Personal Wealth Management / Market Analysis

What to Make of German Recession Chatter

As recession forecasts mount, all eyes are on Europe’s largest economy.

Last Friday, Germany released its revised estimate of Q3 GDP, and its 0.4% q/q growth was better than the initial estimate announced in late October—which also beat expectations. While backward-looking Q3 growth doesn’t mean Germany will sidestep recession, economic reality has been faring better than most anticipated. In our view, this is the type of positive surprise that often underlies a stock market recovery.

Germany’s initial GDP estimate doesn’t have a component breakdown beyond statisticians’ general commentary about what drove growth, but now we have the detailed numbers. As national statistics agency Destatis hinted at earlier, household spending was a key contributor, rising 1.0% q/q.[i] The agency noted sharp price increases didn’t dissuade consumers from spending in Q3—especially on travel, with nearly all of the country’s COVID restrictions removed. Though gross fixed capital formation fell -1.4% q/q in construction, investment in machinery and equipment was up 2.7%.[ii] Trade was resilient, too, with exports (2.0%) and imports (2.4%) both up on a quarterly basis—a sign of solid external and domestic demand.[iii] Considering these data are all adjusted for inflation, activity appears to have held up despite high prices. On a sector basis, manufacturing surprisingly contributed on a gross value added basis, as did most services industries.[iv] German Q3 GDP also climbed above its pre-pandemic level for the first time—a fun, if arbitrary, milestone.

The growthy data are notable considering many think Germany is on the precipice of a recession, if not already in one, primarily tied to the ongoing economic ripples from Russia’s invasion of Ukraine. Moscow responded to Western sanctions by throttling natural gas flows to Europe, hurting Germany in particular. Not only was Russia Germany’s top supplier pre-invasion, but the country depends on natural gas for energy and feedstock to power its large chemicals industry.

Now, restricted energy supply has weighed on the economy. Though the Q3 GDP report didn’t provide detailed figures, Destatis noted output fell in energy-intensive manufacturing categories, including chemicals and chemical products and basic metals.[v] That is consistent with Germany’s industrial production gauge, as the chemical and pharmaceuticals products category has contracted on a monthly basis in seven of nine reported months.[vi] But so far, less commodity-sensitive industries within manufacturing have more than picked up the slack. If chemical companies’ situation worsens beyond electrical and computing devices and equipment manufacturing’s ability to offset their declines, then manufacturing output could turn negative. But we think it is worth nothing that the expected hit to Germany’s industrial sector hasn’t derailed broader growth thus far.

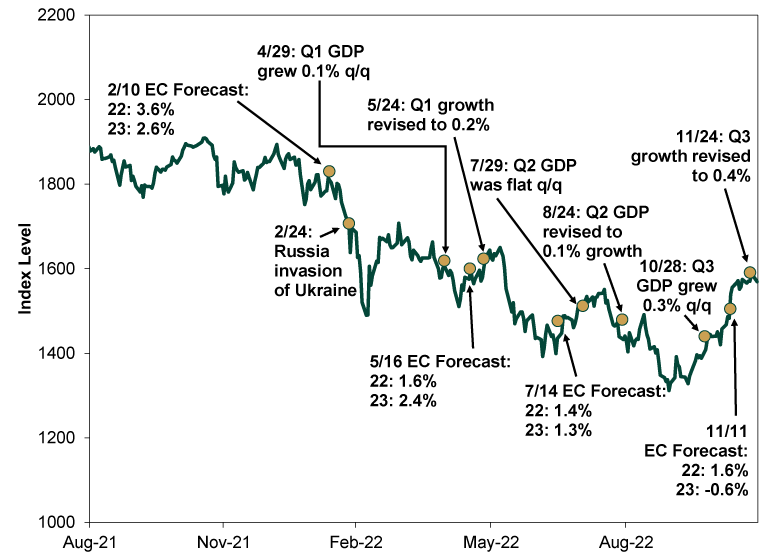

That said, a German recession also wouldn’t shock. Late last year, economists discussed the prospect of recession tied to energy supply concerns, elevated inflation, ongoing COVID restrictions and supply chain bottlenecks.[vii] That chatter increased after Russia invaded Ukraine and the West responded with sanctions, and many now think recession is a given next year. But this scenario isn’t sneaking up on stocks. In our view, German stocks’ behavior over the past 12 months has been consistent with an approaching recession.

As Exhibit 1 shows, after their November 2021 high in euros (to avoid the strong dollar skewing the picture), German stocks fell -30.8% through the end of September.[viii] (They have since clawed back some of that decline.) Over those 10 months, the European Commission (EC) has steadily lowered its German economic forecasts. Per its latest estimate, German GDP will grow 1.6% in 2022 and contract -0.6% next year. But German stocks haven’t waited for statistics agencies or supranational organizations to officially confirm whether the economy was in recession or not: They pre-priced the weakness.

Exhibit 1: German Stocks Aren’t Ignoring Weak Economy Talk

Source: FactSet and European Commission, as of 11/29/2022. MSCI Germany IMI Index returns in euros with net dividends, 8/31/2021 – 11/28/2022. Returns in euros to avoid currency skew from the strong USD. European Commission releases its annual growth forecasts four times a year.

The EC’s view isn’t an anomaly, either. At this point, a German recession appears to be the baseline expectation. Back in August, the Bundesbank, Germany’s central bank, said declining output in the winter months looked likely.[ix] The following month, the OECD forecast a GDP contraction in 2023, as did German multinational Deutsche Bank.[x] The IMF followed suit in October with its own 2023 German recession call.[xi] If the data confirm a downturn, we think stocks likely already reflect the impact to a great extent. In our view, reality would have to turn pretty bad to negatively surprise markets. But if the data end up even a tad better than thought, that outcome would likely count as a positive surprise. Between those two scenarios, the data thus far suggest to us the latter is more likely.

This doesn’t mean a recession, if one materialized, wouldn’t create hardships for people and businesses. It likely would. But in investing, it is critical to view the economic environment as stocks do: Is anything here a surprise? If it isn’t, stocks have likely digested and reflected the news already. With the numbers implying Germany’s economy isn’t in the dire straits many think, reality seems likely to positively surprise, in our view.

[i] Source: Destatis, as of 11/28/2022.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

[vi] Source: FactSet, as of 11/29/2022.

[vii] “Recession Risk Looms for Germany as Business Confidence Falls,” Martin Arnold, Financial Times, 12/17/2021.

[viii] Source: FactSet, as of 11/29/2022. MSCI Germany IMI Index returns in euros with net dividends, 11/4/2021 – 9/29/2022.

[ix] “German Recession Increasingly Likely, Bundesbank Says,” Staff, Reuters, 8/22/2022.

[x] “Energy, Inflation Crises Risk Pushing Big Economies Into Recession, OECD Says,” Leigh Thomas, Reuters, 9/26/2022 and “Deutsche Bank CEO Warns Recession Is Inevitable, Says Germany Must Cut Reliance on China,” Elliot Smith, CNBC, 9/7/2022.

[xi] “IMF Says Germany and Italy to Slip Into Recession in 2023,” Staff, Deutsche Welle, 10/11/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today