Personal Wealth Management / Market Analysis

Don’t Be Tempted By India

India’s a temptress (capital markets-wise). Don’t be seduced—at least not for the balance of 2011.

Since the days of early spice traders, outsiders have been enamored by India’s potential wealth. European explorers set off on uncharted journeys with nothing but hope guiding them in search of a faster route to India’s spices (accidentally finding North America along the way). Since then, America’s gone from uncharted land to the largest economy in the world, while India remains a land with, well, potential.

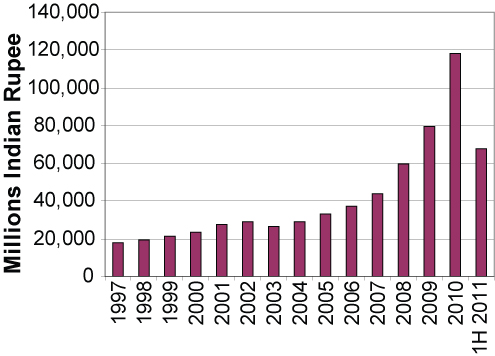

Of course, similar things could be said of other nations, but few have the potential of India: It has the world’s second largest population—over 1.2 billion—and amazingly, half are under the age of 25. What a work force! And it’s tantalizingly beginning to unleash that force in a more productive manner. State-owned enterprises are rapidly privatizing (at least 5% a year until less than 75% is publicly owned). Annual infrastructure investment surged by a whopping 250% from 2005 through 2010 and should set a new annual record in 2011. Finally, over six million people are urbanizing annually nationwide—equivalent to filling three quarters of New York City...every year!

Figure 1: Annual India Infrastructure Growth (road, rail, shipping, irrigation, power generation and distribution and telecom)

Source: Thomson Reuters.

All of which contributes to giving India the second fastest GDP growth rate in the world at nearly 8% (trailing only China). Pretty attractive, right?

But all is not rosy. A combination of historical tribal and caste divisions built upon by the former British bureaucracy has created a society light on property rights and heavy on corruption and tax evasion. Transparency International ranked India 87th in its 2010 corruption index—behind such bastions of private property rights as Ghana and Rwanda and tied with Albania and Liberia. Based on estimates from the Indian Government itself, only 3% of workers are estimated to pay personal income taxes. The major reason infrastructure has boomed is a 2005 law allowing public-private joint ventures, effectively reducing the government’s bureaucratic role in development. Now if they can simply get the permits (still no small task), private firms can build the infrastructure and operate it for a profit. But that still takes time.

The government’s web of rules, tariffs and corruption is such a problem that when Prime Minister Singh was re-elected in May 2009, India’s stock market jumped 20% the next day on hopes of economic reform. Unfortunately, as with most of India’s history, the reality hasn’t matched the hope—at least not yet.

Singh proposed the first major tax reform in 50 years, which would cut tax rates, increase tax evasion penalties and unify the nation’s sales tax, but the proposal has languished for two years and increasingly appears a pipe dream. Additional reforms to simplify land acquisition, spur foreign direct investment and allow foreign companies in a range of industries to operate independently (retailers, supermarkets and logistics firms are currently only allowed as minority joint ventures) are pending, but have been so for the better part of a decade. The same can be said for land reform to streamline acquisitions and approval of large tracts of land for infrastructure development. A number of major mining and steel firms have been waiting for over six years for approval to establish mines and plants.

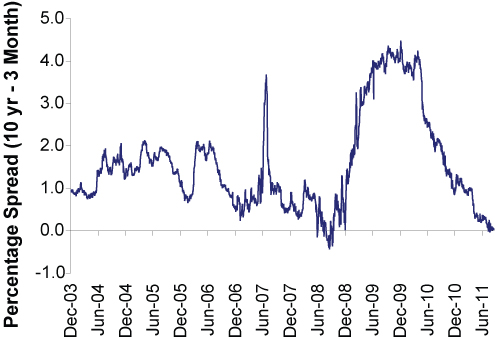

To be fair, Emerging Markets countries are classified emerging as opposed to developed for reasons, and these are some of India’s. And a good investment is often more about the marginal change versus expectations than the status quo. Unfortunately, in my view, India is not just failing to move forward; at this point, its investment conditions are seemingly getting worse. India’s attempt to combat one of the world’s highest inflation rates has led to an inverted yield curve, typically not a good sign for an economy. And additional interest rate hikes are expected—likely further inverting the curve.

Figure 2: India Yield Curve Spread (10 year minus 3 month)

Source: Thomson Reuters.

India’s economy isn’t big enough nor insular enough to buck the global trend. It likely doesn’t go into or out of recession without the rest of the world—but its markets can underperform. In fact, the lack of economic reforms and progressive inverting of the yield curve has contributed to India’s market being the third worst Emerging Markets performer in 2011—eclipsing only Egypt and Turkey.

India could still turn things around but likely not fast enough to turn this nation—with much ballyhooed “potential”—into an outperformer in the next 12 months.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today