Personal Wealth Management / Economics

About That Dour Reaction to Fine Q4 US GDP

The popular reaction to a fine Q4 US GDP report shows dour sentiment setting a low bar for reality to clear, in our view.

Q4 GDP hit yesterday, about a month later than usual due to the government shutdown. There weren’t any big revelations, with growth continuing at a fine rate and matching expectations. But the accompanying negative outlook from pundits suggests a low bar for economic reality to clear this year to boost stocks.

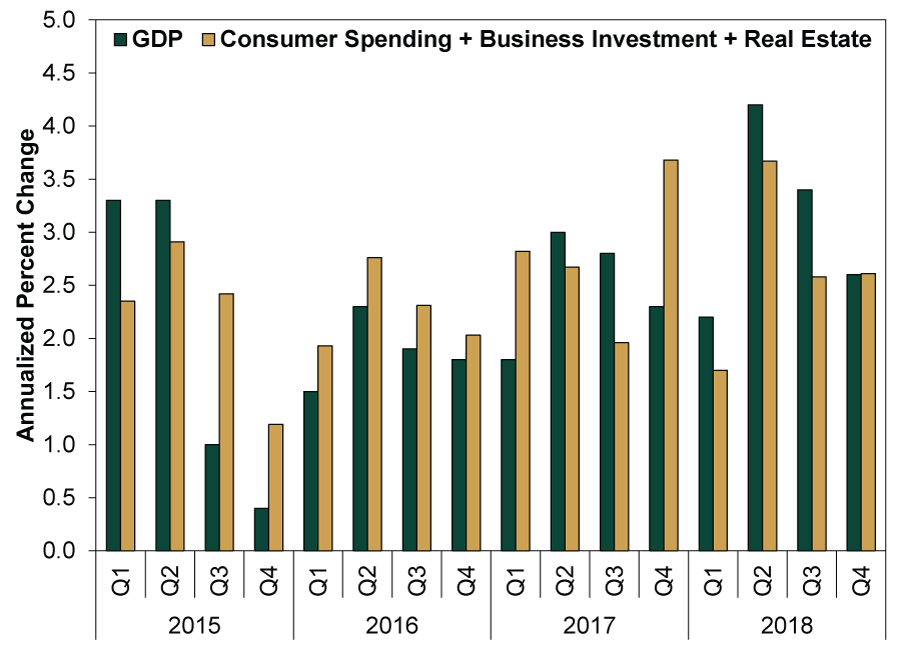

First, the numbers. GDP rose 2.6% annualized in Q4, slowing from Q3’s 3.4% as forecasters anticipated.[i] Consumer spending—69% of GDP[ii]—rose 2.8% annualized (slowing from Q3’s 3.5%). Business investment also contributed, accelerating to 6.2% from Q3’s 2.5% as investment in intellectual property products jumped 13.1%. Meanwhile, residential investment declined -3.5% annualized, its fourth straight negative quarter. Not great news for that sector, but not a huge driver of overall growth, as residential real estate is just 3% of GDP.[iii] Even with its decline, total private sector demand (e.g., consumer spending, business investment and residential investment) rose 2.6%. (Exhibit 1) Meanwhile, exports and imports rose 1.6% and 2.7% annualized, respectively, signaling the US economy’s resilience to China’s slowdown, which knocked trade throughout Europe and Asia in Q4.

Exhibit 1: GDP and Private Sector “Core GDP”

Source: Bureau of Economic Analysis, as of 2/28/2019. GDP and “Core GDP” consisting of personal consumption expenditures, private nonresidential fixed investment and residential fixed investment, Q1 2015 – Q4 2018.

A solid report! Growth is broad-based and in line with recent years. Yet many continue fretting a cooling economy. Some suggest GDP’s back-to-back deceleration in Q3 and Q4 means the economy is losing momentum and should see steadily weaker growth from here. One widely cited survey this week showed about half of the country’s business economists expect a recession by 2020, with about three-fourths seeing one by 2021.[iv] A popular argument says tax cuts fueled growth, but their effect is now fading, making recession likelier absent further stimulus. Others believe weak home sales imply a “housing recession” that will spread to the wider economy. Many also think global economic uncertainty—from China and Europe—could drag the US down.

This tells you where sentiment is. But these fears are far from guaranteed to come true. Pessimists have pooh-poohed growthy data since this expansion’s first green shoots emerged nearly 10 years ago. They have been too dour at nearly every turn. We think the same is true today. The supposed negatives are either well known, not huge, one-offs or some combination thereof. We think people actually overestimate tax cuts’ impact. The corporate profit tax cut helped boost earnings, but history shows small household tax cuts usually have minimal impact on consumer spending. They are only one small variable. As for China’s slowdown rippling, US exports depend much more on Canada and Mexico, which are in good shape. So is the global economy, judging by the world’s loan and money supply growth.

Persistent pessimism in the face of broadly supportive economic data is a sign sentiment underappreciates reality. Leading indicators—like the yield curve, credit growth and new orders—all point positively, setting an easy hurdle for reality to clear. Markets move on the gap between reality and expectations, and with expectations quite low, we expect upside surprises to buoy stocks for the foreseeable future.

[i] Source: Bureau of Economic Analysis, as of 2/28/2019.

[ii] Source: Federal Reserve Bank of St. Louis, as of 3/1/2019. Personal consumption expenditures as a percentage of GDP, Q4 2018.

[iii] Ibid. Private residential fixed investment as a percentage of GDP, Q4 2018.

[iv] “Most Economists See U.S. Recession by 2021, Survey Shows,” Alexandre Tanzi, Bloomberg, 2/25/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today