Personal Wealth Management /

A New Leader for India

But do expectations exceed reality?

Indian voters went to the polls over the last six weeks and it seems they’ve again cast ballots hoping for economic reform. This time, they’ve pinned those hopes on Narendra Modi, who won what seems like a mandate in the voting. And it appears Indian investors bought the hype too, with the MSCI India Index surging 7.89% since polling began.[i] (And the upswing predates voting, which may be influenced in part by Modi’s gaining strength in the polls.) For the rally to turn into more lasting outperformance, though, it will likely take Modi following through with actions backing up the talk.

Modi’s Bharatiya Janata Party (BJP) beat Rahul Gandhi’s and current Prime Minister Manmohan Singh’s Congress party in a landslide—taking 282 of the 545 seats. The margin of victory is the biggest since 1984, when Rajiv Gandhi led the Congress party to take 80% of the seats. Part of the lopsided result is likely just how unpopular and feckless Singh’s administration is—a vote against Congress as much as for Modi. But still, Modi filled his campaign with a laundry-list of promises—a corruption-free government, building bullet trains, hydroelectric power plants, manufacturing centers and even more cities. A wee bit ambitious, in our view, but hopes are high and Indian stocks are popping. (Exhibit 1)

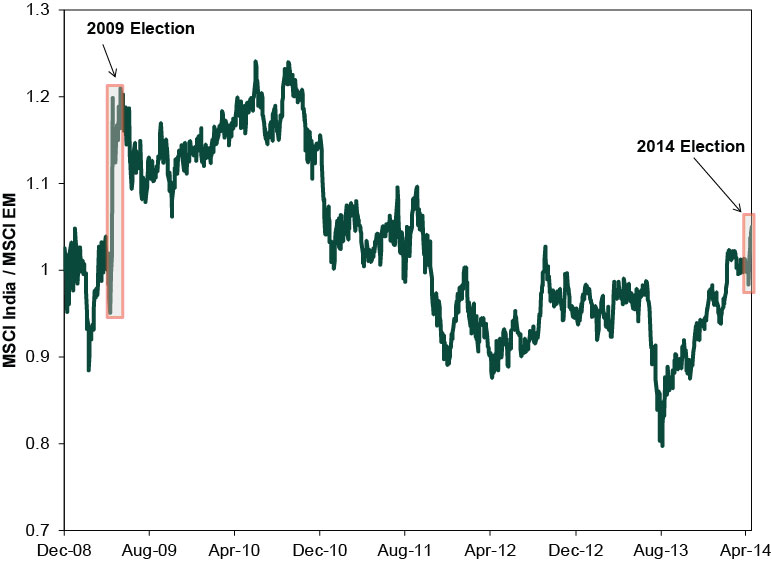

Exhibit 1: India’s Relative Performance to Emerging Markets

Source: FactSet, as of 5/19/2014. MSCI India Total Return Index and MSCI Emerging Markets Total Return Index. Note: When the line is rising, India is outperforming Emerging Markets. 2009 Election (4/16/2009-5/13/2009). 2014 Election (4/7/2014-5/12/2014).

Talk is one thing, though, and action is another. Like many leaders who cruise to victory on big reform platforms, it isn’t clear how much he’ll actually accomplish. Take the election of Japanese Prime Minister Shinzo Abe. In 2012, he cruised to victory on promises to revive Japan’s economy with “three arrows” of reform (also known as “Abenomics”)—monetary stimulus, fiscal stimulus and economic reform. A year later, Abe fired the first two. The third seems thus far to be a bit of a dud.

India has seen its share of big reform talkers, too. In 2009, Modi’s predecessor Manmohan Singh led the Congress party to victory on big reform pledges. He promised to reduce bureaucracy, boost infrastructure, introduce labor market and tax reforms and help open up India’s doors to foreign investment, to name a few. Then, markets reacted positively as well! But over the last five years Indian economic growth slowed markedly, corruption remains and those expecting reforms are still waiting. For instance, Singh stumped on the first major tax reform in 50 years but it still has yet to materialize. Reality didn’t quite match the initial optimism.

Investing big hope in any one leader of the world’s most populous democracy is a little misguided, as any one person isn’t likely the game changer making all the economic difference. Maybe Modi’s big win will motivate more leaders to cooperate with him. A primary problem is India’s political system puts a lot of power in the hands of the states—where leaders may have entirely different ideas about the desirability of reforms. For this reason, though Singh’s government didn’t prove terribly skilled at navigating the Federal bureaucracy, even when it did get reforms through, implementation didn’t necessarily follow. For example, Singh’s government proposed a plan to implement a single, national goods and services tax (GST), but it stalled. Why? It would place the central government’s authority to tax above the states, who would then be allotted a transfer payment—unconstitutional in India. To pass this measure—which businesses favor due to reduced red tape—would require revising the constitution. Half the states have to support such a move, support Singh lacked as many state leaders fear losing their tax bases and relying on central government transfers is a shot at their independence. Businesses still want the national GST, but whether Modi has sufficient support to overcome entrenched interests is unclear.

Another example: Singh’s government tried to keep its promise to open India’s markets to foreign retailers and actually passed a model law in 2012. The law sought to encourage foreign investment by allowing investors to set up multi-brand retail spaces in India—but implementation was a state matter. Singh flip-flopped on whether only single-line retailers (think: Ikea) or multi-line (think: Walmart) would be allowed to own a majority of a business. But the political gymnastics didn’t seem to make the states flip. While some states support the reform, others like Delhi (which reversed its decision to support the reform in January) don’t. That’s not to say it is impossible for the national government to implement significant reforms, but it likely will continue to face some hurdles.

With all that being said, remember: Stocks move most on the gap between expectations and reality, in the longer term. While hopes are high domestically, the foreign investing public likely stays cooler for a spell—being burned by Singh is fresh in the minds of many investors. The bar may be lower for Modi than it was for Singh. So the key question is: How much of Modi mania becomes reality?

Modi won election on hopes of a bright future, and maybe his administration has the support and clout it needs to move the needle. The degree to which he succeeds in passing reforms is likely to be critical in determining the economic and market future of the country during his turn at the helm of the world’s largest democracy.

[i] FactSet, as of 5/19/14. MSCI India Total Return Index, 4/7/14-5/16/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today