Personal Wealth Management / Politics

A Look at Egypt and Global Markets

Tensions are flaring in Egypt, but history shows this shouldn’t much impact global stocks.

Military planes fly over Egypt’s Tahrir Square the day after President Mohammed Morsi’s Ouster. Photo by Spencer Platt/Getty Images.

Tensions are flaring in Egypt, where the military has deposed President Mohammed Morsi and installed Chief Justice Adly Mansour as interim president. Civil unrest continues, with protests turning violent, but long-term growth investors needn’t fret—history shows geopolitical tensions have only a fleeting, and not necessarily negative, impact on global stocks in the mid- to long-term.

Morsi’s ouster came after months of civilian protests and division between supporters of Morsi, his Muslim Brotherhood party and the opposition. The opposition has grown increasingly restive over Egypt’s weakening economy and Morsi’s attempts to consolidate power. Millions of Egyptians demonstrated against him last weekend, calling for his resignation. On Monday (July 1), the military gave him and the opposition 48 hours to resolve their differences—with no results. So on Wednesday (July 3), the military took action, detaining Morsi, installing Mansour, suspending the constitution and calling for new elections.

How this plays out is far from certain—elections aren’t yet scheduled, and demonstrations continue. Even if free and fair elections happen soon, uncertainty likely persists as Egypt drafts another constitution. However, this shouldn’t disrupt profitability of businesses globally—the key driver of global stock returns. Egypt is a tiny sliver of the global economy and capital markets—global fundamentals typically swamp such isolated tensions.

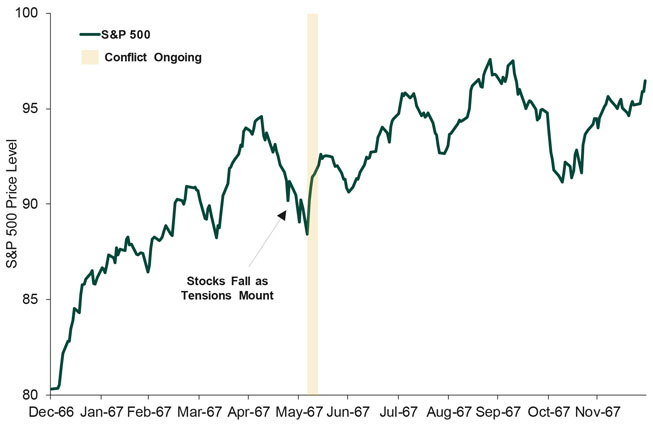

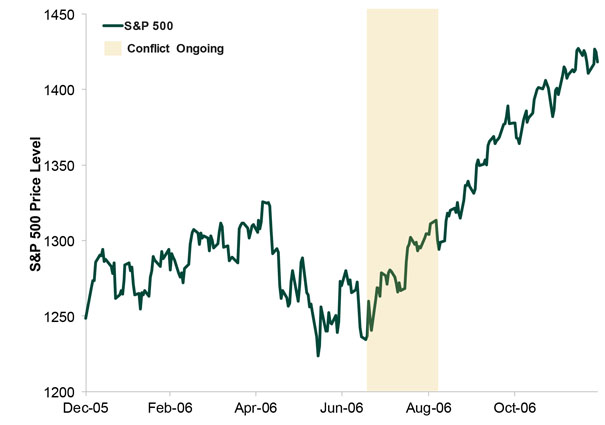

That likely stays true even if Egypt descends into further chaos—a possibility, though not necessarily probable. History shows localized conflicts—even seemingly major ones—don’t have lasting negative impacts on global equities. Volatility can increase prior to military action, but an outbreak of conflict often alleviates uncertainty. For example, stocks fell before the Six-Day War among Israel, Egypt, Jordan and Syria but rose every session after the outbreak (Exhibit 1). Markets were similarly volatile ahead of the Israel-Hezbollah conflict in 2006 but rallied well before the conflict subsided (Exhibit 2).

Exhibit 1: Six-Day War and S&P 500 Price

Source: Federal Reserve Bank of St. Louis, as of 7/5/2013.

Exhibit 2: Israel-Hezbollah Conflict and S&P 500 Price

Source: Federal Reserve Bank of St. Louis, as of 7/5/2013.

There are many other examples. The 1956 Suez Crisis, a 1958 spat between China and Taiwan, Brazil’s 1964 coup, Lebanon’s 1976 Civil War and both Gulf Wars occurred during positive years for global markets. The Nazi Invasion of the Sudetenland is the only modern example of armed conflict knocking a bull off course—and that bear market ended in 1942, three years before the war’s end.

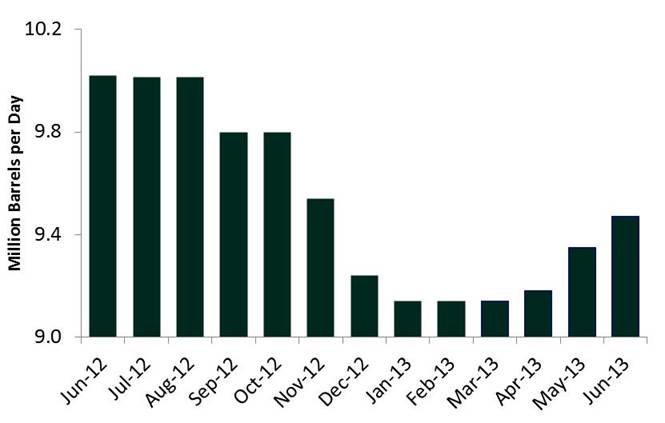

Energy markets likely prove similarly resilient. Egypt’s oil production is less than 1.0% of the world’s total—likely easily replaced by major producers. Global oil production has some spare capacity, as some OPEC producers have cut production to offset the US’s shale boom. Saudi Arabia, for example, has cut output from 10.15 million barrels a day (MB/D) last June to the 9.47 MB/D estimated for June 2013 (Exhibit 3).

Exhibit 3: Saudi Arabian Oil Production

Source: Thomson Reuters, as of 7/5/2013.

A potential closure of the Suez Canal would likely have some impact, but it’s not guaranteed to happen. Though the likelihood of closure is impossible to predict—it’s not a market function—it’s worth noting the military and opposition have incentives to keep the passage open. Egypt’s already under severe economic pressure, having depleted over half its forex reserves since 2010 in an effort to defend its currency. A long-in-the-works $4.8 billion IMF loan still isn’t final, and every source of economic activity is precious. And even if oil prices creep up, history shows no meaningful correlation between stock and oil prices.

Egypt has experienced much political upheaval since Hosni Mubarak’s 2011 ousting, and only time will tell where the country goes from here. For equity investors though, this is a largely academic question, as countless other variables impact global stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Expert Commentary 3 Things You Need to Know This Week | Global Inflation, Fed Minutes, US Sentiment2026-05-18

-

In The News Around the World in Tax Policy Talk2026-05-15

-

Expert Commentary This Week in Review | US Inflation, US-China Visit, Fed Chair Confirmation

2026-05-15

2026-05-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today