Personal Wealth Management / Market Analysis

A Retrospective on a Record-Book Rocky First Half

Lessons from one of the most volatile six-month stretches in history.

2020’s first half is in the books, and we reckon it is fair to say the MSCI World Index’s -5.8% decline hardly hints at all investors had to deal with over the past six months.[i] We won’t recap the main events here—you lived them. However, we do think it is worth highlighting a couple of market-related developments and the lessons they impart.

Chief among them: Markets anticipate developments few foresee. On February 12, global stocks closed at an all-time high.[ii] The next day, they fell -0.2%.[iii] It seemed like a typical daily blip, the kind history doesn’t bother remembering. The world was aware of COVID-19, but cases outside Asia were isolated and seemingly rare. Considering no pandemic in history had ever ended a bull market, there seemed no rational reason to treat it any differently than SARS in 2003 or swine flu in 2009. Both hit sentiment, but neither caused deep economic or market problems. Lockdowns weren’t even in the conversation at a regional level, never mind a global one. But as politicians acted over the next month to contain the pandemic, stocks were forced to digest lockdowns and their economic consequences in short order. They hit bear market territory (-20% from a prior high) on March 12, the fastest ever.[iv] On March 23, they closed down -34% from the high.[v] Most of the US and Europe were under shelter-in-place orders. Japan was headed that way. No economic data had yet measured the negative impact, but everyone was sure it would be bad.

But the next day, stocks rose. They kept rising, overall and on average, for the next several weeks—even as economic data began emerging and notching record-awful readings. Pundits said rising stocks were ignoring reality, but we think dispassionate observation shows stocks had simply shifted to looking further into the future. Past the immediate hemorrhaging, past the gradual fall in COVID caseloads, past the baby steps toward reopening the US and Europe, past occasional setbacks, and to a day further out when society learned how to live with the virus and maintain some semblance of normal economic activity. As Q2 progressed and more cities reopened, that eventuality became more apparent. By June’s end, those who hung on were rewarded with global stocks’ 38.2% bounce off the low.[vi]

