taxed immediately, as they are typically in part return of capital, not return on capital. But investors still pay the piper eventually. When the MLP is sold, the distributions are subtracted from the initial investment's cost basis, creating a larger taxable realized gain. This nuance is often buried in fine print. Also buried is the fact that MLPs can trigger tax bills in IRAs and other tax-deferred retirement accounts. We read regularly about investors learning this the hard way.

Again, we think MLPs are a fine tool in general, and at times they can add significant value. But investors considering them should understand all the risks and tradeoffs and what drives revenues, and not view them as steady income with zero sector-based risks.

[i] And, oddly, from weather forecasts, which project temperatures 10-25 degrees above normal throughout the US over the next two weeks-sparking fears a warm El Niño winter could sap demand for home heating fuel, putting more downward pressure on prices. We kid you not, this was all over the financial media Monday.

[ii] FactSet, as of 12/7/2015. Market capitalization of S&P 500 and S&P 500 Energy on 12/4/2015.

[iii] FactSet, as of 12/7/2015. Market capitalization of S&P 500 and S&P 500 Energy on 6/30/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today