Personal Wealth Management / Market Volatility

Understanding Bull Markets

When it comes to discussing financial markets, investors will encounter industry-specific jargon. Wall Street professionals and financial media outlets often use terms such as bull, bear, beta and risk profile to describe prevailing stock market conditions or fears. But what is a bull or a bear? In this article, we aim to provide clarity on one of these industry-specific terms: bull markets.

Bull Market Characteristics

Bull markets are periods—typically multiple years—when stock prices generally rise in the long term. You can expect equity market indexes to rise and stock valuations to climb. Conversely, bear markets are periods—often ranging between roughly six months to two years—in which some fundamental factors drive stock prices downward approximately 20% or more. While the definitions may vary across the industry, the general distinction is that bull markets are rising markets, and bear markets are falling markets.

However, it’s crucial to understand that bull markets don’t rise in a straight line. Stocks normally encounter bumps or drops along the way, usually driven by overblown investor fears. We call some of these bull market drops “corrections”. Corrections are short, sentiment-driven drops of 10% to 20%, which often start quickly. Because they are usually fear-driven, they can be happen at any time for any or no reason and are normally sharp and swift. When they are over, stock prices may quickly resume their upward trend, which can make trying to time bull market corrections a futile exercise.

As bull markets mature, investor sentiment—how investors feel—becomes more optimistic. While it can be difficult to gauge the emotion of a large group of investors, some examples of things we monitor are initial public offering (IPO) activity, margin debt levels and stock mutual fund inflows and outflows. Mutual fund inflows, for instance, can help show investor sentiment because as markets rise and optimism increases, investors become more comfortable putting their money into the stock market and fund inflows increase. However, after a downturn investors fear losing money and may sell off their mutual funds or other securities. This pessimistic outlook often causes investors to miss out on early bull market returns, potentially reducing their ability to meet their long-term financial goals.

The Importance of Investor Sentiment

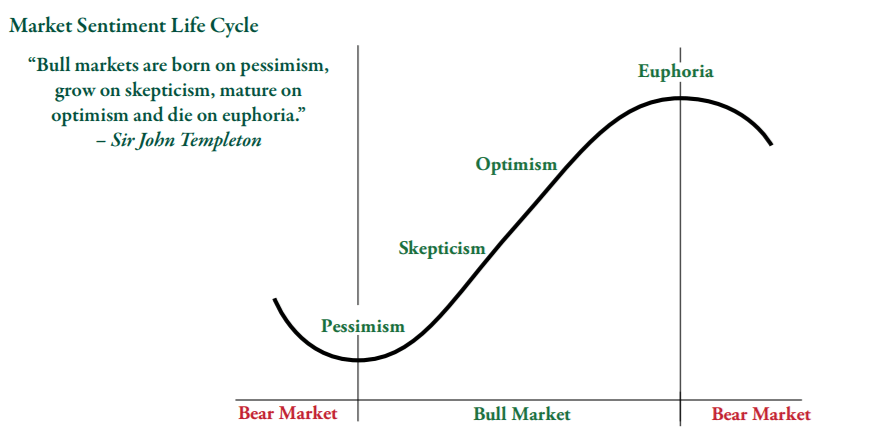

When you look at historical charts, it may appear easy to stay invested during a bull market from bottom to top. Investors are often unaware of the potentially counter-intuitive or contrarian nature of investor sentiment. Sir John Templeton described investor sentiment and its relation to the market cycle, saying, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.”

Exhibit 1: The Market Sentiment Life Cycle

The above is intended to illustrate a point and does not reflect actual returns or market behavior.

Investors are often most pessimistic at or near the bottom of a bear market. After the stock market has endured a sustained downward trend, investors tend to have overly dour expectations—a sign of pessimism. When prices begin to rise consistently, skepticism begins, as folks are hesitant to invest again. Despite widespread skepticism, in a bull market, companies continue to beat overly dour expectations and more investors step into the market as prices continue to rise, creating optimism. During optimism, stocks are generally on a stable rise over time, investors raise expectations for regular company earnings and investors start to develop a fear of missing out on future returns.

The final stage in the Templeton’s cycle is euphoria. As investors throw caution to the wind and look for the next hot investment, euphoria can lead them to dismiss fundamental economic issues and continue to look for reasons why the market should continue rising. Emotions and biases are often investors’ nemeses. Because investments aren’t intuitive, investors can often sell stocks when they should be holding or buying. Making poorly-timed investment decisions based on emotion can threaten your ability to achieve your longer-term investment goals.

