Personal Wealth Management /

When to Start Social Security? Some Basic Considerations

Starting Social Security payments can have lasting consequences. What should you weigh beforehand?

When retirement nears, you will face many big decisions. Exactly when should you retire? What should you do with your time? Lastly, one of the biggies: When should you start taking Social Security payments? The inconvenient truth: There is no one-size-fits-all answer. You must weigh key variables like your year of birth, work history and health—as well as your income sources outside Social Security. Here is a brief primer on how to get started.

First, the basics: To be eligible for Social Security benefits, you must have at least 10 years work history. The amount you are eligible for fluctuates based on your highest 35 years’ earnings. The highest benefit you can qualify for at your full retirement age (FRA) presently is $2,861 monthly (although you can increase this—more on that later). To find out your benefit eligibility, follow the calculation steps here. You can also check your annual Social Security benefit statement, give the Social Security Administration (SSA) a call or pay them a visit.

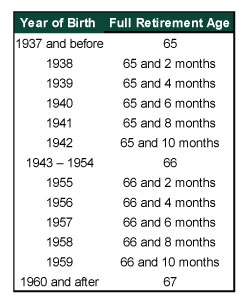

The above discussion cites full benefit amounts—but you have to be eligible for them first! This hinges on your birth year, based on a schedule Congress has tweaked a number of times historically. Exhibit 1 plots FRAs by birth year under current law.

Exhibit 1: Full Retirement Ages for Retired Worker and Spouse Benefits

Source: Social Security Administration, as of 7/22/2019.

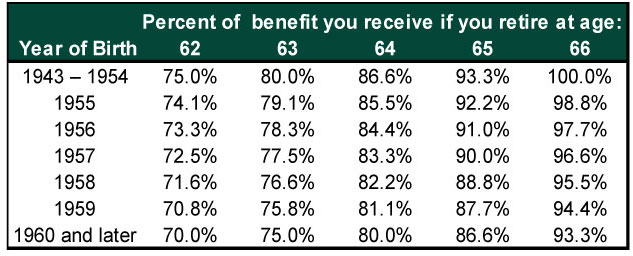

You can tap Social Security sooner—as early as age 62. But if you start before your FRA, the government reduces your benefit amount. The further from full retirement age, the more the Social Security Administration slashes. Exhibit 2 shows the impact taking benefits early may have.

Exhibit 2: Percent of Benefit Received if Retiring Early

Source: Social Security Administration, as of 7/22/2019.

Note: This lower amount determines future cost-of-living adjustments. A lower amount now means smaller increases going forward, too—benefits compound from a smaller base. If you are married, you should also consider the potential impact on your spouse. While your decision won’t affect their primary benefit—they are entitled to their own benefit or 50% of yours. However, if you pass away, your spouse would receive survivor benefits based on your reduced payments.

If you can put off taking payments beyond FRA, it may pay to do so. Benefits rise through age 70—even beyond the aforementioned maximum—if you defer. The amount of extra benefit depends, again, on your birth year. But for folks born in 1943 or later, benefits increase 8% each year you wait past full retirement age. Delaying as long as possible can mean as much as a 32% higher monthly benefit when you do start taking them—and as an added bonus, future cost of living increases start from a higher base.

So what should you consider when weighing a decision to start Social Security payments?

First, know that getting this right takes work. Moreover, there is only a one-time opportunity to change you mind—if you are within a 12-month window from the first payment. Even then, switching means you must repay any benefits you received in full.

Before you choose, consider your options. Start by using the SSA’s tools or an office visit to estimate your benefits. But don’t stop there. Remember taxes play a role, too. The IRS’s website can help you sort out how much of your benefit is taxable. If math isn’t your forte, we recommend consulting a tax professional. Understanding your likely after-tax situation is key.

Crucially, you should consider how various Social Security payment amounts would affect your cash flow needs throughout retirement. To start with, create a detailed budget (if you don’t already have one). Online tools can help—from your bank, Mint.com or elsewhere. Once you have a sense of your monthly spending—use several months as a baseline to catch potential fluctuations—compare this to various Social Security benefits—early, full and deferred. If you have a pension, factor that in here, too. The question you seek to answer: How much would you need to draw from your retirement savings in different Social Security payment scenarios? If delaying Social Security (to full retirement age or beyond) means your annual withdrawal needs will exceed 5% of your portfolio’s value, think carefully. Levels above this range risk depletion, especially early in retirement. If delaying means you far exceed this mark, taking benefits early—or working longer—may be valuable. Even a part-time job can bolster income early in retirement and help bridge the gap to full retirement age. At that point, you can revisit.

If you can wait beyond FRA, the higher benefits may mean many years of lower withdrawals, allowing your assets to compound and grow—with potentially huge upside. Is this right for you? Consider your goals. Are you trying to leave an inheritance to family or charity? Or would you laugh if your last check bounced? If you are relatively healthy with a family history of longevity, taking benefits late may mean a bigger portfolio to pass to your heirs (due to taking smaller withdrawals for longer). Delaying as long as possible also maximizes your benefit—which can help you finance costly healthcare treatments, assisted living or other expenses late in life. If you can swing it and it matches your goals, delaying may make sense. But we don’t think this is always or even usually true. You must weigh the potential positives against the likely portfolio impact, in our view.

Finally, laws change over time, potentially affecting your benefits. Hence, regularly revisiting your plan is likely a good idea. For example, in 2015 Congress eliminated “File and Suspend”—which allowed retirees to turn on spousal benefits while delaying primary benefits beyond full retirement age, boosting monthly payments in the process. Such changes may not happen every day, but they happen often enough that those relatively near retirement should stay on top of things. Keeping abreast of possible future changes reduces the risk of a nasty surprise.

Ultimately, there is no “right” decision for everyone. It is personal. The SSA can help if you pay them a visit. But be sure to weigh the decision yourself, too.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today