Personal Wealth Management / Market Analysis

A Possible Leadership Rotation in 2017?

Warmer sentiment toward US stocks could tee up a rotation to non-US leadership this year.

The second estimate of US Q4 2016 GDP hit Tuesday, with growth coming in at an unrevised 1.9% annualized.[i] While this is fine enough growth for stocks-markets don't really worry about the magnitude of GDP growth, as this bull market has long demonstrated-it did miss expectations, which called for an upward revision to 2.1%. And that, folks, is what matters more: how data relate to expectations. This illustrates a broader point we are watching presently: Sentiment has warmed in America, meaning data have a higher hurdle to clear to positively surprise investors than data abroad. Should this persist, it could set up a rotation to non-US leadership later this year.

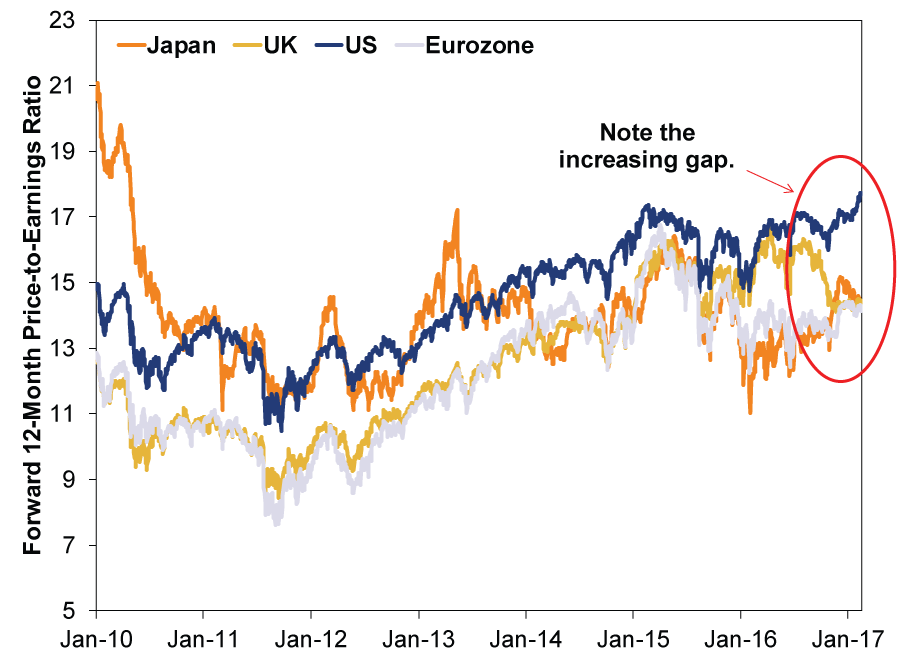

While investor sentiment has been slow to warm in America in this bull market, Europe (and, specifically, the eurozone) is even further behind. Not only did the eurozone suffer a deep downturn in 2008's global financial crisis-an anchor on sentiment for years-it experienced a second downturn from 2011 - 2013 tied to its sovereign debt crisis-driven regional recession. Fears over banks and sovereign finances have long run high. Accordingly, valuation gauges-measures of sentiment-are showing far more optimism in the US than abroad. This isn't just true versus the eurozone, either.

Exhibit 1: Relative Forward Price-to-Earnings Ratios, US v. Eurozone, UK and Japan

Source: FactSet, as of 2/27/2017. MSCI UK, MSCI EMU, MSCI Japan and S&P 500 forward 12-month price-to-earnings ratios. 12/31/2008 - 2/24/2017.

Now, those discounted valuations outside America may be warranted if data were weak or weakening. But they aren't. The eurozone has grown in 15 straight quarters; a run exceeding the US. Growth is increasingly broad-based, too-it isn't just Germany. Inflation recently turned positive in all 19 member nations, which should assuage long-lingering-but-false deflation fears. Purchasing managers' indexes show widespread growth across the eurozone private sector.

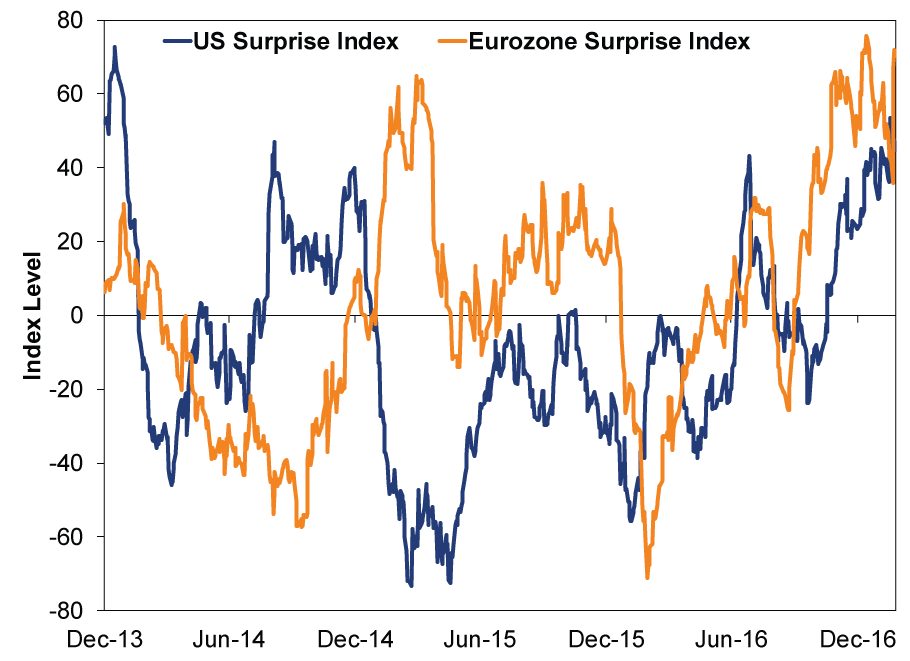

Growth isn't fast, but eurozone economic data have been positively surprising analysts more frequently than US data lately. That isn't to say US data has been "bad" or uniformly disappointing, as Wednesday's ISM Manufacturing report illustrated by beating estimates. Exhibit 2 shows the Citigroup Economic Surprise Indexes, loose measures of how economic data relate to professional forecasters' expectations. Relative to expectations, eurozone data has been better than US.

Exhibit 2: Citi Surprise Gauges, US v. Eurozone>

Source: FactSet, as of 2/27/2017. Citi Surprise Indexes (daily), 12/31/2013 - 2/24/2017.

This hasn't translated into eurozone outperformance yet in 2017, which we believe is mostly related to political uncertainty. However, that uncertainty is poised to fall throughout 2017, and as it does, investors should get a clearer view of fundamentals. If recent trends persist, that could mean a leadership rotation later this year. Investors exclusively focusing on the US should take note.

[i] Source: US Bureau of Economic Analysis, as of 2/28/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today