Bull vs. Bear: When to be Bullish

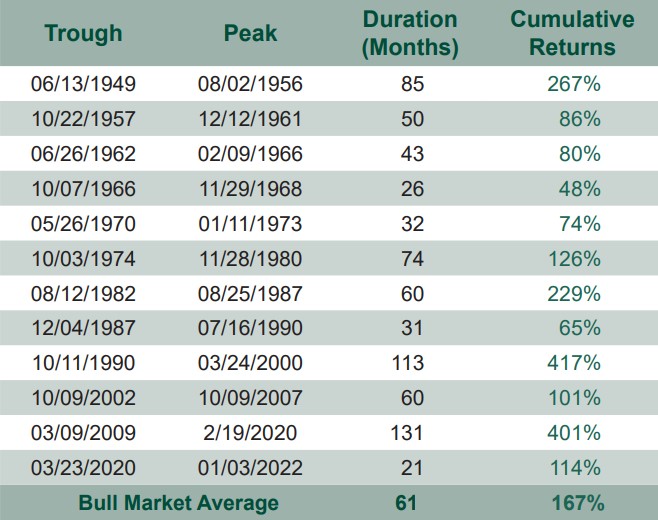

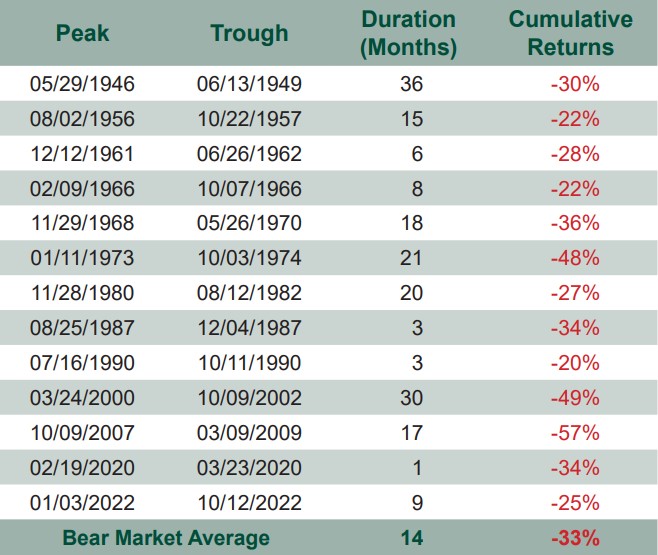

Being bullish is a form of optimism and means believing the market will rise in the foreseeable future. History has shown bull markets last longer and returns are stronger, on average, than bear markets’ losses. As shown in Exhibits 2 and 3, bull markets have lasted from 26 months to as many as 131 months.1 Since 1946, there have been 11 bear markets with an average decline of 34% and an average duration of 16 months.2 During the same period, bull markets have averaged over five years in duration and 151% cumulative return for the S&P 500 Price Index.3

Exhibit 2: Last 12 S&P Bull Markets

Exhibit 3: Last 13 S&P Bear Markets

*For “Duration,” a month equals 30.5 days.

Source: Global Financial Data, as of 3/24/2020; S&P 500 Index Price Level from 5/29/1946 - 12/30/2013. FactSet, as of 3/24/2020; S&P 500 Index Price Level from 1/1/2014 - 2/19/2020.

During bear markets, investors who act on emotion typically sell their investments near market lows. Due to the losses incurred, investors may be reluctant to invest again when the market initially rebounds. They want more proof the rebound isn’t just a temporary bounce. As they wait on the sidelines, they miss out on the often steep bull market beginning. This mistake can be especially costly because investors often endure much of a downturn, and miss the initial rebound, which can help them recoup some of their losses—further detracting from their long-term returns. Missing this initial upswing can set you further back and may even prevent you from reaching your long-term financial goals. That’s one more reason why reacting emotionally to market developments can be costly in the long run.

Investments come with many different risks. One of the most overlooked risks is the risk you don’t achieve the long-term growth you need to achieve your long-term goals. Missing the initial upswing in a bull market can be costly and many investors don’t account for this cost. It can severely increase your risk of missing out on the necessary growth needed to meet your long-term financial goals.

How We Can Help

At Fisher Investments, we help our clients navigate capital markets, and clients can reach out to their client service team with questions along the way. To learn more, download one of our guides or speak with one of our experienced professionals today.

Investing in securities involves a risk of loss. Past performance is never a guarantee of future returns.

Investing in foreign stock markets involves additional risks, such as the risk of currency fluctuations. The foregoing constitutes the general views of Fisher Investments and should not be regarded as personalized investment advice or a reflection of the performance of Fisher Investments or its clients. Nothing herein is intended to be a recommendation or a forecast of market conditions. Rather it is intended to illustrate a point. Current and future markets may differ significantly from those illustrated here. Not all past forecasts were, nor future forecasts may be, as accurate as those predicted herein.

1 Global Financial Data, as of 3/24/2020; S&P 500 Index Price Level from 5/29/1946 - 12/30/2013. FactSet, as of 3/24/2020; S&P 500 Index Price Level from 1/1/2014 - 2/19/2020. For “Duration,” a month equals 30.5 days.

2 Source: Global Financial Data, as of 2/5/2018; S&P 500 Index Price Level from 5/29/1946 – 12/30/2013. FactSet, as of 2/5/2018; S&P 500 Index Price Level from 1/1/2014 – 2/2/2018. For “Duration,” a month equals 30.5 days.

3 Global Financial Data, as of 3/24/2020; S&P 500 Index Price Level from 5/29/1946 - 12/30/2013. FactSet, as of 3/24/2020; S&P 500 Index Price Level from 1/1/2014 - 2/19/2020. For “Duration,” a month equals 30.5 days.

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Insights & Media

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today