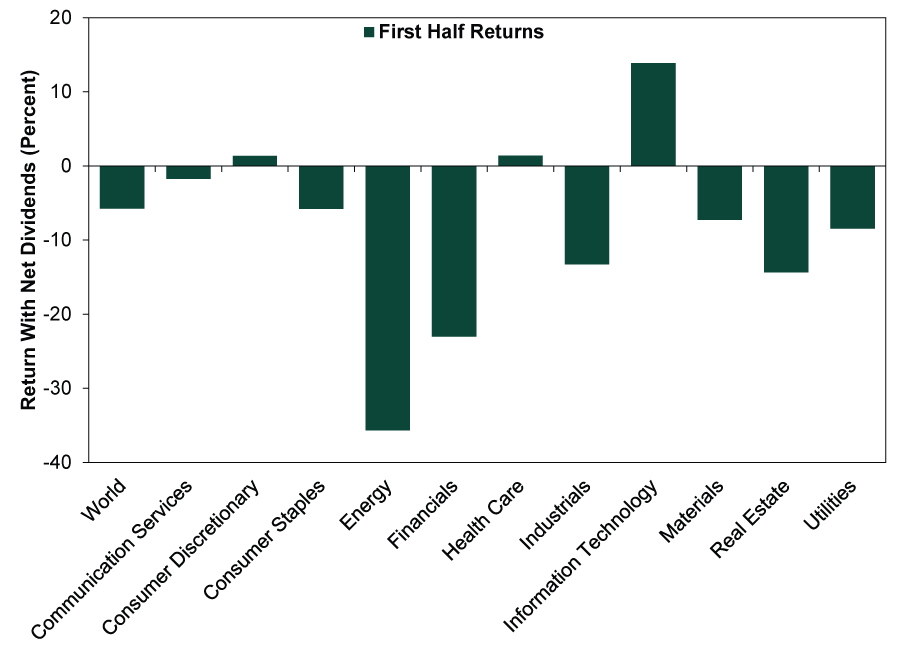

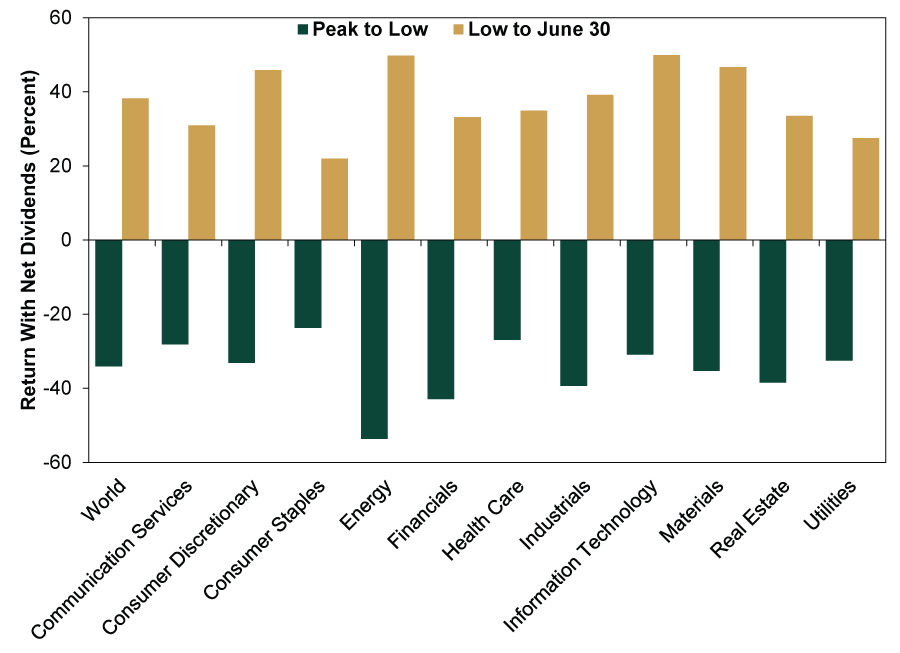

Don’t let anyone tell you it was easy—especially not with so much variance among sectors. Exhibit 1 shows the MSCI World Index and all 11 sectors’ first-half returns. To get them, though, you had to live with the reality shown in Exhibit 2, which separates each sector’s return from peak to trough—and trough to June 30. Even Tech, widely touted as a coronavirus winner for its outperformance, had a rough ride early in absolute terms. Reaping its positive first-half return required all the patience the human spirit can muster.

Exhibit 1: MSCI World Index and Sector Returns in 2020’s First Half

Source: FactSet, as of 7/1/2020. MSCI World and constituent sector returns with net dividends, 12/31/2019 – 6/30/2020.

Exhibit 2: MSCI World Index and Sector Returns on Both Sides of a V

Source: FactSet, as of 7/1/2020. MSCI World and constituent sector returns with net dividends, 2/12/2020 – 3/23/2020 and 3/23/2020 – 6/30/2020.

In our view, these charts also exhibit the follies of heat chasing. Energy has been the second-best sector in the rebound thus far. But it also got hammered hardest on the way down, as lockdowns wrecked demand for oil and gas and OPEC’s gamesmanship monkeyed with supply. That bounce off the bottom came nowhere close to recouping all the earlier declines, and with supply still abundant and demand only partly recovering, oil companies probably have difficulty reaping big profits for the foreseeable future. These issues are widely known, suggesting to us they don’t present a reason for Energy stocks to fall from here. But we are skeptical the sector’s huge bounce off the low persists ahead.

Energy is also something of an exception in another sense. While this bear market had the magnitude and an identifiable fundamental cause of a typical bear market, in terms of speed, it acted more like a correction. Bear markets usually begin gradually, grinding lower for months before Mr. Market pulls the rug out in its final throes. Corrections, by contrast, usually plunge fast throughout, then end equally suddenly. That is how this bear market behaved.

This isn’t mere trivia. The bear market’s duration has implications for style leadership. Usually, small value stocks lead in a new bull market. They typically get hammered hardest in a bear’s final plunge, when investors ditch anything that has even the slightest chance of not surviving the associated recession. That makes them the prime target for bargain hunters in a new bull market. But for that to happen, we think stocks have to go through the full progression of a long, grinding bear market. Otherwise, if the market behaves more like it does during a correction, then it becomes much more likely that the category leading before the downturn—in this case, large growth stocks—leads in the recovery as well.

