Personal Wealth Management / Economics

A Manufactured Buzz?

Manufacturing is strong, but investors still seem skeptical of US economic strength.

Shale oil extraction in North Dakota has been a part of the manufacturing boom. Photo by Andrew Burton, Getty Images.

US manufacturing stayed hot in August, with the ISM PMI hitting 55.7—up 0.3 from July and beating expectations of 54 (above 50 indicates growth). Though less than 15% of the US economy, manufacturing is a key driver of the ongoing expansion—and its still-underappreciated strength is one more sign this bull market has plenty of fuel.

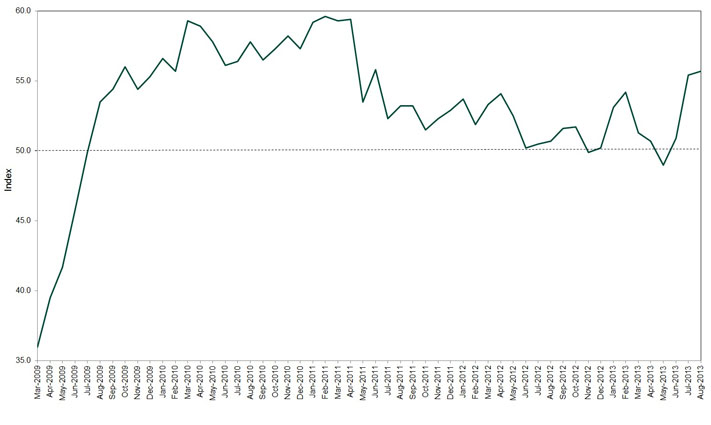

Headlines seem surprised every time manufacturing expands, suggesting folks don’t quite fathom how strong the category is. Perhaps they’re still stuck on May’s small contraction, ignoring every other month this year saw expansion. Looking even further back, there have only been two contractions during this bull market, both mere blips along the way to longer-term growth (Exhibit 1).

Exhibit 1: ISM Manufacturing: PMI Composite Index since March 2009

Source: St. Louis Federal Reserve, as of 9/4/2013.

Looking ahead, the index’s underlying components point to more growth. The New Orders subindex—the most forward-looking component—hit 63.2 in August, up +4.9 points from July—the highest reading since April 2011. Of the 18 covered industries, 12 reported growth, including textile mills, wood products, computer & electronic products and plastic & rubber products. In the coming months, these new orders should lead to higher production—and, with demand still firm, higher sales. It’s happening already! The Production Index hit 62.4—decelerating from July’s 65, but still the second-highest since March 2011. Rising production in July and August followed rising new orders earlier this year—with new orders today way higher, the potential for even higher production increases in the coming months appears high.

If the US economy were weakening, this wouldn’t happen—it’s all a byproduct of healthy demand. Retail sales are high and rising in the US and globally, and overall and on average, inventories are falling—firms can’t keep up. So they order more goods to replenish stockpiles, ultimately boosting factories up and down the supply chain. Not just in the US: The UK, eurozone and China also reported faster manufacturing growth—again driven by new orders. And they, too, beat expectations and initial flash estimates, suggesting sentiment remains too dour. Positive surprise power persists! Just one more indication sentiment remains stuck between skeptical and optimistic. Folks are willing to cop to manufacturing’s strength as it’s reported—they aren’t much portraying it as potentially fleeting—but they’re surprised nonetheless. This is happening broadly throughout the global economy—one more indication this bull has room to run.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today