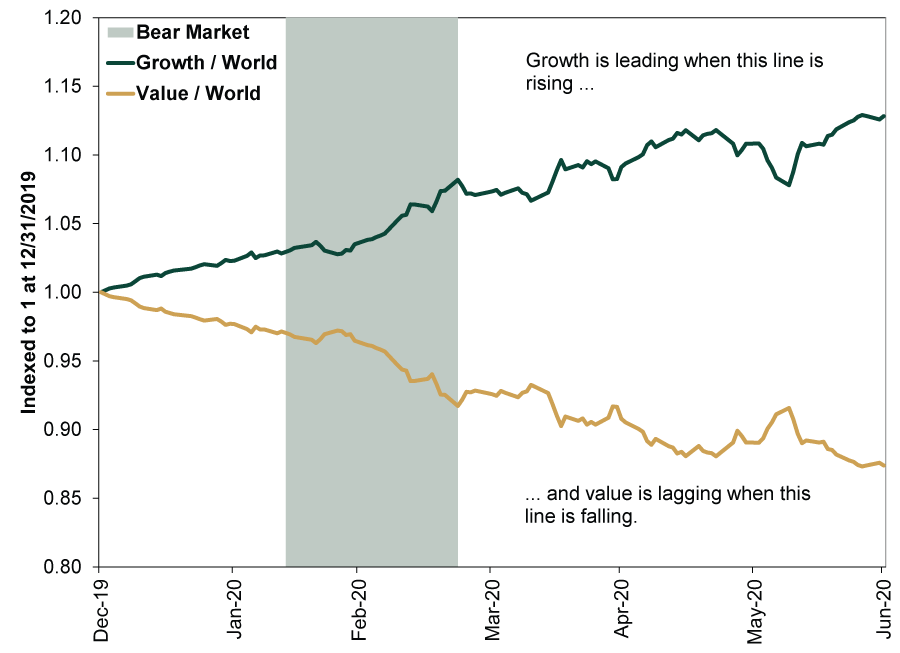

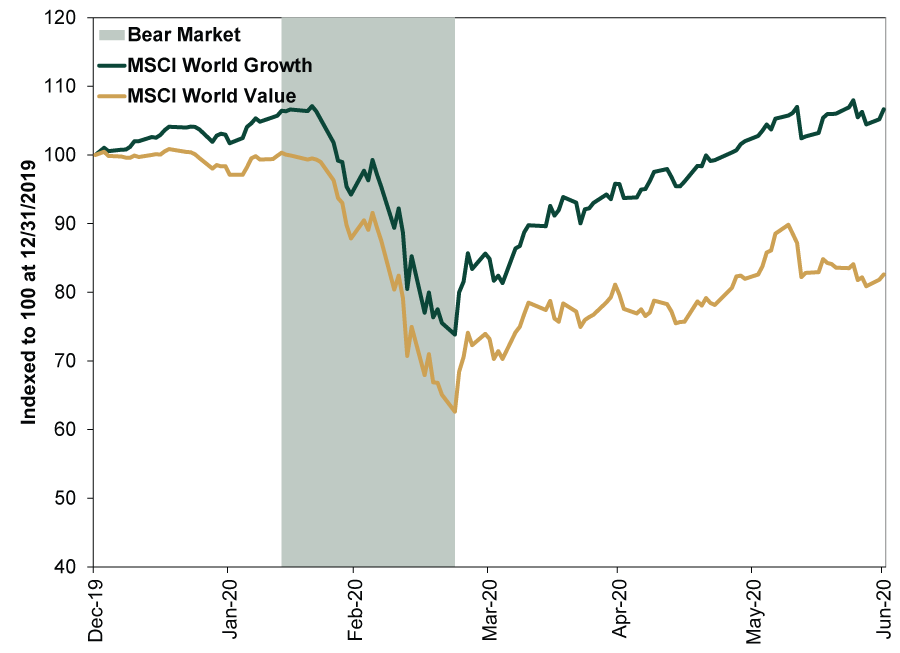

So far, that has happened this time. Large growth led heading into the bear market. It led cumulatively during the bear market. And it has led since the recovery (Exhibit 3). It still fell plenty during the downturn on an absolute basis (Exhibit 4), but on a relative basis, it has brought the most benefits.

Exhibit 3: Value and Growth’s Relative Returns in 2020

Source: FactSet, as of 7/1/2020. MSCI World Value and MSCI World Growth returns relative to the MSCI World Index with net dividends, 12/31/2019 – 6/30/2020. Indexed to 1 at 12/31/2019.

Exhibit 4: Value and Growth’s Absolute Returns in 2020

Source: FactSet, as of 7/1/2020. MSCI World Value and MSCI World Growth returns with net dividends, 12/31/2019 – 6/30/2020. Indexed to 100 at 12/31/2019.

Looking ahead, we think growth stocks are poised to keep leading. For one, while value lagged, it didn’t suffer the typical late-bear market hammer blow. Two, most pundits expect small value stocks to lead, citing their normal early bull market history. In general, when the masses expect something to happen in markets, that becomes priced in, and something else happens instead. Unless sentiment shifts radically and value becomes unloved, we doubt a leadership shift materializes.

This year’s rocky first half is no doubt one for the record books. If you endured all the swings, worries, uncertainties and painful drops, kudos to you. The rebound since March 23 is part of the reward for your fortitude, in our view.

[i] Source: FactSet, as of 7/2/2020. MSCI World Index return with net dividends, 12/31/2019 – 6/30/2020.

[ii] Ibid. MSCI World Index level with net dividends, 12/31/1969 – 2/12/2020.

[iii] Ibid. MSCI World Index return with net dividends, 2/13/2020.

[iv] See note ii.

[v] Ibid. MSCI World Index return with net dividends, 2/12/2020 – 3/23/2020.

[vi] Ibid. MSCI World Index return with net dividens, 3/23/2020 – 6/30/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today